Alberta

Danielle Smith: Is there Going to Be a Central Bank Digital Currency? Almost Certainly

This newsletter was distributed by Danielle Smith.

I started my Western Standard show last week in the same week I was moderating a two-day conference for the Canadian Blockchain Consortium. So my shows last week were centred around trying to educate people as to what is cryptocurrency and Bitcoin, in particular, and how it is being used by regular people: such as when governments hyperinflate their currencies – like this story in Venezuela where people use it to buy food – or when countries fall apart like in Ukraine – where this man used the Bitcoin in the wallet on his phone to escape from the country before conscription came in.

As a side note, I can tell you I haven’t missed the cesspit of social media commentary. Part of the agreement with Western Standard is they broadcast on the social media channels so I get social media trolls shit posting me through the entire show. Delightful.

But I do take seriously those in our community who write me emails and approach me at events to express concerns.

Amanda is an example. She thanked me for the primers and said, “I was just chatting with a friend who said Poilievre needs to tone it down on that (cryptocurrency) because he is losing people like her because it is not well understood.” Others told me they wanted me to stop talking about Bitcoin also because they don’t understand it and they said I should just talk about freedom instead.

My dears…

I wish I could stop the world so we could all get off.

I’d probably get off in the year 2005 – just when we had all the advantages of technology but none of creepiness. I could easily live in a world before iPhone. I loved my blackberry. My husband would probably choose the 1950s when we still had passenger rail service and men wore hats. He can do without technology completely.

But we are in the world of the Technocreepy (to borrow the phrase coined by professor Thomas Keenan) and, ironically, it is one where you will soon be able to fully immerse yourself in whatever world you choose. I’m just learning about the Metaverse, but the concept of it is to use virtual reality goggles to enter into a world of digital avatars and artificial intelligence to meet up with others in a constructed environment. “Meet you for a wine on the train from Calgary to Toronto in 1950” may one day be a weekend date for my husband and me.

Central Bank Digital Currency vs Cryptocurrency…

But the biggest uneasiness I’m hearing is around the concept of a central bank digital currency. Pierre Poilievre has said he is absolutely opposed to a central bank digital currency at the same time as he says he wants to make Canada the blockchain capital of the world and make it easier to receive payments in cryptocurrency. That should tell you right there that a digital currency (issued by a central bank) and a cryptocurrency (not issued by a central bank) aren’t the same thing. More on that in a minute.

I’m hearing from many of you who are feeling unease that you don’t want either one. You say you want to move to bartering or stay in cash.

Two things…

You will always be free to barter goods but I would put it to you that it will be pretty limiting. There a remains a problem that most employers will still want to pay you in cash and most businesses will want to receive cash for your purchases. Anyone who has success in trading their baked bread and jars of chutney at the automechanic should let me know so I can be corrected. But I suspect you won’t find many takers.

I also don’t want our old dears thinking that the safest way to hold money is to withdraw cash from the bank and put it under their mattress. Holding cash in an environment where we have 10 to 15 per cent annual inflation is positively the worst advice anyone could give. Your money just loses its value year after year. That’s no way to preserve wealth either.

People say they want politicians to level with them. But now that I’m levelling with you about what is coming and how you can counter it, you are telling me you are too afraid to listen so I should just shut up about it.

I acknowledge your fears.

But I would ask you to soldier on and try to understand how the world is going to change. Because the World Economic Forum compendium document on digital currencies released in November 2021 shows a central bank digital currency is where the central bankers of the world are moving and it is has already started in China and Russia.

Here’s some background on where we already sit…

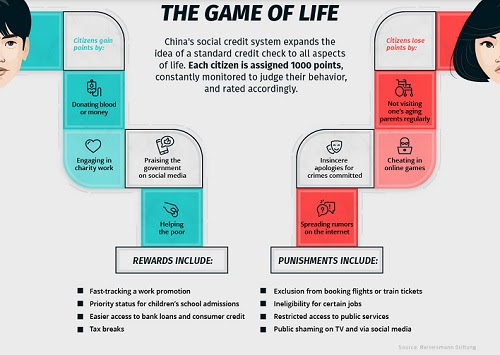

Bahamas was the first, but China rolled out its central bank digital currency called the renminbi last year and Time Magazine wrote about it last August in advance of the Beijing Olympics. The Chinese already have 96 per cent of their transactions taking place digitally with private options through Alipay and WeChat. Citizens like it. They simply flash a QR code on their smartphone screen to pay for everything they need: commuter tickets, lunch, convenience store items.

Chinese citizens are now voluntarily switching to the digital central bank renminbi – there are already more than 260 million individual users of the central bank digital coin. Also, 86 per cent of world’s central bankers (according to a survey by the Bank for International Settlements) are actively researching adopting their own.

Why do governments like the idea so much? Oh, so many reasons.

The biggest change of money since the gold standard…

According to Time, “It’s the biggest change in money since the end of the gold standard.”

The reason political leaders like digital coins is because there are “tremendous new functionalities.” For example:

Transfer “tokens” could be created to instantly transfer homes and property. You could own a “token” for a fractional share of any asset including vacation property, precious gems, art or other collectibles. It will reduce cross border transaction fees and costs to the financial services industry, which currently amount to $350 a year for each person in the world. It will make the SWIFT banking system – the one the Americans have used to cut off Iran and Russia – obsolete. And governments will be able to see all financial transactions rather than having to ask banks to provide it. It will also allow 1.7 billion people who have no bank accounts to get access to money.

But there is a dark side too…

There is also a reason authoritarian regimes like China like it too. From the Time article:

“In the Chinese pilot program, money has an expiration date of a few weeks because authorities are hoping to drive consumption in an economy trying to recover from the pandemic. Cash can be customized for other purposes. If the government is trying to stimulate the hospitality industry in a certain area, for example, it can program money to be used for meals and drinks but not for, say, petrol or power tools… Linked to China’s social credit system, it could see citizens fined in a split second for behaviors deemed undesirable. Dissidents and activists could see their wallets emptied or taken offline.”

So why does Poilievre oppose central bank digital currency and yet support cryptocurrency, the most important of which is Bitcoin? This article in the National Telegraph describes the differences well.

“Bitcoin as a currency functions as an anti-CBDC in a lot of ways. Where CBDCs are completely controlled by a central authority, Bitcoin is 100 percent decentralized, no one can mess with the system. CBDCs can have built-in controls so they can discriminate based on age, sex, wealth, race, or whatever other categories the government wanted, Bitcoin, on the other hand, has no control built-in so discrimination is impossible. While every CBDC transaction can be tracked and recorded Bitcoin transactions can be done peer to peer and are untraceable to a specific person. CBDCs are a windfall for bankers who love to print money and run up inflation, Bitcoin is a deflationary asset that less and less of can be mined every four years.”

Bitcoin is essentially an antidote to central bank coins.

A new geopolitical realignment…

There is a law of the universe: for every action there is an equal and opposite reaction. The Americans throwing their weight around by excluding countries from the SWIFT system has accelerated the move from using the US dollar as an intermediary for global transactions and contracts. This will change the US dollar from being the de facto international currency and all the geopolitical shifts that implies.

Will it be good for us, tied as we are to the Americans?

I’m not sure yet, which is why I am following this closely. This article in the Algora blog site believes the change signals the end of Western domination and that we are going to find ourselves isolated from the rest of the world. According to them we are witnessing the end of globalization and the world is being split in two with the US, Europe and its allies (10 per cent of the world population) in one corner and the Brazil, Russia, India, China and South Africa – BRICS partners – representing 90 per cent of the world population on the other side.

“Reacting swiftly, Russia has convinced its BRICS partners to stop trading in dollars and to eventually create a common virtual currency for their exchanges. Until then, they will proceed in gold. This currency should be based on a basket of BRICS currencies, weighted according to the GDP of each member state, and on a basket of commodities listed on the stock exchange. This system should be much more stable than the current one.”

So if I were a guessing person, I would imagine this is going to be the model for how a new common digital currency will emerge for us.

Canada would develop its own central bank digital currency. Then we would opt in to a common virtual currency that includes the US, Europe, Australia and anyone else who wants to join us based on a basket of our currencies weighted according to GDP and (maybe?) a basket of commodities on the stock exchange.

The reason I think this is inevitable and that it will happen before Pierre Poilievre gets elected in 2025 and gets a chance to stop it, is because the momentum to do something to address our damaged currency is already too great.

The Great Money Printing Crusade of the last two years has rendered western currencies increasingly valueless. Printing money only works in the short term. Eventually you outpace the ability of the economy to keep up with producing goods and it causes inflation. Canadian inflation was 6.7 per cent last month – the highest it’s been in 30 years.

The Central Bank has already started raising rates to rein in spending and rate hikes are expected to continue.

I can imagine a few ways that shifting to a central bank digital coin could bail the government out of the mess it has created.

As we’ve seen in China, if it were implemented as a pilot project I suspect a large number of Canadians would simply sign up. We saw through COVID that at least 90 per cent of the public (or more) will do whatever the government tells them to do. So I suspect there will be a high uptake of the digital coin.

So yes, while I think we have reason to be gravely concerned that the federal government will want to use our transactions to micromanage our affairs, nudge us, monitor our ESG profile, and potentially punish us, I think we should also consider that the real reason for the global desire to suddenly go digital is so government can profit from the digital coin.

How Debt Jubilees Work…

Lyn Alden has done a wonderful write up of the historical experience with debt jubilees, which date back 4000 years. It began because farmers would be severely indebted to their lenders after a harvest failed and to avoid debt servitude, slavery or land seizure, the rulers from time to time (every 50 years or so) would just declare a debt jubilee so that all was forgiven. In the absence of this periodic forgiveness, more and more money would concentrate in the hands of the few, more and more would be pushed into poverty and there would be a popular uprising that would result in more than a few beheaded leaders.

No one in power ever wants that to happen.

And so we find ourselves in a familiar debt trap.

As Alden says, now that we have divorced our currency entirely from gold, we have created a banking ouroboros that makes it (nearly) impossible for central banks to forgive debt. In the past you could simply rebase your currency relative to the price of gold. Now we have a circular system: “Commercial banks store their cash at the central bank, which are assets for the commercial banks and liabilities for the central bank. In turn, the central bank holds government debt as its primary collateral assets. Government debt is backed up by the government’s ability to tax its citizens, and in practice, by having the central bank create new bank reserves to buy its government debt when needed. We can’t just remove one piece of it, like government debt from the central bank balance sheet. The monetary base is collateralized by government debt, and government debt is supported by expanding the monetary base when needed. It’s basically an ouroboros.”

So with inflation kicking in, interest rates rising, private debt in the stratosphere, government debt in the mesosphere, and no ability to cancel it all, what is a central banker to do?

One, they can do some “debt restructuring” and convert government bonds into 100-year zero coupon bonds, making the debt no longer relevant but allowing the central bank to raise rates for you and me while protecting themselves.

Two, they can hold interest rates below inflation, and let high inflation rates “burn debt away”, even though it will affect you and me in our purchasing power for the goods we need to buy on a daily basis. You can pay off your debt more easily then, but it will cost more to buy food and electricity.

Three, they could just steal it directly by doing a bail in, like they did in Cyprus in 2013, where the government taxed bank deposits up to 9.9 per cent and issued worthless equity certificates in exchange for the theft.

I’m wondering if a central bank digital coin offers a fourth way?

What about a Financial Transactions Tax?…

If it is indeed the case that the financial services industry costs $350 per person per year, it seems to me a digital currency is a way for the government to capture some of this revenue.

If you consider that the dollar from 1971 until today has been a petrodollar based on the flows of oil and natural gas denominated in the US currency, if we are moving to a digital dollar based on the amount of GDP and flow of financial transactions, what new revenue generating possibilities does that open for government?

I remember reading years ago about a proposal from Green Party Leader Elizabeth May for a financial transactions tax. The idea was to levy a tax on all sales of stocks and bonds and other financial holdings, to stick it to the rich but to also discourage speculative trading. In the US, they calculated charging 0.2 per cent ($2 on every $1000 in trade) would generate $777 billion over 10 years. Canada, with half the size, might expect to generate a $77 billion over 10 years.

But what if the concept was expanded to generate a fee for all transactions in Canadian dollars, equivalent to the transaction fees already being paid in the cryptocurrency markets? And what if all governments collaborated to make sure everyone charged the same tax so it couldn’t be avoided?

In Bitcoin, transactions under $10,000 carry a fee of 0.5 per cent. Canada’s Gross Domestic Product is $1.643 Trillion compared to a world GDP of $84.71 Trillion.

So if $1.7 trillion Canadian digital dollars trade hands each year, and the government could generate $5 for every $1000 spent, that would be $8.5 billion a year. But why stop there?

Banks often charge etransfer fees of $1.50 a transaction. At the top end, Visa and Mastercard charge 3.4 per cent on transactions. If the Bank of Canada were to charge rates that high on all Canadian dollar transactions they’d generate $58 billion a year.

Now we are talking some real money…

At the Blockchain conference this week, the keynote fireside chat was with Jeff Booth, author of The Price of Tomorrow: Why Deflation is the Key to an Abundant Future. In the video below he talks with Real Vision Finance about the pattern of inflation we have seen throughout history and how it creates a predictable pattern of behaviour in government to keep getting elected.

First they create internal division to distract people to stay elected, and when that stops working they blame another country. We have a structural change that is happening in the country, he says, and everything we are talking about is two orders of magnitude away from the first principles we should be talking about.

So I know this is uncomfortable. I know you don’t want me to talk about it. But we must. Because money affects everything.

So now you are thinking, if Canada is moving toward a central bank digital currency, and the WEF is championing central bank digital currencies, and if governments can use it to develop social scores (like China) to punish and reward its citizens, how can you escape the system?

How can you get the equivalent of cash that can’t be centrally controlled, monitored, devalued or turned off?

Now you understand why so many of us are interested in Bitcoin and cryptocurrency.

How you can help…

If you want to support me personally there are three ways to do it.

Book me to speak at your event: If you want me to do an event or coffee party in Livingstone Macleod I am happy to line it up. Just email [email protected] and my executive assistant will book it. If you are not in the constituency of Livingstone Macleod and want me to speak about The Future of Alberta and The Alberta First Initiative, my fee is $500 and you can book me by emailing me at [email protected]

The Danielle Smith Show: The Danielle Smith Show launched April 18. I did three 30 minute news monologues on Bitcoin during the week and a weekend long form interview on Saturday with Gord Tulk on health care spending accounts and radical idea to reform confederation. You can tune in live at 9 am or listen on podcast. Send me an email at [email protected] if you want to discuss sponsorship or advertising.

Subscribe to my Free Weekly Newsletter: Subscribe to this newsletter by going online to http://daniellesmith.ca. I will continue to write to you weekly.

See Previous Newsletters Online: Go to https://daniellesmith.ca/

Sign up on Locals: For Subscribers Only I will be doing a one hour livestream call in/text in so you can Ask Me Anything on Friday at 11 am as well as posting my thoughts on the issues of the day. I’ve set the minimum subscription fee very low – $2US a month – because I don’t want to create a barrier but I don’t want to content with anonymous bots and trolls either.

The Livingstone Macleod campaign …

My campaign website is http://daniellesmithucp.ca

You can donate online (sorry no tax receipts unless I am the nominated candidate!) to a maximum individual donation of $4000. This money will be put to use to pay for my campaign manager, scheduler, web designer, social media, signs and literature. I would be grateful for your contribution. I also need the gift of time, so if you can volunteer I will need that too! There is a portal on the website to sign up for campaign specific emails and to buy a UCP membership.

Donate by Mail: Make Cheques out to the Danielle Smith Campaign and send to 5548 Station Main, High River, Alberta, T1V 1H2.

Upcoming Events and Appearances…

April 25 Seminar to the CPAA on The Future of Alberta

April 27 AEG Calgary Event

April 27 Zoom telephone town halls for Livingstone Macleod

April 28 Crownest Pass Responsible Coal Association town hall

April 30 Civitas

May 4 Lethbridge Event with UCP Members

May 7 Airdrie Event with UCP Members

May 12 Canada in Question with Peter McInnon

May 18 High River Event with UCP Members

May 19 Alberta Adolescent Recovery Centre Gala

| Donate |

What’s New?

The Danielle Smith Podcast is now available.

From LifeSiteNews

‘I think the court was in error,’ Alberta Premier Danielle Smith has said. ‘There will be irreparable harm to children who get sterilized.’

LGBT activists have won an injunction that prevents the Alberta government from restricting “gender transitions” for children.

On June 27, Alberta King’s Court Justice Allison Kuntz granted a temporary injunction against legislation that prohibited minors under the age of 16 from undergoing irreversible sex-change surgeries or taking puberty blockers.

“The evidence shows that singling out health care for gender diverse youth and making it subject to government control will cause irreparable harm to gender diverse youth by reinforcing the discrimination and prejudice that they are already subjected to,” Kuntz claimed in her judgment.

Kuntz further said that the legislation poses serious Charter issues which need to be worked through in court before the legislation could be enforced. Court dates for the arguments have yet to be set.

READ: Support for traditional family values surges in Alberta

Alberta’s new legislation, which was passed in December, amends the Health Act to “prohibit regulated health professionals from performing sex reassignment surgeries on minors.”

The legislation would also ban the “use of puberty blockers and hormone therapies for the treatment of gender dysphoria or gender incongruence” to kids 15 years of age and under “except for those who have already commenced treatment and would allow for minors aged 16 and 17 to choose to commence puberty blockers and hormone therapies for gender reassignment and affirmation purposes with parental, physician and psychologist approval.”

Just days after the legislation was passed, an LGBT activist group called Egale Canada, along with many other LGBT organizations, filed an injunction to block the bill.

In her ruling, Kuntz argued that Alberta’s legislation “will signal that there is something wrong with or suspect about having a gender identity that is different than the sex you were assigned at birth.”

She further claimed that preventing minors from making life-altering decisions could inflict emotional damage.

However, the province of Alberta argued that these damages are speculative and the process of gender-transitioning children is not supported by scientific evidence.

“I think the court was in error,” Alberta Premier Danielle Smith said on her Saturday radio show. “That’s part of the reason why we’re taking it to court. The court had said there will be irreparable harm if the law goes ahead. I feel the reverse. I feel there will be irreparable harm to children who get sterilized at the age of 10 years old – and so we want those kids to have their day in court.”

READ: Canadian doctors claim ‘Charter right’ to mutilate gender-confused children in Alberta

Overwhelming evidence shows that persons who undergo so-called “gender transitioning” procedures are more likely to commit suicide than those who are not given such irreversible surgeries. In addition to catering to a false reality that one’s sex can be changed, trans surgeries and drugs have been linked to permanent physical and psychological damage, including cardiovascular diseases, loss of bone density, cancer, strokes and blood clots, and infertility.

Meanwhile, a recent study on the side effects of “sex change” surgeries discovered that 81 percent of those who have undergone them in the past five years reported experiencing pain simply from normal movements in the weeks and months that followed, among many other negative side effects.

![]()

By Mark Milke

It is a mistake to dismiss the movement as too small

In light of the poor showing by separatist candidates in recent Alberta byelections, pundits and politicians will be tempted to again dismiss threats of western separatism as over-hyped, and too tiny to be taken seriously, just as they did before and after the April 28 federal election.

Much of the initial skepticism came after former Leader of the Opposition Preston Manning authored a column arguing that some in central Canada never see western populism coming. He cited separatist sympathies as the newest example.

In response, (non-central Canadian!) Jamie Sarkonak argued that, based upon Alberta’s landlocked reality and poll numbers (37 per cent Alberta support for the “idea” of separation with 25 per cent when asked if a referendum were held “today”), western separation was a “fantasy” that “shouldn’t be taken seriously.” The Globe and Mail’s Andrew Coyne, noting similar polling, opined that “Mr. Manning does not offer much evidence for his thesis that ‘support for Western secession is growing.’”

Prime Minister Mark Carney labelled Manning’s column “dramatic.” Toronto Star columnist David Olive was condescending. Alberta is “giving me a headache,” he wrote. He argued the federal government’s financing of “a $34.2-billion expansion of the Trans Mountain pipeline (TMX)” as a reason Albertans should be grateful. If not, wrote Olive, perhaps it was time for Albertans to “wave goodbye” to Canada.

As a non-separatist, born-and-bred British Columbian, who has also spent a considerable part of his life in Alberta, I can offer this advice: Downplaying western frustrations — and the poll numbers — is a mistake.

One reason is because support for western separation in at least two provinces, Alberta and Saskatchewan, is nearing where separatist sentiment was in Quebec in the 1970s.

In our new study comparing recent poll numbers from four firms (Angus Reid Institute, Innovative Research Group, Leger, and Mainstreet Research), the range of support in recent months for separation from Canada in some fashion is as follows, from low to high: Manitoba (6 per cent to 12 per cent); B.C. (nine per cent to 20 per cent); Saskatchewan (20 per cent to 33 per cent) and Alberta (18 per cent to 36.5 per cent). Quebec support for separation was in a narrow band between 27 per cent and 30 per cent.

What such polling shows is that, at least at the high end, support for separating from Canada is now higher in Saskatchewan and Alberta than in Quebec.

Another, even more revealing comparison is how western separatist sentiment now is nearing actual Quebec votes for separatism or separatist parties back five decades ago. The separatist Parti Québécois won the 1976 Quebec election with just over 41 per cent of the vote. In the 1980 Quebec referendum on separation, “only” 40 per cent voted for sovereignty association with Canada (a form of separation, loosely defined). Those percentages were eclipsed by 1995, when separation/sovereignty association side came much closer to winning with 49.4 per cent of the vote.

Given that current western support for separation clocks in at as much as 33 per cent in Saskatchewan and 36.5 per cent in Alberta, it begs this question: What if the high-end polling numbers for western separatism are a floor and not a ceiling for potential separatist sentiment?

One reason why western support for separation may yet spike is because of the Quebec separatist dynamic itself and its impact on attitudes in other parts of Canada. It is instructive to recall in 1992 that British Columbians opposed a package of constitutional amendments, the Charlottetown Accord, in a referendum, in greater proportion (68.3 per cent) than did Albertans (60.2 per cent) or Quebecers (56.7 per cent).

Much of B.C.’s opposition (much like in other provinces) was driven by proposals for special status for Quebec. It’s exactly why I voted against that accord.

Today, with Prime Minister Carney promising a virtual veto to any province over pipelines — and with Quebec politicians already saying “non” — separatist support on the Prairies may become further inflamed. And I can almost guarantee that any whiff of new favours for Quebec will likely drive anti-Ottawa and perhaps pro-separatist sentiment in British Columbia.

There is one other difference between historic Quebec separatist sentiment and what exists now in a province like Alberta: Alberta is wealthy and a “have” province while Quebec is relatively poor and a have-not. Some Albertans will be tempted to vote for separation because they feel the province could leave and be even more prosperous; Quebec separatist voters have to ask who would pay their bills.

This dynamic again became obvious, pre-election, when I talked with one Alberta CEO who said that five years ago, separatist talk was all fringe. In contrast, he recounted how at a recent dinner with 20 CEOs, 18 were now willing to vote for separation. They were more than frustrated with how the federal government had been chasing away energy investment and killing projects since 2015, and had long memories that dated back to the National Energy Program.

(For the record, they view the federal purchase of TMX as a defensive move in response to its original owner, Kinder Morgan, who was about to kill the project because of federal and B.C. opposition. They also remember all the other pipelines opposed/killed by the Justin Trudeau government.)

Should Canadians outside the West dismiss western separatist sentiment? You could do that. But it’s akin to the famous Clint Eastwood question: Do you feel lucky?

Mark Milke is president and founder of the Aristotle Foundation for Public Policy and co-author, along with Ven Venkatachalam, of Separatist Sentiment: Polling comparisons in the West and Quebec.

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

The Passage of Bill C-5 Leaves the Conventional Energy Sector With as Many Questions as Answers

Federal fiscal anchor gives appearance of prudence, fails to back it up

-

COVID-1911 hours ago

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

-

Energy19 hours ago

Energy19 hours agoThis Canada Day, Celebrate Energy Renewal

-

Business2 days ago

Business2 days agoWhile China Hacks Canada, B.C. Sends Them a Billion-Dollar Ship Building Contract

-

Alberta1 day ago

Alberta1 day agoSo Alberta, what’s next?

-

Alberta10 hours ago

Alberta10 hours agoAlberta Next Takes A Look At Alberta Provincial Police Force

-

Bjorn Lomborg2 days ago

Bjorn Lomborg2 days agoThe Physics Behind The Spanish Blackout

-

Alberta12 hours ago

Alberta12 hours agoCanadian Oil Sands Production Expected to Reach All-time Highs this Year Despite Lower Oil Prices

-

Business14 hours ago

Business14 hours agoPotential For Abuse Embedded In Bill C-5