Opinion

Middle Class

The middle class.

This phrase is shrouded in mystery but typically refers to ones occupation, income, education and social status in relation to others.

Depending on the political party using the term, the underlying definition can change.

The Liberal Party has an entire section of it’s 2019 election platform dedicated to the middle class and people working hard to join it.

Unfortunately, the Minister of Middle-Class Prosperity has had difficulties defining the characteristics of the people she was elected to represent.

Excuse me if I’m a little concerned that the middle class might be forgotten as a result.

Making Life More Affordable

Any claims of government giving anything to citizens “tax free” should be met with scrutiny.

All government funding ultimately comes from taxpayers so to suggest that government can give you tax free funds is simply not accurate. Someone is being taxed in order to provide the benefits.

Effective for 2016 tax filings, the Liberal Government lowered the tax rate on income in the 2nd tax bracket by 1.5%. This bracket currently applies to income between $48,535 to $97,069. All other brackets have either remained the same or increased since that time.

For those earning up to the maximum of $97,069, this results in tax savings of $1,456.

In conjunction with the 1.5% tax drop, the Liberal Government removed the Family Tax Cut (FTC). This allowed families with children to notionally transfer income from the spouse with higher annual income to the other spouse.

Depending on your situation, this could result in a tax credit of up to $2,000.

Effective in 2019, the Liberal Government implemented an increase in the Canada Pension Plan annual rates. By 2023, this will result in additional annual employee contributions of $1,107 for those earning above the annual ceiling of $65,700.

The employer portion would increase in proportion, putting further pressure on small business cash flows.

While the Liberal Government may claim that they are “making life more affordable”, the numbers above paint a different picture.

What should the government do?

The Canadian Income Tax Act (ITA) has not seen a major review since the late 1960’s. It is now a patchwork of legislation that is difficult for even seasoned Chartered Professional Accountants to apply into practice.

Complexities within the ITA result in a significant added administrative burdens. Instead of focusing on growing your business, creating jobs or planning for retirement, significant time is lost navigating the ITA.

The government should immediately engage in a full scale review of the ITA. The review must consult the private sector and address all major industries across Canada. The revisions should be made in such a way as to allow for amendments in future as the economy continues to evolve.

Key areas that should be the focus of a review:

-

Simplify: The tax system needs to be fair, efficient and competitive.

-

Modernize: Tax policy needs to be able to keep up with the digital economy.

-

Be Supportive: Changes to Canada Revenue Agency (CRA) policies that will ease compliance for taxpayers.

Simple:

In Alberta, there are now nine personal tax brackets, a patch work of credits and numerous complexities to navigate in complying with regulations relating to owner-operator business.

Serious consideration should be given to shift away from taxing income and toward taxing consumption instead. It is far more beneficial to tax activities that reduce the wealth of society, ie. consumption, rather than tax the creation of wealth.

The simplest way to make the shift to a consumption based tax system would be to increase the rate of federal GST. This would be offset with reductions in personal tax rates. The personal tax rate drops could be implemented in a manner that preserves the progressive tax regime, but with significantly fewer tax brackets.

For those in the lower tax brackets, the majority of their annual income is spent on non-GST’able expenditures such as groceries, rent and health care. Those with higher disposable incomes would contribute more to government revenues as a result. This preserves the progressive tax regime, protects the vulnerable and doesn’t penalize the creation of wealth.

More comprehensive reforms could also be analyzed to determine the best solution for Canadians.

Modernize:

In recent months, there has been a growing call for government to implement a “wealth tax”. The New Democratic Party has suggested that a 1% on families with a net worth in excess of $20 million would generate net tax revenue of $5.6 billion in 2020-21.

As mentioned above, government should not introduce further tax on the creation of wealth. This tax policy will only further drive investment out of the country at a time that we can ill afford it.

Additionally, there have been calls to add an additional layer of tax on big tech companies, most notably Google, Amazon, Facebook and Apple. There is no doubt that these companies have seen record profits in 2020 but haphazardly implementing a 3% tax on the revenues of these companies will likely back fire.

The reason why large corporations are able to take advantage of low tax rates in foreign jurisdictions is due to varied rates across the globe. If one jurisdiction makes the decision to implement a tax increase, naturally, corporations will seek out lower tax jurisdictions.

If government is concerned with tech giants skirting federal taxes, they need to consult with all jurisdictions in which these companies operate. A unilateral tax will simply resulting in these corporations moving profits to lower tax jurisdictions.

Be Supportive:

The Canada Revenue Agency is typically thought of with disdain by many Canadian taxpayers. Some of these feelings are self induced, others are not.

Much like the difficulties that individuals and businesses have in navigating the Income Tax Act (ITA), the same can be said for CRA agents. While the senior agents typically have specific training and field experience, the majority of front line CRA agents simply do not have the necessary training to effectively help taxpayers navigate the complexities of the ITA.

In order for the CRA to provide more supportive service to taxpayers, they too need to see a reform in the ITA. It simply is not fair to ask agents to be able to interpret the ITA and how it applies to each taxpayer they speak with.

Secondly, the CRA needs to revise audit training procedures for their agents that considers materiality of each case. Far too often I see audit cases that request significant amounts of supporting documentation in response to a taxpayers nominal expense claim. Some of these being less than $100.

This places a significant administrative burden on taxpayers, specifically small business owners. It also leads to a great deal of frustration, which further damages the relationship between this government agency and the general public.

Final Thoughts

Canada’s middle class has fallen on difficult times in recent years. This has only been exasperated by the impacts of COVID-19.

For far too long, Canada has lost investment and stymied growth due to its archaic tax regime.

The Liberal government has promised to “build back better” and create an economy that is just and equitable for all. Details of these plans remain to be seen.

Instead of grandiose plans stemming from pie-in-the-sky slogans, the government should immediately look to reform the tax system.

Focusing on simplicity, modernization and reducing administrative burden will give taxpayers the confidence to know that their hard work will translate into consistent after-tax earnings.

It’s time to unleash the power of the Canadian worker, supported by a competitive and modern tax regime. Future generations depend on it.

https://www.jaredpilon.com/

Quick Hit:

Village officials in Dolton, Illinois, have purchased the boyhood home of Pope Leo XIV, calling it a “once-in-a-lifetime opportunity” to bring pride, attention, and tourism to the community. The historic acquisition comes just weeks after Robert Prevost was elected pope.

Key Details:

- The three-bedroom, 1,050-square-foot home was purchased by the Pope’s parents in 1949 and remained in the family for nearly 50 years.

- Initially listed for $245,957, the home was removed from the market after Prevost’s election and later sold directly to the Dolton Village Board at a “significantly lower” price.

- Dolton Mayor Jason House called the deal a major win for the community, with board members and residents already seeing increased interest and tour bus traffic.

Diving Deeper:

The childhood home of Pope Leo XIV has officially been purchased by the village of Dolton, Illinois, after a unanimous vote by the Village Board on Monday night. Local officials are celebrating the move as a historic acquisition that could serve as a source of civic pride and new economic opportunity.

As reported by the New York Post, the modest 1,050-square-foot home—located just south of Chicago—was originally purchased by the Pope’s parents in 1949 for a $49 monthly mortgage. It stayed in the Prevost family for nearly half a century.

After Robert Prevost was elected pope, the home—initially listed on May 5 for $245,957—was pulled from the market and briefly entered into an auction process. That plan was ultimately scrapped in favor of a direct sale to the village. While the final purchase price hasn’t been disclosed, attorney Burt Odelson, who handled the deal, said it was “significantly lower than what they thought they would get.”

Mayor Jason House praised the acquisition as a unique chance to put Dolton on the map. “This is a once-in-a-lifetime opportunity,” House said. “We can either seize this moment and move it forward, or we can let that moment go to an investor. I would like our community to get the benefits of this opportunity.”

Tourism has already begun. Within hours of Pope Leo XIV’s election, visitors started arriving at the home. Officials say that momentum has only grown. Trustee Edward Steave said the traffic in the area speaks for itself: “If you ever see the traffic over there, the constant busloads in and out of our town, this is a great opportunity for us. This is a historical thing.”

Peter Doocy asked directly, “What happened to the Epstein client list that the Attorney General said she had on her desk?” Here’s how Leavitt tried to explain it.

The Epstein client list was supposed to be SITTING on Pam Bondi’s desk for review.

But months later, the DOJ says no such list even exists.

Karoline Leavitt was just asked why there was such a reversal in so little time.

Her responses today are raising eyebrows.

On February 21st, Pam Bondi told the world the Epstein client list was “sitting on [her] desk right now to review,” explaining it was part of a directive ordered by President Trump.

Shortly afterward, she and Kash Patel pledged to end the Epstein cover-up, promising to fully disclose the Epstein files to the public, hold accountable any government officials who withheld key evidence, and investigate why critical documents had been hidden in the first place.

But ever since late February, it seems the cover-up wasn’t exposed but buried even deeper by those who promised transparency.

First, they handed out the so-called “Epstein files” to influencers like golden Willy Wanka tickets, only for everyone to discover that almost all of the contents inside were already public and contained no new revelations.

Fast-forward to May, and suddenly Kash Patel and Dan Bongino are declaring firmly that Epstein killed himself.

“I’ve seen the whole file. He killed himself,” Bongino stated bluntly to Fox News’s Maria Bartiromo.

Today, the Trump-appointed DOJ and FBI released a new report that’s turning heads and raising plenty of questions.

They concluded that Epstein had no clients, didn’t blackmail anyone, and definitely killed himself.

FBI Concludes Epstein Had No Clients, Didn’t Blackmail Anyone, and Definitely Killed Himself

This article originally appeared on Infowars and was republished with permission.

They also released surveillance footage and claimed it showed no one entered Epstein’s cell area, supporting the suicide ruling.

But people aren’t convinced. Some allege the video cuts off, with a minute of footage missing between 11:59 PM and midnight.

Monday, White House Press Secretary Karoline Leavitt responded to questions about the Epstein client list in light of these new DOJ and FBI statements.

A reporter asked, “Karoline, the DOJ and FBI have now concluded there was no Jeffrey Epstein client list. What do you tell MAGA supporters who say they want anyone involved in Epstein’s alleged crimes held accountable?”

Leavitt replied, “This administration wants anyone who has ever committed a crime to be accountable, and I would argue this administration has done more to lock up bad guys than certainly the previous administration.”

She continued, “The Trump administration is committed to truth and transparency. That’s why the Attorney General and the FBI Director pledged, at the president’s direction, to do an exhaustive review of all the files related to Jeffrey Epstein’s crimes and his death. They put out a memo in conclusion of that review.”

“There was material they did not release because frankly it was incredibly graphic and contained child pornography, which is not something that is appropriate for public consumption,” she added.

“But they committed to an exhaustive investigation. That’s what they did and they provided the results of that.”

“That’s transparency,” Leavitt said.

Leavitt was also pressed about Attorney General Pam Bondi’s comments in February when she claimed she had the Epstein list “on [her] desk.”

Peter Doocy asked, “Okay, so the FBI looks at the circumstances surrounding the death of Jeffrey Epstein. According to the report, this systematic review revealed no incriminating client list. So what happened to the Epstein client list that the Attorney General said she had on her desk?”

Leavitt responded, “I think if you go back and look at what the Attorney General said in that interview, which was on your network, on Fox News—”

Doocy pushed back, “I have the quote. John Roberts said: ‘DOJ may release the list of Jeffrey Epstein’s clients, will that really happen?’ And she said, ‘It’s sitting on my desk right now to review.’”

Leavitt explained, “Yes. She was saying the entirety of all of the paperwork, all of the paper in relation to Jeffrey Epstein’s crimes, that’s what the Attorney General was referring to. And I will let her speak for that.”

“But when it comes to the FBI and the Department of Justice, they are more than committed to ensuring that bad people are put behind bars.”

So, after months of patiently waiting, the American people get a nothing burger that simply repeats the same old claims we heard under Bill Barr.

Even worse, it’s purported that this is what “transparency” and “accountability” look like.

The story went from saying the Epstein client list was “on my desk” to “actually, there is no client list.”

And the newly released video footage raises questions and, in the age of AI, proves nothing.

If there’s really nothing to hide, why does it still feel like they’re hiding everything?

And most importantly—who’s still being protected?

Thanks for reading to the end. I hope you found this timeline of events and recap helpful.

Subscribe to The Vigilant Fox

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

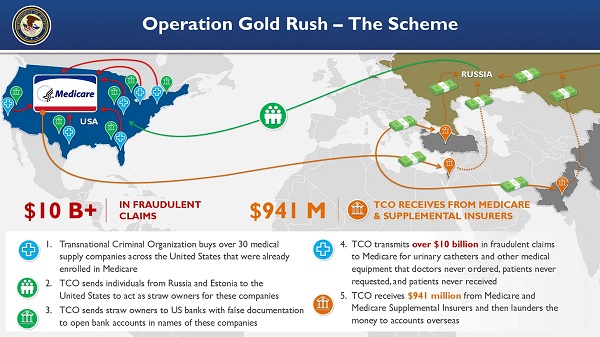

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Alberta2 days ago

Alberta2 days agoAlberta Provincial Police – New chief of Independent Agency Police Service

-

Business2 days ago

Business2 days agoWhy it’s time to repeal the oil tanker ban on B.C.’s north coast

-

International2 days ago

International2 days agoCBS settles with Trump over doctored 60 Minutes Harris interview

-

Energy2 days ago

Energy2 days agoIf Canada Wants to be the World’s Energy Partner, We Need to Act Like It

-

Alberta2 days ago

Alberta2 days agoPierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

-

Aristotle Foundation2 days ago

Aristotle Foundation2 days agoHow Vimy Ridge Shaped Canada

-

Alberta1 day ago

Alberta1 day agoAlberta uncorks new rules for liquor and cannabis

-

Canadian Energy Centre1 day ago

Canadian Energy Centre1 day agoAlberta oil sands legacy tailings down 40 per cent since 2015