Also Interesting

Medicare 101 Guide

Medicare was established in the United States as a national health insurance program for those 65 or older. Medicare Parts A, B, and D are the parts of Medicare that most people pay for individually. The program is chiefly funded through a payroll tax, though recipients are responsible for a monthly premium and cost-sharing. Medicare provides benefits to eligible beneficiaries who meet specific eligibility requirements. Participants are encouraged to enrol in a supplemental private supplementary policy through Medicare Advantage or private fee-for-service plans. The premium for these policies is paid by the beneficiary, not the federal government. Those eligible for Medicare enrolment must be at least 65 years old. Those under 65 must be permanently disabled or suffer from specific terminal illnesses.

1. What is Medicare?

Medicare is the federal healthcare program for seniors and the disabled. Its age eligibility rules are confusing, so some of those who qualify get stuck in a coverage gap that leaves them unable to afford necessary medical care. The government has been trying to help out with an updated guide on how Medicare works, but there’s still confusion about what benefits people should expect from this program. Here are some things you should know about Medicare from a healthcare perspective to make the most of your coverage and stay healthy for as long as possible.

It provides medical services to those covered by Parts A and B of the plan, which covers hospital expenses and doctor visits, respectively. Part C is Medicare Advantage (MA), which offers additional benefits such as prescription drug coverage, outpatient care, and hearing aids or eyeglasses for seniors. Those who enrol in Medicare Part D receive coverage for prescription drug costs.

2. Medicare Part A

Part A covers most of the hospital expenses for Medicare beneficiaries. The amount of coverage is based on financial needs determined by complicated formulas adjusted annually for inflation. You might wonder why this coverage gap exists in the first place, but it’s important to remember that Medicare is also a government program—i.e., you pay taxes into it, and the government gives you healthcare back. The government limits the hospital expenses covered by Part A each year.

People who have certain types of employer-sponsored insurance—such as pensions or other retirement plans—also get Medicare Part A coverage. These people are known as “dual eligible” which means they are both Medicare beneficiaries and members of an eligible group.

3. Medicare Part B

Part B covers the costs of doctors and outpatient care, such as doctor office visits and in-patient hospital stays. Medicare beneficiaries must pay a monthly premium for that coverage. Recipients also have to pay a deductible each year for any covered services. You must pay the deductible for each service before Medicare kicks in to cover the remainder.

The Social Security Administration (SSA) sets cost-of-living increases yearly. The program also covers certain preventive services with no cost sharing. You can expect to pay about $4 for your doctor visits and up to $150 for prescription drugs.

4. Medicare Part C (Medicare Advantage)

It is privatized Medicare, offered by health insurance companies and paid directly to Medicare beneficiaries. It covers various healthcare benefits and services, from screenings to hospital stays, with cost-sharing or copayments. It’s private, beneficiaries don’t have to pay anything for their plans, and neither does the government for most of those benefits.

Private insurance companies offer these plans and don’t have an annual limit on Medicare benefits. They can cover the same services as Part B and cost less because they aren’t required to follow Medicare’s formula for setting premiums and deductibles. Beneficiaries must know precisely what’s covered by each plan.

5. Medicare Part D

Part D is the prescription drug coverage offered through Medicare Part A. It covers the costs of most, but not all, prescription drugs. Some of the covered drugs are generic versions of brand-name drugs. You have to pay a monthly premium for your prescription drug coverage, and there is no cost-sharing requirement as with other parts of Medicare Part A. There’s no annual limit on the total drug costs covered, but there is a limit on what you pay out-of-pocket each year for prescriptions. Part D plans also have pre-set out-of-pocket limits that beneficiaries must pay before their plans kick in again. Beneficiaries pay their premiums and cost-sharing annually, which are set by the insurance companies offering the plans.

6. How to Enroll in Medicare?

Most people eligible for Medicare enrol in the program through their employers. If you’re self-employed, it’s wise to enroll in employer-sponsored health insurance as a dual eligible. If you’re not covered by an employer-provided plan and don’t qualify for Medicaid or a state plan, you can enroll in Medicare at any time during open enrollment. Plans often allow you to pick which parts of Medicare the federal government will cover and which ones you want to be responsible for paying out of pocket.

7. How is Medicare Paid For?

The government pays a fixed amount to beneficiaries based on their income and a sliding scale for those who are disabled or elderly. There are also premiums for MA plans. Medicare is a federal program, so it is subject to all the laws passed by Congress that regulate the establishment of insurance companies and the prosecution of fraud committed against them. Participants have access to all the information about their benefits from the Social Security Administration, which maintains a database with all Medicare enrolees’ personal information.

Medicare is a good program that helps seniors when they need it most. The government will pay its share of the costs of hospitalization or doctor visits during its 50-year lifetime. Since Medicare pays so much less than private insurance, beneficiaries often have to pay more out-of-pocket for many services, especially prescription drugs and other medical supplies.

Financial freedom means different things to different people. Some seek to clear debt or reduce working hours. Others aim to build an income stream separate from traditional employment. Betting is often seen as entertainment, but some treat it as a potential method for financial gain.

It is not a simple route. Success in betting depends on skill, patience, and clear risk control. Casual bets and chasing losses are not the same as long-term planning. Play slots and live casino online deals may attract interest, but true gains require a well-developed approach grounded in calculation,

not luck.

Some treat betting as a serious income project. Like investing, it involves monitoring markets, sticking to rules, and managing emotion. These habits shape outcomes more than any single win or loss.

The Role of Strategy and Market Choice

Building consistent returns from betting starts with discipline. Most success stories come from people who specialize in specific markets. They avoid randomness and focus on repeatable patterns. This reduces risk and allows room for structured decisions.

For some, sports betting offers the best value. Others prefer slots, roulette, or blackjack. Success in each area depends on the ability to control the betting environment. Choosing fixed budgets, setting limits, and logging results all contribute to a more sustainable system.

In Ireland and the UK, platforms now offer a wider range of services. These include analytics tools, stat-based bets, and account dashboards. Markets like Slots and table games in Ireland are especially popular among users who combine short sessions with targeted goals.

Key traits of long-term betting approaches include:

● Specialising in specific games or sports.

● Avoiding emotional or rushed bets.

● Logging every session and reviewing performance.

● Staking only a fixed portion of the bankroll per event.

Psychological Factors and Risk Limits

Financial growth through betting requires mental control. Most losses in gambling happen when people act without a plan. Emotional decisions, such as doubling stakes after a loss, often lead to poor outcomes.

Structured bettors approach the activity with neutral judgement. They view each bet as part of a larger system, not an isolated moment. This approach reduces stress and protects capital. Understanding the limits of control also helps. For example, not every market behaves the same

way each week.

Many betting platforms now offer tools that assist with self-monitoring. These include loss caps, spending summaries, and trend reports. These systems support the user but cannot replace careful thinking. Understanding the connection between strategy risk and decision making can lead to

better choices, both short and long-term.

Economic Context and the Role of Discipline

The idea of using betting as a route to financial freedom often attracts attention during economic stress. Some people look for faster income options when prices rise or wages stagnate. However, betting is not a guaranteed path. It only works when treated as a skill-based discipline, not a

shortcut.

Those who see results often treat betting like a second job. They put in regular hours for research, review performance metrics, and stick to a strict process. This removes guesswork and replaces it with control.

Having multiple sources of income is one part of building financial freedom. Betting can be one of those if it is paired with discipline, patience, and analysis. It is not passive income. It requires consistent effort and awareness.

Sensible Goals and Sustainable Progress

Success with betting should not be measured in jackpots or sudden windfalls. Small, repeatable profits are more stable. The aim is to grow a bankroll slowly, avoid major losses, and learn from every result. This mindset supports steady progress and avoids burnout.

Financial freedom through betting is possible for some. However, it depends on the user, not the platform. Planning, structure, and clear risk boundaries matter more than the type of bet. For those who view betting as a long-term activity rather than a quick fix, it can play a role in building

independence.

As always, betting should be treated with care and clear intent. When combined with focus and habit, it can support a wider plan toward financial freedom. However, without those foundations, it is more likely to create setbacks than solutions.

The Dodgers are on a roll, with nine consecutive victories against the Colorado Rockies and nine out of the last 11 overall. Max Muncy hit a grand slam and drove in six, and Yoshinobu Yamamoto pitched five scoreless innings, giving up only one hit and striking out six to go to 7-6 on the season in the finale on June 26 in Denver. More recently, in the season opener (June 25), the game was a 97 slugfest where Ohtani, Conforto, and Teoscar Hernandez, among others, put their stamp on the scoreboard, with the Dodgers taking home the game thanks to Colorado giving them the opportunity to win it late.

Top Players: Muncy/Ohtani Setting the Pace

Max Muncy has been feisty with the bat, hitting his twelfth homer of the season, his second grand slam in only three contests. Shohei Ohtani keeps producing at the plate and the mound with key home runs and a three-run triple as part of a 13-7 triumph over Washington last week, though he pitched a scoreless inning in his post-surgery outing. Teoscar Hernandez and Michael Conforto have also provided power and reliability, and provided the Dodgers with a strong offensive weapon range.

Squad Depth

The rotation has been boosted by Yoshinobu Yamamoto being the team’s ace, leading the team in April with a 1.06 ERA and still good towards the end of June, most recently against Colorado. The club has an extremely solid starting staff when healthy, with Blake Snell and Tyler Glasnow added to the mix in the offseason. Teoscar Hernandez has contributed clutch offense in the lineup during spring and early regular season after signing a three-year extension before the season began.

Looking at it through betting glasses, having both spectacular pitching and a potent offensive battery makes the Dodgers a heavy moneyline favorite and a good run line bet, particularly against inferior teams. Betting enthusiasts who want to compare the odds and get the maximum return on the Dodgers will find useful websites such as Wincomparator, a solid link to sportsbooks promotions, and a useful tool with real-time updates so that they can stay ahead of the odds.

What Next: Preview of Forthcoming Matchups

After sweeping Colorado, Los Angeles plans on concentrating on future matches at home. They have some prime match-ups with divisional rivals such as the Diamondbacks and Padres (who will provide the most difficult stretch of games in the NL West) as the season progresses. One of the most intriguing games will involve the Dodgers making a second visit to Arizona, a team that has a strong offense, including Cy Young winner Corbin Burnes.

In the meantime, recent Yankees-Dodgers previews indicated that New York would challenge L.A. with its depth as the Yankees were leading MLB in many offensive categories, and with games approaching in later summer, Dodgers fans will hope that Betts, Freeman, and Ohtani will be able to handle it in key moments in June or July.

Outlook: Second Half Positioning

As July approaches, the Dodgers appear to be in shape to continue dominating the NL West. They possess a talented pitching staff, a powerful offense that will depend on depth, and the ability to withstand injuries, which places them within the upper tier of projections, with pundits expecting them to prevail in futures markets towards another deep playoff run. So long as they remain healthy, continue to deliver in crunch time, Los Angeles is a solid step away in the season stretch run.

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

Federal fiscal anchor gives appearance of prudence, fails to back it up

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

Business1 day ago

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

COVID-192 days ago

COVID-192 days agoNew Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

-

MAiD1 day ago

MAiD1 day agoCanada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Business1 day ago

Business1 day agoWorld Economic Forum Aims to Repair Relations with Schwab

-

Alberta2 days ago

Alberta2 days agoThe permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

-

Alberta1 day ago

Alberta1 day agoAlberta’s government is investing $5 million to help launch the world’s first direct air capture centre at Innisfail

-

Business1 day ago

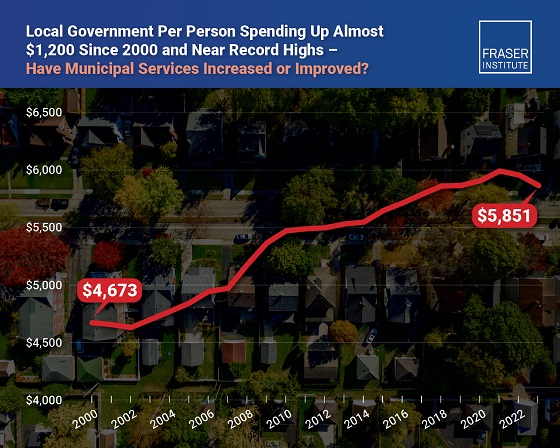

Business1 day agoMunicipal government per-person spending in Canada hit near record levels

-

Business1 day ago

Business1 day agoA new federal bureaucracy will not deliver the affordable housing Canadians need