CBDC Central Bank Digital Currency

Davos 2024: Queen Maxima advocates global digital ID for financial services, vaccine verification

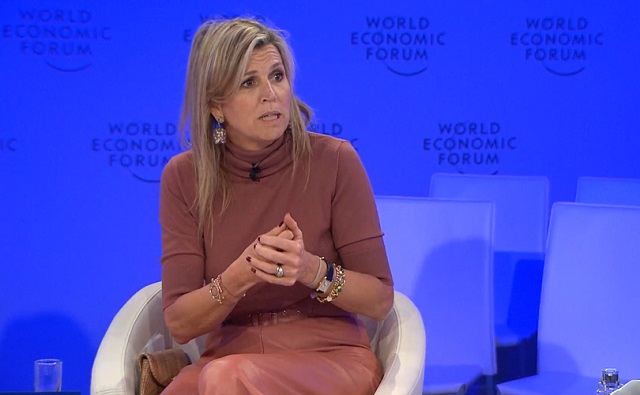

Queen Maxima of the Netherlands

From LifeSiteNews

Digital IDs are ‘good for school enrollment; it is also good for health – who actually got a vaccination or not; it’s very good actually to get your subsidies from the government,’ Queen Maxima of the Netherlands stated at the 2024 Davos summit.

Queen Maxima of the Netherlands tells the World Economic Forum (WEF) in Davos that digital ID is good for knowing “who actually got a vaccination or not” and for financial inclusion.

On Thursday the Dutch queen continued her crusade to see universal adoption of digital ID because she believes it is good for everything from opening a bank account to enrolling in school and for providing proof of vaccination, aka “vaccine passports.”

It [digital ID] is also good for school enrollment; it is also good for health – who actually got a vaccination or not; it’s very good actually to get your subsidies from the government.

Speaking at the WEF annual meeting panel entitled “Comparing Notes on Financial Inclusion,” Her Majesty said:

In order to open up an account, you need to have an ID. I have to say that when I started this job, there were actually very little countries in Africa or Latin America that had one ubiquitous type of ID, and certainly that was digital and certainly that was biometric.

We’ve really worked with all our partners to actually help grow this, and the interesting part of it is that yes, it is very necessary for financial services, but not only.

Queen Maxima of the Netherlands at WEF in Davos: [Digital ID] is very necessary for financial services, but not only – it is also good for school enrollment; it is also good for health — who actually got a vaccination or not" #DigitalID #WEF24 https://t.co/DJiO8nISih pic.twitter.com/RgYA2ahXS0

— Tim Hinchliffe (@TimHinchliffe) January 18, 2024

Beyond financial services, Queen Maxima said that digital ID was good for proving an individual’s vaccination status:

It is also good for school enrollment; it is also good for health – who actually got a vaccination or not; it’s very good actually to get your subsidies from the government.

The Dutch queen also highlighted that for the past 10 years, she had been working on developing Digital Public Infrastructure (DPI), which is a digital stack consisting of digital ID, digital payments systems like Central Bank Digital Currencies (CBDCs), and massive data sharing.

“We’ve been working in the last 10 years on a notion that we call Digital Public Infrastructure. In our experiences in different countries, to actually have these sort of things that are actually very important,” the queen told the WEF panel.

“One of these is IDs, e-signature, digital ID, so that’s extremely important, even having a QR code legislation is very important,” she added.

Last November, the United Nations and the Bill and Melinda Gates Foundation launched their 50-in-5 campaign to get 50 countries to rollout at least one DPI component within the next five years:

Digital public infrastructure (DPI) – which refers to a secure and interoperable network of components that include digital payments, ID, and data exchange systems – is essential for participation in markets and society in a digital era.

Digital Public Infrastructure (DPI) is essential for countries to improve their economies & the well-being of people.

Join us for the launch of the #50in5 initiative to discuss how building inclusive DPI can foster strong economies & equitable societies: https://t.co/SB2QDNJp2I pic.twitter.com/S01Rpxq1VP

— UNDP Digital (@UNDPDigital) October 25, 2023

As the United Nations Secretary-General’s Special Advocate for Inclusive Finance for Development, Queen Maxima has been pushing the digital ID agenda for a number of years.

Wonderful to have @UNSGSA HM Queen Máxima of the Netherlands with us at #ID4D event today highlighting the critical role of #DigitalID in inclusive development: https://t.co/bNRaIulRc7 #GoodID #WBGMeetings pic.twitter.com/nNCO8qP50q

— World Bank Digital Development (@WBG_DigitalDev) April 12, 2019

#UNSGSA Queen Máxima delivered the keynote speech at today’s @WorldBank #ID4D event on inclusive digital ID for a resilient recovery from #COVID-19. Read it here → https://t.co/vD9uYPtA7P #financialinclusion pic.twitter.com/8W2tk2ImIY

— UN SG's Special Advocate Queen Máxima (@UNSGSA) October 21, 2020

Vaccine passports, by their very nature, serve as a form of digital identity, according to the WEF.

And the WEF envisions digital identity being linked to everything from financial services and healthcare records to travel, mobility, and digital governance.

A WEF report on “Reimagining Digital ID” published in June 2023, says:

- “Digital ID may weaken democracy and civil society.”

- “The greatest risks arising from digital ID are exclusion, marginalization and oppression.”

- Requiring any form of ID risks exacerbating fundamental social, political and economic challenges as conditional access of any kind always creates the possibility of discrimination and exclusion.”

This digital identity determines what products, services and information we can access – or, conversely, what is closed off to us

Queen Maxima is also a staunch advocate for Central Bank Digital Currencies (CBDCs), which cannot operate without a digital ID.

According to the Bank for International Settlements (BIS) Annual Economic Report 2021:

The most promising way of providing central bank money in the digital age is an account-based CBDC built on digital ID with official sector involvement…

Identification at some level is hence central in the design of CBDCs. This calls for a CBDC that is account-based and ultimately tied to a digital identity.

#CBDCs can help overcome some barriers facing the unbanked, write Agustín Carstens and H.M. Queen Máxima of the Netherlands, the United Nations Secretary-General’s Special Advocate for Inclusive Finance for Development @UNSGSA @koninklijhuis @ProSyn https://t.co/C8VXHvDSZ2 pic.twitter.com/aTqJdeTCa2

— Bank for International Settlements (@BIS_org) April 18, 2022

At this very moment, governments and central banks all over the world are exploring how to implement Central Bank Digital Currencies that are inextricably linked with pegging every citizen to a digital identity.

A CBDC adds another layer to digital ID, in that it can program permissions on purchases.

Speaking at the WEF’s 14th Annual Meeting of the New Champions, aka “Summer Davos,” in Tianjing, China, last year, Cornell University professor Eswar Prasad explained that governments could program CBDCs to restrict undesirable purchases and set expiry dates.

You could have a potentially […] darker world where the government decides that units of central bank money can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort.

"You could have a potentially […] darker world where the government decides that [CBDC] can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort": Eswar Prasad, WEF #AMNC23 pic.twitter.com/KkWgaEWAR5

— Tim Hinchliffe (@TimHinchliffe) June 28, 2023

The theme of this year’s WEF Annual Meeting is “Rebuilding Trust.”

Kicking off the meeting this week in his welcome address, WEF founder Klaus Schwab appointed himself and the Davos crowd “trustees” over humanity’s future.

Reprinted with permission from The Sociable.

Central Bank of Bahrain governor Khalid Humaidan

From LifeSiteNews

When asked how he would convince people that CBDCs would be a trusted medium of exchange, Bahrain’s central bank governor said that COVID made the digital transformation ‘something of a requirement’ that had ‘very little resistance.’

Central bank digital currencies (CBDCs) will hopefully replace physical cash and become fully digital, a central banker tells the World Economic Forum (WEF).

Speaking at the WEF Special Meeting on Global Collaboration, Growth and Energy Development on Sunday, Central Bank of Bahrain governor Khalid Humaidan told the panel “Open Forum: The Digital Currencies’ Opportunity in the Middle East” that one of the goals of CBDC was to replace cash, at least in Bahrain, and to go “one hundred percent digital.”

Humaidan likened physical cash to being an antiquated “analogue” technology and that CBDC was the digital solution that would hopefully replace cash:

"We're probably going to stop calling it central bank digital currency [CBDC]. It's going to be a digital form of cash, and at some point in time hopefully we will be able to be 100% digital": Central Bank of Bahrain Governor Khalid Humaidan to the WEF https://t.co/Pspr0M1Uuq pic.twitter.com/N5aOkCpzh1

— Tim Hinchliffe (@TimHinchliffe) April 29, 2024

“I thank this panel and this opportunity. It forced me to refine my thoughts and opinions where I’m at a place comfortably now that I’m ready to verbalize what I think about CBDC,” said Humaidan.

If we think cash is the analogue and digital currency is the form of digital – CBDC is the digital form of cash – today, clearly we’re in a hybrid situation; we’re using both.

We know in the past when it comes to cash, central bankers were very much in control with all aspects of cash, and now we’re comfortable to the point where the private sector plays a big role in the printing of the cash, in the distribution of the cash, and with the private sector we use interest rates to manage the supply of cash.

The same thing is likely to happen with CBDC. Yes, the central bank will have a role, but at some point in time – the same way we don’t call it ‘central bank cash’ – we’re probably going to stop calling it central bank digital currency.

“It’s going to be a digital form of the cash, and at some point in time hopefully we will be able to be one hundred percent digital,” he added.

When asked how he would convince people that CBDC would be a trusted medium of exchange, Bahrain’s central bank governor said that people were already used to it and that COVID made the digital transformation “necessary” and “something of a requirement” that had “very little resistance.”

"There's less use of cash […] The transition to fully digital is not going to be a stretch […] People are used to it […] Its adoption rates increased because of COVID […] There is very little resistance": Central Bank of Bahrain Governor Khalid Humaidan to the WEF on CBDC pic.twitter.com/zB7nJAi48G

— Tim Hinchliffe (@TimHinchliffe) April 29, 2024

“Right now, many of our payments are digital. The truth is, I said that we’re in a hybrid model; there’s less and less use of cash,” said Humaidan.

I think from predominantly digital with a little physical, I think the transition to fully digital is not going to be a stretch.

People are used to it, people have engaged in it and certain circumstances did help. Its adoption rates increased because of COVID.

“This is where contactless started to become something of a necessity, something of safety, something of a requirement, and because of that there is very little resistance; trust is already there,” he added.

"Is it [digital euro] going to be as private as cash? No. A digital currency will never be as anonymous and as protecting of privacy in many respects as cash, which is why cash will always be around": Christine Lagarde, BIS Innovation Summit, March 2023 #CBDC pic.twitter.com/BLMVOPax6a

— Tim Hinchliffe (@TimHinchliffe) April 11, 2023

Meanwhile, European Central Bank president Christine Lagarde has been going around the world telling people that the digital euro CBDC would not eliminate cash, and that cash would always be an option.

Speaking at the Bank for International Settlements (BIS) Innovation Summit in March 2023, Lagarde said that a digital currency will never be as anonymous as cash, and for that reason, cash will always be around.

“Is it [digital euro] going to be as private as cash? No,” she said.

A digital currency will never be as anonymous and as protecting of privacy in many respects as cash, which is why cash will always be around.

If people want to use cash in some countries or in some transactions, cash should be available.

“A digital currency is an alternative, is another means of payment and will not provide exactly the same level of privacy and anonymity as cash, but will be pretty close in terms of complete neutrality in relation to the data,” she added.

A WEF Agenda blog post from September, 2017, lists the “gradual obsolescence of paper currency” as being “characteristic of a well-designed CBDC.”

"You could have a potentially […] darker world where the government decides that [CBDC] can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort": Eswar Prasad, WEF #AMNC23 pic.twitter.com/KkWgaEWAR5

— Tim Hinchliffe (@TimHinchliffe) June 28, 2023

Last year at the WEF’s 14th Annual Meeting of the New Champions, aka “Summer Davos,” in Tianjing, China, Cornell University professor Eswar Prasad said that “we are at the cusp of physical currency essentially disappearing,” and that programmable CBDCs could take us to either a better or much darker place.

“If you think about the benefits of digital money, there are huge potential gains,” said Prasad, adding, “It’s not just about digital forms of digital currency; you can have programmability – units of central bank currency with expiry dates.

You could have […] a potentially better – or some people might say a darker world – where the government decides that units of central bank money can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort, and that is very powerful in terms of the use of a CBDC, and I think also extremely dangerous to central banks.

The WEF’s Special Meeting on Global Collaboration, Growth and Energy Development took place from April 27-29 in Riyadh, Saudi Arabia.

“Saudi Arabia’s absolute monarchy restricts almost all political rights and civil liberties,” according to D.C.-based NGO Freedom House.

In the kingdom, “No officials at the national level are elected,” and “the regime relies on pervasive surveillance, the criminalization of dissent, appeals to sectarianism and ethnicity, and public spending supported by oil revenues to maintain power.”

Reprinted with permission from The Sociable.

From the Daily Caller News Foundation

From the Daily Caller News Foundation

Central bank digital currencies (CBDC) are a threat to liberty.

Sixty-eight countries, including communist China, are exploring the possibility of issuing a CBDC. CBDCs are essentially government-sponsored cryptocurrencies pegged to the value of a national currency that allow for real-time payments.

The European Union has a digital euro CBDC pilot program, and all BRICS nations (Brazil, Russia, India, China and South Africa) are working to stand up CBDCs. China’s CBDC pilot, the largest in the world, is being used by 260 million individuals.

While faster payments are a positive for markets and economic growth, CBDCs present major risks. They would allow governments to meticulously monitor transactions made by their citizens, and CBDCs open the door for government planners to limit the types of transactions made.

Power corrupts, and no government should have that level of control. No wonder China and other authoritarian regimes around the globe are eager to implement a CBDC.

Governments that issue CBDCs could prohibit the sale or purchase of certain goods or services and more easily freeze and seize assets. But that would never happen in the U.S, right? Don’t be so certain.

Take a look at recent events in our neighbor to the north. The government of Canada shut down bank accounts and froze assets of Canadian citizens protesting the COVID-19 vaccination in Ottawa during the winter of 2022. With a CBDC, authoritarian actions of this kind would be even easier to execute.

To make matters worse, the issuance of a CBDC by the Federal Reserve, the U.S.’s central bank, has the potential to undermine the existing banking system. The exact ramifications of what a CBDC would mean to the banking sector are unclear, but such a development could position the Fed to offer banking services directly to American businesses and citizens, undercutting the community banks, credit unions, and other financial institutions that currently serve main street effectively.

The Fed needs to stay out of the banking business – it’s having a hard enough time achieving its core mission of getting inflation under control. A CBDC would open the door for the Fed to compete with the private sector, undercutting economic growth, innovation, and financial access in the process.

Fed Chair Jerome Powell has testified before Congress that America’s central bank would not issue a CBDC without express approval from Congress, but the Fed has studied CBDCs extensively.

For consumers who want the ability to make real-time payments internationally, CBDCs are not the answer. Stablecoins offer a commonsense private sector solution to this market demand.

Stablecoins are a type of cryptocurrency pegged to the value of a certain asset, such as the U.S. dollar. If Congress gets its act together and creates a regulatory framework for stablecoins, many banks, cryptocurrency firms, and other innovative private sector entities would issue dollar-pegged stablecoins. These financial instruments would allow for instantaneous cross-border payments for market participants who find that service of value.

Stablecoins are the free market response to CBDCs. They offer the benefits associated with the technology without the privacy risk, and they would likely enhance, not disrupt, the existing banking sector.

Representatives Patrick McHenry (R-N.C.) and French Hill (R-Ark.) have done yeoman’s work advancing quality, commonsense stablecoin legislation in the House of Representatives, and the Senate needs to move forward on this issue.

Inaction by Congress will force innovators overseas and put the U.S. at a competitive disadvantage. It would also help the Fed boost the case for a CBDC that will undermine liberty and open the door to government oppression.

Tommy Tuberville is a Republican from Alabama serving in the United States Senate. He is a member of the Senate Agriculture Committee, which plays a key role in overseeing emerging digital assets markets.

UN plastics plans are unscientific and unrealistic

The Teams Are Set for World War III

Support a young reader through the Tim Hortons Smile Cookie campaign

Alberta threatens to fight Trudeau government restrictions on Canada’s plastics industry

-

John Stossel1 day ago

John Stossel1 day agoWhy Biden’s Just Wrong: NO ONE “Knows How to Make Government Work.”

-

Business2 days ago

WEF panelist suggests COVID response accustomed people to the idea of CBDCs

-

Automotive2 days ago

Automotive2 days agoCanadian interest in electric vehicles falls for second year in a row: survey

-

COVID-192 days ago

COVID-192 days agoPeckford: Hallelujah! Supreme Court of Canada to hear Newfoundland and Labrador charter case

-

illegal immigration1 day ago

illegal immigration1 day agoFlight Docs Reveal Which Cities Are Receiving Migrants Under Biden’s Parole Program

-

COVID-192 days ago

COVID-192 days agoFormer Canadian lawmaker has no regrets about refusing COVID shot despite losing his job

-

Alberta2 days ago

Alberta2 days agoCanada’s postal service refuses to help with Trudeau’s gun ban buyback program: report

-

COVID-192 days ago

COVID-192 days agoStates move to oppose WHO’s ‘pandemic treaty,’ assert states’ rights