CBDC Central Bank Digital Currency

Davos 2024: Queen Maxima advocates global digital ID for financial services, vaccine verification

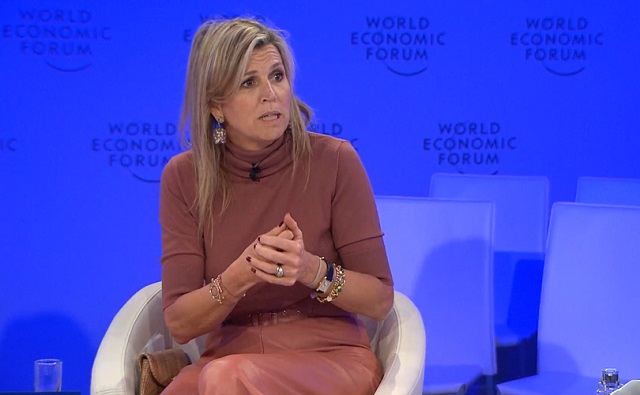

Queen Maxima of the Netherlands

From LifeSiteNews

Digital IDs are ‘good for school enrollment; it is also good for health – who actually got a vaccination or not; it’s very good actually to get your subsidies from the government,’ Queen Maxima of the Netherlands stated at the 2024 Davos summit.

Queen Maxima of the Netherlands tells the World Economic Forum (WEF) in Davos that digital ID is good for knowing “who actually got a vaccination or not” and for financial inclusion.

On Thursday the Dutch queen continued her crusade to see universal adoption of digital ID because she believes it is good for everything from opening a bank account to enrolling in school and for providing proof of vaccination, aka “vaccine passports.”

It [digital ID] is also good for school enrollment; it is also good for health – who actually got a vaccination or not; it’s very good actually to get your subsidies from the government.

Speaking at the WEF annual meeting panel entitled “Comparing Notes on Financial Inclusion,” Her Majesty said:

In order to open up an account, you need to have an ID. I have to say that when I started this job, there were actually very little countries in Africa or Latin America that had one ubiquitous type of ID, and certainly that was digital and certainly that was biometric.

We’ve really worked with all our partners to actually help grow this, and the interesting part of it is that yes, it is very necessary for financial services, but not only.

Queen Maxima of the Netherlands at WEF in Davos: [Digital ID] is very necessary for financial services, but not only – it is also good for school enrollment; it is also good for health — who actually got a vaccination or not" #DigitalID #WEF24 https://t.co/DJiO8nISih pic.twitter.com/RgYA2ahXS0

— Tim Hinchliffe (@TimHinchliffe) January 18, 2024

Beyond financial services, Queen Maxima said that digital ID was good for proving an individual’s vaccination status:

It is also good for school enrollment; it is also good for health – who actually got a vaccination or not; it’s very good actually to get your subsidies from the government.

The Dutch queen also highlighted that for the past 10 years, she had been working on developing Digital Public Infrastructure (DPI), which is a digital stack consisting of digital ID, digital payments systems like Central Bank Digital Currencies (CBDCs), and massive data sharing.

“We’ve been working in the last 10 years on a notion that we call Digital Public Infrastructure. In our experiences in different countries, to actually have these sort of things that are actually very important,” the queen told the WEF panel.

“One of these is IDs, e-signature, digital ID, so that’s extremely important, even having a QR code legislation is very important,” she added.

Last November, the United Nations and the Bill and Melinda Gates Foundation launched their 50-in-5 campaign to get 50 countries to rollout at least one DPI component within the next five years:

Digital public infrastructure (DPI) – which refers to a secure and interoperable network of components that include digital payments, ID, and data exchange systems – is essential for participation in markets and society in a digital era.

Digital Public Infrastructure (DPI) is essential for countries to improve their economies & the well-being of people.

Join us for the launch of the #50in5 initiative to discuss how building inclusive DPI can foster strong economies & equitable societies: https://t.co/SB2QDNJp2I pic.twitter.com/S01Rpxq1VP

— UNDP Digital (@UNDPDigital) October 25, 2023

As the United Nations Secretary-General’s Special Advocate for Inclusive Finance for Development, Queen Maxima has been pushing the digital ID agenda for a number of years.

Wonderful to have @UNSGSA HM Queen Máxima of the Netherlands with us at #ID4D event today highlighting the critical role of #DigitalID in inclusive development: https://t.co/bNRaIulRc7 #GoodID #WBGMeetings pic.twitter.com/nNCO8qP50q

— World Bank Digital Development (@WBG_DigitalDev) April 12, 2019

#UNSGSA Queen Máxima delivered the keynote speech at today’s @WorldBank #ID4D event on inclusive digital ID for a resilient recovery from #COVID-19. Read it here → https://t.co/vD9uYPtA7P #financialinclusion pic.twitter.com/8W2tk2ImIY

— UN SG's Special Advocate Queen Máxima (@UNSGSA) October 21, 2020

Vaccine passports, by their very nature, serve as a form of digital identity, according to the WEF.

And the WEF envisions digital identity being linked to everything from financial services and healthcare records to travel, mobility, and digital governance.

A WEF report on “Reimagining Digital ID” published in June 2023, says:

- “Digital ID may weaken democracy and civil society.”

- “The greatest risks arising from digital ID are exclusion, marginalization and oppression.”

- Requiring any form of ID risks exacerbating fundamental social, political and economic challenges as conditional access of any kind always creates the possibility of discrimination and exclusion.”

This digital identity determines what products, services and information we can access – or, conversely, what is closed off to us

Queen Maxima is also a staunch advocate for Central Bank Digital Currencies (CBDCs), which cannot operate without a digital ID.

According to the Bank for International Settlements (BIS) Annual Economic Report 2021:

The most promising way of providing central bank money in the digital age is an account-based CBDC built on digital ID with official sector involvement…

Identification at some level is hence central in the design of CBDCs. This calls for a CBDC that is account-based and ultimately tied to a digital identity.

#CBDCs can help overcome some barriers facing the unbanked, write Agustín Carstens and H.M. Queen Máxima of the Netherlands, the United Nations Secretary-General’s Special Advocate for Inclusive Finance for Development @UNSGSA @koninklijhuis @ProSyn https://t.co/C8VXHvDSZ2 pic.twitter.com/aTqJdeTCa2

— Bank for International Settlements (@BIS_org) April 18, 2022

At this very moment, governments and central banks all over the world are exploring how to implement Central Bank Digital Currencies that are inextricably linked with pegging every citizen to a digital identity.

A CBDC adds another layer to digital ID, in that it can program permissions on purchases.

Speaking at the WEF’s 14th Annual Meeting of the New Champions, aka “Summer Davos,” in Tianjing, China, last year, Cornell University professor Eswar Prasad explained that governments could program CBDCs to restrict undesirable purchases and set expiry dates.

You could have a potentially […] darker world where the government decides that units of central bank money can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort.

"You could have a potentially […] darker world where the government decides that [CBDC] can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort": Eswar Prasad, WEF #AMNC23 pic.twitter.com/KkWgaEWAR5

— Tim Hinchliffe (@TimHinchliffe) June 28, 2023

The theme of this year’s WEF Annual Meeting is “Rebuilding Trust.”

Kicking off the meeting this week in his welcome address, WEF founder Klaus Schwab appointed himself and the Davos crowd “trustees” over humanity’s future.

Reprinted with permission from The Sociable.

corbettreport.com

But it’s another thing altogether for those conspirators to follow through on that psyop and actually achieve their desired end goal: the erection of the biosecurity state.

For those of us who managed to maintain our sanity over the last five years, the question is not whether COVID was a psyop—the answer to that question was obvious from the start—but whether the COVID conspirators have accomplished their objectives.

So, where do we stand in 2025? Did the COVID scamsters win?

Lockdowns

One of the intended effects of the COVID psyop was to take the concept of lockdowns and social distancing from the realm of obscure authoritarian fantasy to stone-cold reality.

As I pointed out in my 2020 video on “What NO ONE is Saying About The Lockdowns,” the idea of using school shutdowns, mandatory lockdowns and social distancing as pandemic prevention measures was first floated by Albequerque high school student Laura Glass for her local science fair project. (For those who are interested, she won third place!)

Prior to 2020, the notion of locking down healthy populations to prevent the spread of disease was still pie-in-the-sky fantasy. No government had seriously attempted to impose lockdowns or social distancing on a mass scale and the very thought of mass quarantines and government-imposed, electronically monitored lockdowns would have been laughed off as conspiracy paranoia.

On the other side of the 2020 divide, however, lockdowns became not only thinkable but an essential tool in the biosecurity state’s toolbelt.

Since 2020, for example, we have seen the extent to which lockdowns penetrated the popular imagination reflected in such ideas as “climate lockdowns.” After all, if locking people in their homes worked for a planetary health emergency, why not use it for a planetary climate emergency?

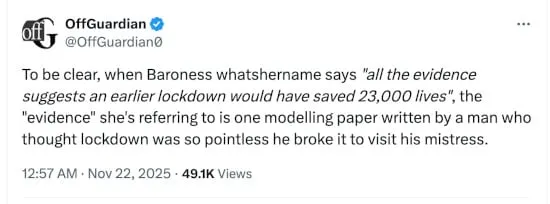

Yet another example of the mindset shift that has occurred over the past five years arrived last week when the UK Covid-19 Inquiry delivered its verdict that the lockdowns the UK government imposed during the scamdemic were “too little, too late“ and that they could have saved 23,000 lives by locking down earlier.

This is, of course, nonsense. Actually, it’s worse than nonsense; it’s nonsense based on made-up numbers from a known liar. As Off-Guardian point out in their (shadow-banned) tweet on the subject:

For those who don’t know, the tweet is referring to this passage from the inquiry’s report:

Professor Ferguson told the Inquiry that in later work which analyzed the impact of restrictions in England: “we explicitly modelled the counterfactual scenario of moving the lockdown of 23rd March back to 16th March, and estimated mortality … would have been reduced by 48%.“ That could have equated to a reduction in deaths in England from 48,600 to approximately 25,600 in the first wave up to 1 July 2020.

“Professor Ferguson” is, lest we forget, Neil Ferguson, the “virus modeller” (or should that be the “Liberal Lysenko“?) from Imperial College London who produced the computer model suggesting that 500,000 Britons were destined for the grave unless the UK government imposed a national lockdown. Ferguson has since walked back that claim and now denies calling for a lockdown at all, but it should be kept in mind that his about-face came after he was caught breaking the UK lockdown restrictions to carry on an affair with his married lover.

This is also the same Neil Ferguson who used his amazing “virus modeling” powers to predict 50,000 deaths from the UK’s 2002 mad cow outbreak (actual number of deaths: 177) and up to 200 million deaths from a potential, theoretical bird flu outbreak (which has yet to arrive).

Ferguson’s projection of what could have resulted if the government had locked down faster and earlier suffers from the same “garbage in, garbage out” tomfoolery as the Club of Rome’s environmental apocalypticism. Keep in mind that the number of people who would supposedly have been saved by a quicker UK lockdown is based on a fundamentally flawed input: the number of people who the UK government assert died of COVID. Those of us who called out the scam from the start have been noting for years that these COVID death tolls are statistical chicanery, since they rely on the fraudulent claim that everyone who died with COVID—as measured by the scientifically meaningless PCR test—had in fact died of COVID.

In other words, Ferguson’s numbers are plucked out of thin air and aren’t worth the paper they’re written on. They should not be taken seriously by anyone, whatever their opinion on the efficacy of lockdowns.

But, as usual, the damage has been done. The controlled establishment media has run their headlines about the lives that could have been saved by earlier lockdowns, and the type of people who still get their news from these mockingbird repeaters will now be more certain than ever that social distancing and quarantining populations is the right thing to do in the event of a declared health emergency.

Chalk that one up as a win for the COVID scamsters.

QR Codes, Vaccine Passports and Digital ID

Even more important to the would-be medical tyrants than the normalization of lockdowns and social distancing, however, was the creation of the technological infrastructure upon which the biosecurity state is enabled. This digital infrastructure includes:

- the QR codes that people were habituated into scanning before being allowed access to or egress from various quarantine zones;

- the vaccine passports that were used to assess compliance with vaccine mandates; and

- the various contract tracing apps and self-quarantine apps that were employed to keep track of citizens as they moved from place to place.

If you’ve read about my recent experience trying to order breakfast in Malaysia, you’ll know that, once again, the COVIDians have been remarkably successful in achieving their objectives. As I found out during that Malaysian sojourn, scanning QR codes to access online menus and using cashless payment systems to pay for purchases is becoming so normalized in certain parts of the world that it can be difficult to so much as order breakfast without a smartphone and cellular service. Indeed, the smartphone has become a virtual prerequisite for participation in the public space, and it was the scamdemic that allowed the shift to 100% dependence on smartphones to take place.

One recent demonstration of this smartphone requirement for participation in public life came from an email I received this week from a Corbett Reporter in Canada. He was trying to send a registered letter to the US via Canada Post but was informed that his addressed envelope alone would no longer do. Instead, he now had to fill out an online form and print off a special tracking number in order to mail the item. Not owning a smartphone, he was out of luck. He would have to go home, fill out the online forms on his desktop, print out the paperwork and bring it back to the post office. He opted not to send the letter, vowing instead to never again mail anything to the US.

Living in Japan as I do, the only surprising part of his story is that Canada held off making this change in their postal system for so long. Japan Post implemented the same electronic system for international mail four years ago. Of course, at that time the COVID border closures and postal delivery issues were used as the excuse for the intrusive new policy. But, given that country after country is now bringing in similar measures, the reality is clear: the change to a computer-dependent postal system is a global directive that was pushed, using the cover of COVID contagion, during the scamdemic. The end result is that one must either carry their smartphone with them at all times or spend extra time at home filling out online forms and printing off paperwork if they want to send mail internationally.

Of course, all of these technological “upgrades” to our daily experience—from the smartphone postal system to the QR code menus to the cashless payment systems—serve the same agenda. They are meant to pave the way toward the apotheosis of the biosecurity state: the consolidation of all our information into a single government-issued digital identity app. Soon, we will be giving the government real-time access to all of our daily movements, transactions and interactions and will be signing in with government-issued digital credentials everywhere we go online and in real life.

In the event of the next scamdemic, the scammers will hardly have to do anything at all. The QR code check-ins, vaccine passport checks and cashless payments will already be so much a part of our daily life that we’ll hardly notice any new scamdemic-related restrictions on our activities.

That’s another win for Team COVID. But they’re not done yet.

Clot shots

Another key goal of the scamdemic, of course, was to fast track government approval of mRNA and DNA “vaccine” technologies.

We know this, of course, because the conspirators told us as much in their own words. Who can forget the October 2019 Milken Institute-hosted discussion on the “Universal Flu Vaccine“? In case you have forgotten, that was the conference in which such luminaries as Tony Fauci and Rick Bright lamented that the poor, beleaguered Big Pharma corporations were going to have to spend billions of dollars and at least a decade of hard work proving the safety and efficacy of their DNA/mRNA injection techniques…unless some health emergency arose to justify the emergency approval of these experimental technologies.

So, were Fauci and Bright and their co-conspirators successful in their fast-tracking task? Did they circumvent a decade of regulatory approval work for their Big Pharma buddies? Well, if the point was to invoke a health emergency to get emergency approval for these clot shot monstrosities, then we need look no further than “Operation Warp Speed” for proof that the COVID conspirators were, in fact, remarkably successful.

And let’s never forget that Trump considers the Warp Speed MAGA jabs to be “one of the greatest things ever in politics or in the military!”

Lest there be any doubt about Trump’s devotion to this technology, let’s not forget that he hosted an event launching his $500 billion AI-pushing “Stargate” project on his third day in office earlier this year, at which Larry Ellison discussed using AI to develop personalized mRNA cancer vaccines. And just two months ago, Bill Gates used his place of honor at a White House banquet to boast that he and Trump were discussing “vaccines and gene editing” in their joint effort to “tak[e] American innovation to the next level.”

But this isn’t just about Trump, and it isn’t just about what’s happening in the US. This is a worldwide agenda. And, if this smattering of headlines from the past few months is any indication, the COVID era has given a gigantic shot in the arm (pun intended) to the clot shot “vaccine” manufacturers:

Experimental mRNA flu vaccine shows superior efficacy against symptomatic illness (just don’t ask about the side effects)

COVID Vaccine Tech May Reduce Disabilities in Snakebite Victims

Personalized mRNA Vaccines Will Revolutionize Cancer Treatment—If Funding Cuts Don’t Doom Them

The Dawn of Personalized DNA Vaccines

And, exactly in line with my reporting in Who Is Bill Gates? there’s this recent report

New Gates-Funded Microneedle Patch Implant Installs Both mRNA and Quantum Dot Markings Into the Body

Yes, it’s safe to say we are now ensconced in the era of genetic intervention masquerading as “vaccines.”

That’s another win for the WHO mafia.

Mission Accomplished?

I could go on. I haven’t even mentioned yet the passage of the WHO’s pandemic treaty or how its provisions actually encourage the work of the bioweapons industry…in the name of “defense” against such weapons, naturally. (A “poor man’s nuke,” anyone?)

But you get the point. Just as it’s difficult to deny that the COVID scamdemic was the biggest psyop of our lifetime, it’s equally difficult to deny that the perpetrators of that scam have been remarkably successful, achieving so many of their 2030 Agenda items in one fell swoop.

So, did the conspirators win?

The answer to this question is even more important than it might seem at first glance. History, as we know, is written by the winners, so if the WHO goons and their string-pullers and paymasters did indeed win, then our grandchildren will grow up learning about the terrible plague that threatened to wipe out the global population in 2020. They’ll read about how some crazy kooks resisted the loving lockdowns of the government and warned against the life-saving vaccines. They’ll truly believe we were only saved by the skin of our teeth thanks to our benevolent masters imposing lockdowns, mRNA clot shots and masks on us all (though they should have locked us down sooner and harder!).

This is why spreading the truth about these events is so vital. We must not let the lies stand. If these lies are written into the history books, then the conspirators really have won.

If you agree with me, share this report (or at least the evidence linked herein) with someone you love.

Like this type of essay? Then you’ll love The Corbett Report Subscriber newsletter, which contains my weekly editorial as well as recommended reading, viewing and listening.

If you’re a Corbett Report member, you can sign in to corbettreport.com and read the newsletter today.

Not a member yet? Sign up today to access the newsletter and support this work.

Are you already a member and don’t know how to sign in to the website? Contact me HERE and I’ll be happy to help you get logged in!

Subscribe to The Corbett Report

From LifeSiteNews

By David James

The aim is to have the digital euro fully in place by 2030 in order to move Europe fully into the United Nations’ post-capitalist system described in Agenda 2030.

It always pays to scrutinize closely the comments of financial elites because they are rarely honest about their intentions. An instance is the comments of Christine Lagarde, president of the European Central Bank (ECB) who said there will be a vote next month in the European Union parliament on the next step toward creating a digital euro, which would be a central bank digital currency (CBDC).

A central bank digital currency is money issued by the central bank in digital form as opposed to digital credit issued by banks, which is the dominant form of money in Western societies. She claims that it will mean more freedom for Europeans and that there is nothing to fear.

Lagarde anticipates launching the digital euro in about 18 months. The aim is to have it fully in place by 2030 in order to move Europe fully into the United Nations’ post-capitalist system that is described in Agenda 2030.

Lagarde’s blandishments about what the digital euro represents do not survive close examination. She acknowledged that the main concern of the population is the privacy implications, claiming the ECB is looking at a technology that will offer protections. The private banks, she said, will apply the “rules of scrutiny” that already have access to the transactions. “We are not interested in the data. The private banks are interested in the data.”

Lagarde also said that the “people have dictated” the transition to a digital euro. This looks dubious. Neither the EU Commission nor the ECB is democratically elected. And if the main concern people have with a CBDC is privacy, then why would people prefer it over cash, which is immune to scrutiny? It is not as if a digital euro would satisfy an unmet need. Digital money – credit and online transactions – is already freely available in the banking system.

The ECB is also speaking out of both sides of its mouth, saying on one hand that the digital euro will only complement cash and on the other that cash will be eliminated.

Lagarde made it clear that the aim is to phase out cash completely. Agenda 2030, she claims, “can only be enforced in a cashless economy.” Why? What is it about cash that makes environmental policies impossible to implement? The answer is surely that a digital euro is needed to control people’s behavior, forcing them to comply with environmental rules.

Previous comments by central bankers suggest there is good reason for Europeans to be extremely suspicious. In 2021, the general manager of the Bank for International Settlements, Agustín Carstens, said: “We don’t know who’s using a $100 bill today and we don’t know who’s using a 1,000-peso bill today. The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and also we will have the technology to enforce that.”

The pretext for the financial power play is climate change and the push toward net zero. A European CBDC is not, as implied by Lagarde, the creation of a new digital monetary mechanism. As economist Richard Werner points out, that already exists – credit and debit cards, for example. The significance of a digital euro is that it threatens the banking system.

A CBDC, like cash, has no interest rate on it. So why would people continue to use credit produced by private entities such as banks or credit card companies – currently over 95 percent of the money supply – on which they have to pay interest? As the Reserve Bank of New Zealand noted, CBDCs have the potential to destroy private banks.

That problem does not seem to concern the ECB, however. Indeed, fundamentally altering the banking system may be what they are aiming for. Lagarde said “climate compliance” will become a core element of bank supervision, not a separate initiative, “because climate change presents significant, material financial risks to banks and the entire financial system.”

The ECB’s supervision will mandate that banks integrate the management of climate-related and environmental risks into their existing risk management processes, particularly through new prudential transition planning requirements under what is called CRD VI. European banking, it seems, will no longer be defined by profitability and fiscal soundness but also by the politics of climate change.

The slipperiness of the ECB‘s arguments point to a much darker ambition. Werner says when CBDCs are connected to digital IDs “we are talking about the most totalitarian control system in human history … it gives you as a controller complete visibility on what everyone is doing, every transaction.

“The monitoring is only one aspect. These CBDCs are programmable and you can use big data algorithms, which they sell to us as artificial intelligence, in order to have rules about who can buy what and for what purpose, at what time and at what place – and therefore control all your movement. In the history of dictatorships, there never has been such a powerful control tool.”

There is a flaw, though, in the ECB’s push to change Europe’s financial architecture that may prove fatal to its ambitions. The EU and ECB do not have genuine central control. When the euro was established in 1998, the only way Germany was able to join was on the condition there was no consolidation of the government debt. So, although the ECB notionally sets interest rates for the zone, government debt is held at the national level and each country’s interest rate differs.

The ECB is thus a central bank in name only, unlike the U.S. Federal Reserve, or for that matter most country’s central banks, that oversee their national government debt. A European nation can choose to exit the EU, and each has to have its own monetary policy in spite of the ECB setting a uniform rate.

The push to create a digital euro is most likely an attempt to deal with these contradictions, but at best it will be a makeshift solution and it will take very little for it to fall apart. Disintegration of the European Union, and the common currency, is not out of the question.

Meanwhile, the U.S. is going in the opposite direction. In July, the U.S. House of Representatives passed the Anti-CBDC Surveillance State Act, which prevents the Federal Reserve from issuing a retail CBDC directly to individuals.

European debt is becoming increasingly parlous, especially in France where there have even been suggestions that there might need to be assistance from the International Monetary Fund. Italy’s debt, which is 138 percent of GDP, is also problematic. Lagarde is hoping for a rollout of the digital euro in 2027 and completion in 2030. But the Euro zone, and the ECB that oversees it, may not last that long.

Georgia county admits illegally certifying 315k ballots in 2020 presidential election

ICYMI: Largest fraud in US history? Independent Journalist visits numerous daycare centres with no children, revealing massive scam

While Western Nations Cling to Energy Transition, Pragmatic Nations Produce Energy and Wealth

Alberta project would be “the biggest carbon capture and storage project in the world”

-

Energy18 hours ago

Energy18 hours agoRulings could affect energy prices everywhere: Climate activists v. the energy industry in 2026

-

Digital ID19 hours ago

Digital ID19 hours agoThe Global Push for Government Mandated Digital IDs And Why You Should Worry

-

International2 days ago

International2 days agoTrump confirms first American land strike against Venezuelan narco networks

-

Bruce Dowbiggin17 hours ago

Bruce Dowbiggin17 hours agoThe Rise Of The System Engineer: Has Canada Got A Prayer in 2026?

-

International18 hours ago

International18 hours agoMaduro says he’s “ready” to talk

-

Business2 days ago

Business2 days agoHow convenient: Minnesota day care reports break-in, records gone

-

Business2 days ago

Business2 days agoThe great policy challenge for governments in Canada in 2026

-

International18 hours ago

International18 hours agoLOCKED AND LOADED: Trump threatens U.S. response if Iran slaughters protesters