Business

Craziest examples of government waste – Taxpayer Waste Watch

News release from the Canadian Taxpayers Federation

The feds are spending millions of your tax dollars trying to “green” their offices. Then the government is spending millions more of your tax dollars flying battalions of bureaucrats and politicians around the world.

Here’s a crazy idea: the government could save you money, and cut down on emissions, by skipping out on a couple taxpayer-funded international conferences.

Plus, we’ve compiled the craziest examples of government waste in one video. You’re going to love the video, but hate the waste.

All that and more in this week’s Taxpayer Waste Watch. Enjoy.

Franco.

Bank of Canada fixes with its left hand, what it breaks with its right

They say hypocrites are the kind of people who will cut down a tree, only to stand on the stump and give a speech about the importance of protecting forests.

Someone should get the fat cats at the Bank of Canada on the horn and let them know about that particular definition.

In recent years, the Bank of Canada dumped millions of your tax dollars into a green initiative aimed at lowering its carbon footprint.

Meanwhile, at the exact same time, its executives have been racking up frequent flyer miles while globetrotting to exotic, far-flung locales.

Burning through jet fuel and your tax dollars in the process.

Since 2020, the Bank of Canada dropped $4.1 million on its “greening the bank” initiative, a multi-year effort to measure and reduce its carbon footprint.

More than $1 million has been spent on internal program costs, alongside $950,000 on external consultants and studies, and $2.1 million on green investments.

On top of the greening the bank initiative, the Bank of Canada also signed a contract with the Delphi Group for up to $300,000.

The Delphi Group is a consulting firm “specializing in climate change, sustainability and ESG,” according to its website.

Six staff from the Delphi Group will aid the Bank of Canada’s “annual quantification of its GHG inventory,” according to records obtained by the CTF.

But if the Bank of Canada is looking for ways to lower its carbon footprint, it doesn’t need to spend millions hiring consultants.

All it has to do is look at its executives’ expense reports.

In 2023, Bank of Canada executives racked up $535,000 in travel expenses.

Bank executives took dozens of trips to exotic destinations, including Portugal, Japan, Greece, France, Sweden, Germany, India, Peru, the West Indies and Switzerland.

Bank Governor Tiff Macklem racked up $179,000 in travel expenses alone.

Macklem took 26 separate trips, including four visits to Switzerland, two to Sweden, two to India and one each to Morocco, Portugal, Japan and the Caymen Islands.

So first you’re forced to pay for first-class airfare so bank executives can jet set around the globe to attend conferences and give speeches.

And then you’re forced to pay for millions in consultant fees because the big brains at the central bank are confused why their carbon footprint is so high.

Needless to say, if they can’t crack that puzzle, then it’s little wonder why inflation has run rampant while ravaging the paycheques of taxpayers like you.

But don’t worry, folks.

If the bank runs out of your cash to blow on all these vacations – erm, sorry, we mean “work trips” – we’re sure they’ll just fire up the money printer to cover the costs.

Franco’s note: Any time we write about the Bank of Canada I need to mention this:

The Bank of Canada has one job: keep inflation low and around two per cent. Bank of Canada bureaucrats got $20 million in bonuses in 2022 while it hiked interest rates seven times and inflation reached a 40-year high.

This should go without saying, but bonuses are for people who do a good job, not people who fail at their one and only job.

Trudeau wants to spend your money on…

Every year, the federal government tables main and supplementary estimate documents that detail how your money will be allocated to fund government programs.

But with all the shenanigans currently holding up the House of Commons, the Trudeau government is worried they may not be able to fund these government schemes.

It’s a good bet Prime Minister Justin Trudeau and his minions will claim a vote is needed to make sure struggling Canadians get the help they need.

But the CTF read through the entirety of the recently-released Supplementary Estimates report to see what sort of spending the feds are actually proposing:

- $970 million to cover pay raises for bureaucrats

- $4.5 million for government advertising

- $46 million for the 2026 FIFA Men’s World Cup

- $20 million for Diversity, Equity and Inclusion at the Canada Media Fund

- $200,000 for Prime Minister Justin Trudeau’s plan to plant two billion trees

- $45 million for the gun confiscation scheme

- $6.9 million for pro-carbon tax ads

- $5.5 million for the Toronto Film Festival

- $3.4 million for settlements related to the Phoenix payroll fiasco

Does any of that sound like necessary government spending to you?

VIDEO: Craziest government waste

We’ve said it time and time again.

You pay too much tax because the government wastes too much money.

Don’t believe us? Then watch (and share) the video below.

CTF Federal Director Franco Terrazzano brings the receipts on some of the craziest government waste that’s out of Ottawa in recent years.

If you’re looking for more reading on taxpayer issues, we’ve got you covered.

Canada’s EV gamble looks even more foolish with Trump retaking the White House: https://torontosun.com/

Government employees scored $150M in standby pay last year: https://torontosun.com/

Saskatoon spent more than $300,000 to name new bus system: https://www.taxpayer.

Confirms $523K Rush Orders: https://www.

Trudeau’s bureaucracy boom: Salaries and spending spiralling out of control: https://www.

Premier Holt’s carbon tax flip-flop: https://tj.news/

Alberta

Pierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

From Pierre Poilievre

The Port of Prince Rupert on the north coast of British Columbia. Photo courtesy Prince Rupert Port Authority

From the Canadian Energy Centre

By Will Gibson

Moratorium does little to improve marine safety while sending the wrong message to energy investors

In 2019, Martha Hall Findlay, then-CEO of the Canada West Foundation, penned a strongly worded op-ed in the Globe and Mail calling the federal ban of oil tankers on B.C.’s northern coast “un-Canadian.”

Six years later, her opinion hasn’t changed.

“It was bad legislation and the government should get rid of it,” said Hall Findlay, now director of the University of Calgary’s School of Public Policy.

The moratorium, known as Bill C-48, banned vessels carrying more than 12,500 tonnes of oil from accessing northern B.C. ports.

Targeting products from one sector in one area does little to achieve the goal of overall improved marine transport safety, she said.

“There are risks associated with any kind of transportation with any goods, and not all of them are with oil tankers. All that singling out one part of one coast did was prevent more oil and gas from being produced that could be shipped off that coast,” she said.

Hall Findlay is a former Liberal MP who served as Suncor Energy’s chief sustainability officer before taking on her role at the University of Calgary.

She sees an opportunity to remove the tanker moratorium in light of changing attitudes about resource development across Canada and a new federal government that has publicly committed to delivering nation-building energy projects.

“There’s a greater recognition in large portions of the public across the country, not just Alberta and Saskatchewan, that Canada is too dependent on the United States as the only customer for our energy products,” she said.

“There are better alternatives to C-48, such as setting aside what are called Particularly Sensitive Sea Areas, which have been established in areas such as the Great Barrier Reef and the Galapagos Islands.”

The Business Council of British Columbia, which represents more than 200 companies, post-secondary institutions and industry associations, echoes Hall Findlay’s call for the tanker ban to be repealed.

“Comparable shipments face no such restrictions on the East Coast,” said Denise Mullen, the council’s director of environment, sustainability and Indigenous relations.

“This unfair treatment reinforces Canada’s over-reliance on the U.S. market, where Canadian oil is sold at a discount, by restricting access to Asia-Pacific markets.

“This results in billions in lost government revenues and reduced private investment at a time when our economy can least afford it.”

The ban on tanker traffic specifically in northern B.C. doesn’t make sense given Canada already has strong marine safety regulations in place, Mullen said.

Notably, completion of the Trans Mountain Pipeline expansion in 2024 also doubled marine spill response capacity on Canada’s West Coast. A $170 million investment added new equipment, personnel and response bases in the Salish Sea.

“The [C-48] moratorium adds little real protection while sending a damaging message to global investors,” she said.

“This undermines the confidence needed for long-term investment in critical trade-enabling infrastructure.”

Indigenous Resource Network executive director John Desjarlais senses there’s an openness to revisiting the issue for Indigenous communities.

“Sentiment has changed and evolved in the past six years,” he said.

“There are still concerns and trust that needs to be built. But there’s also a recognition that in addition to environmental impacts, [there are] consequences of not doing it in terms of an economic impact as well as the cascading socio-economic impacts.”

The ban effectively killed the proposed $16-billion Eagle Spirit project, an Indigenous-led pipeline that would have shipped oil from northern Alberta to a tidewater export terminal at Prince Rupert, B.C.

“When you have Indigenous participants who want to advance these projects, the moratorium needs to be revisited,” Desjarlais said.

He notes that in the six years since the tanker ban went into effect, there are growing partnerships between B.C. First Nations and the energy industry, including the Haisla Nation’s Cedar LNG project and the Nisga’a Nation’s Ksi Lisims LNG project.

This has deepened the trust that projects can mitigate risks while providing economic reconciliation and benefits to communities, Dejarlais said.

“Industry has come leaps and bounds in terms of working with First Nations,” he said.

“They are treating the rights of the communities they work with appropriately in terms of project risk and returns.”

Hall Findlay is cautiously optimistic that the tanker ban will be replaced by more appropriate legislation.

“I’m hoping that we see the revival of a federal government that brings pragmatism to governing the country,” she said.

“Repealing C-48 would be a sign of that happening.”

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

Federal fiscal anchor gives appearance of prudence, fails to back it up

The Passage of Bill C-5 Leaves the Conventional Energy Sector With as Many Questions as Answers

-

Business2 days ago

Business2 days agoOttawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

COVID-192 days ago

COVID-192 days agoNew Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Business1 day ago

Business1 day agoWorld Economic Forum Aims to Repair Relations with Schwab

-

Alberta2 days ago

Alberta2 days agoThe permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

-

Alberta2 days ago

Alberta2 days agoAlberta’s government is investing $5 million to help launch the world’s first direct air capture centre at Innisfail

-

Business2 days ago

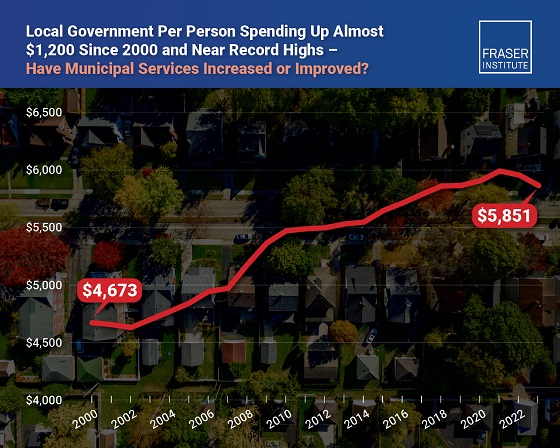

Business2 days agoMunicipal government per-person spending in Canada hit near record levels

-

Business2 days ago

Business2 days agoA new federal bureaucracy will not deliver the affordable housing Canadians need