Economy

Canada’s Energy Wealth Is Bleeding South

From the Frontier Centre for Public Policy

Without infrastructure, Canada is losing billions while the U.S. cashes in on our oil and gas

Canada’s energy wealth is stuck in traffic, and our American neighbours are cashing in. It’s worse than that. Canada is bleeding millions of dollars daily because it lacks the infrastructure to export its natural resources efficiently.

While our oil and gas continue to flow—mainly to the United States—provinces like Alberta and British Columbia are forced to sell at steep discounts. This isn’t just an economic inefficiency; it’s a structural failure of national policy. The beneficiaries? American businesses and their governments which pocket the profits and tax revenues that should be circulating through the Canadian economy. This is no way to achieve economic sovereignty for Canada.

With U.S. interests reaping the rewards, this should have been a central talking point when Prime Minister Carney met with President Trump earlier this month.

Ottawa often offers the recent completion of the Trans Mountain Expansion (TMX) pipeline as an example of federal support for the energy sector. But such claims are misleading. Kinder Morgan, a private enterprise, had initially planned to build the extension without a penny from taxpayers. It withdrew only after being crippled by federal regulatory delays and political uncertainty.

Ottawa stepped in not as a benevolent saviour to help Albertans, but to prevent lawsuits and save face—ultimately overpaying for the pipeline and watching construction costs balloon to nearly six times the original estimate.

To now declare this bungled project a “gift” to Alberta, as a recent op-ed in the Toronto Star did, is not only tone-deaf: it’s an insult. It ignores the fact that Alberta’s taxpayers helped finance the very project Ottawa botched. It also reveals an astonishing lack of understanding of the historical, economic and political dynamics at play between Ottawa and Western Canada.

The tragedy is that TMX, despite its importance, is insufficient. Our infrastructure bottlenecks remain. With each passing day, Canada forfeits wealth that could fund essential improvements in health care, education and national defence.

According to the Frontier Centre for Public Policy, which has developed a real-time tracker to monitor these losses, the price differential between what we could earn on global markets versus what we settle for domestically adds up to $26.5 billion annually.

Ottawa’s reluctance to greenlight new infrastructure is a primary cause of this problem. Ironically, the losses from this reluctance in a single year would be enough to pay for another TMX, mismanaged or not. The solution lies in a national commitment to building utility corridors: designated routes that facilitate the movement of energy, goods and services unhindered across provincial boundaries.

Carney’s recent promise to remove all interprovincial trade barriers by July 1 is a nice soundbite. But unless it includes meaningful infrastructure commitments, it is bound to fail like every other rhetorical flourish before it.

Canadians should be rightly skeptical. After all, what Ottawa has failed to achieve in the 157 years since Confederation is unlikely to be accomplished in the next 60 days.

The political math doesn’t help either. The Bloc Québécois holds the balance of power in the 45th Parliament, and its obstructionist stance on national pipeline development ensures the advent of more gridlock, not less. The federal government continues to uphold Bill C-69—dubbed the “no-pipelines bill”—further entrenching the status quo.

Meanwhile, Canada remains in the absurd position of relying on U.S. infrastructure to transport oil from the West to Ontario and Quebec. This undermines our economic independence, energy security and national sovereignty. No amount of “elbows up” will correct this enormous gap.

If the prime minister is serious about transforming Canada’s economic landscape and making the country strong, he must bypass the Bloc by cooperating with the Official Opposition. A grand bargain focused on utility corridors, interprovincial infrastructure and national trade efficiency would serve Alberta, Saskatchewan, and every Canadian who depends on a strong and self-reliant economy.

The stakes are high. We need a more productive country to face challenges within Canada and from abroad. Billions in lost revenue could fund new hospitals, more schools and better military readiness.

Instead, along with the limited exports of oil and gas, we’re exporting great opportunities to middlemen—and greater economic strength—south of the border.

The path forward is clear. A strong, self-reliant Canada needs infrastructure. It needs corridors. It needs leadership.

Marco Navarro-Genie is the vice president of research at the Frontier Centre for Public Policy. He is coauthor, with Barry Cooper, of Canada’s COVID: The Story of a Pandemic Moral Panic (2023).

Alberta

Pierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

From Pierre Poilievre

The Port of Prince Rupert on the north coast of British Columbia. Photo courtesy Prince Rupert Port Authority

From the Canadian Energy Centre

By Will Gibson

Moratorium does little to improve marine safety while sending the wrong message to energy investors

In 2019, Martha Hall Findlay, then-CEO of the Canada West Foundation, penned a strongly worded op-ed in the Globe and Mail calling the federal ban of oil tankers on B.C.’s northern coast “un-Canadian.”

Six years later, her opinion hasn’t changed.

“It was bad legislation and the government should get rid of it,” said Hall Findlay, now director of the University of Calgary’s School of Public Policy.

The moratorium, known as Bill C-48, banned vessels carrying more than 12,500 tonnes of oil from accessing northern B.C. ports.

Targeting products from one sector in one area does little to achieve the goal of overall improved marine transport safety, she said.

“There are risks associated with any kind of transportation with any goods, and not all of them are with oil tankers. All that singling out one part of one coast did was prevent more oil and gas from being produced that could be shipped off that coast,” she said.

Hall Findlay is a former Liberal MP who served as Suncor Energy’s chief sustainability officer before taking on her role at the University of Calgary.

She sees an opportunity to remove the tanker moratorium in light of changing attitudes about resource development across Canada and a new federal government that has publicly committed to delivering nation-building energy projects.

“There’s a greater recognition in large portions of the public across the country, not just Alberta and Saskatchewan, that Canada is too dependent on the United States as the only customer for our energy products,” she said.

“There are better alternatives to C-48, such as setting aside what are called Particularly Sensitive Sea Areas, which have been established in areas such as the Great Barrier Reef and the Galapagos Islands.”

The Business Council of British Columbia, which represents more than 200 companies, post-secondary institutions and industry associations, echoes Hall Findlay’s call for the tanker ban to be repealed.

“Comparable shipments face no such restrictions on the East Coast,” said Denise Mullen, the council’s director of environment, sustainability and Indigenous relations.

“This unfair treatment reinforces Canada’s over-reliance on the U.S. market, where Canadian oil is sold at a discount, by restricting access to Asia-Pacific markets.

“This results in billions in lost government revenues and reduced private investment at a time when our economy can least afford it.”

The ban on tanker traffic specifically in northern B.C. doesn’t make sense given Canada already has strong marine safety regulations in place, Mullen said.

Notably, completion of the Trans Mountain Pipeline expansion in 2024 also doubled marine spill response capacity on Canada’s West Coast. A $170 million investment added new equipment, personnel and response bases in the Salish Sea.

“The [C-48] moratorium adds little real protection while sending a damaging message to global investors,” she said.

“This undermines the confidence needed for long-term investment in critical trade-enabling infrastructure.”

Indigenous Resource Network executive director John Desjarlais senses there’s an openness to revisiting the issue for Indigenous communities.

“Sentiment has changed and evolved in the past six years,” he said.

“There are still concerns and trust that needs to be built. But there’s also a recognition that in addition to environmental impacts, [there are] consequences of not doing it in terms of an economic impact as well as the cascading socio-economic impacts.”

The ban effectively killed the proposed $16-billion Eagle Spirit project, an Indigenous-led pipeline that would have shipped oil from northern Alberta to a tidewater export terminal at Prince Rupert, B.C.

“When you have Indigenous participants who want to advance these projects, the moratorium needs to be revisited,” Desjarlais said.

He notes that in the six years since the tanker ban went into effect, there are growing partnerships between B.C. First Nations and the energy industry, including the Haisla Nation’s Cedar LNG project and the Nisga’a Nation’s Ksi Lisims LNG project.

This has deepened the trust that projects can mitigate risks while providing economic reconciliation and benefits to communities, Dejarlais said.

“Industry has come leaps and bounds in terms of working with First Nations,” he said.

“They are treating the rights of the communities they work with appropriately in terms of project risk and returns.”

Hall Findlay is cautiously optimistic that the tanker ban will be replaced by more appropriate legislation.

“I’m hoping that we see the revival of a federal government that brings pragmatism to governing the country,” she said.

“Repealing C-48 would be a sign of that happening.”

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

Federal fiscal anchor gives appearance of prudence, fails to back it up

The Passage of Bill C-5 Leaves the Conventional Energy Sector With as Many Questions as Answers

-

Business2 days ago

Business2 days agoOttawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

COVID-192 days ago

COVID-192 days agoNew Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Business1 day ago

Business1 day agoWorld Economic Forum Aims to Repair Relations with Schwab

-

Alberta2 days ago

Alberta2 days agoThe permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

-

Alberta2 days ago

Alberta2 days agoAlberta’s government is investing $5 million to help launch the world’s first direct air capture centre at Innisfail

-

Business2 days ago

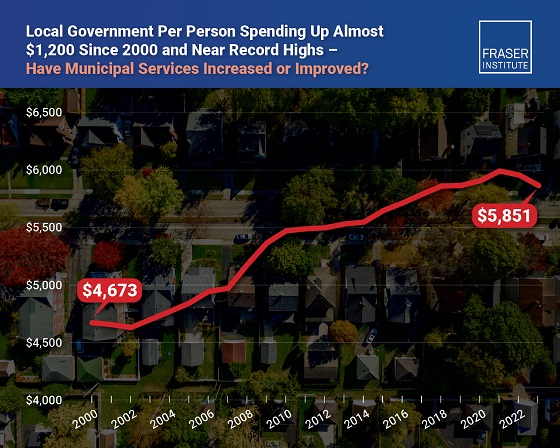

Business2 days agoMunicipal government per-person spending in Canada hit near record levels

-

Business1 day ago

Business1 day agoA new federal bureaucracy will not deliver the affordable housing Canadians need