Banks

What 100 million “unbanked” Nigerians can teach Canadians about Central Bank Digital Currency

From the Frontier Centre for Public Policy

By Gieb Lisikh

Despite credit cards, e-transfers and online banking having already made money go pretty much digital, the Bank of Canada is busily working on a much bigger transformation. Canada is one of about 100 countries that – in uncanny synchronicity – several years ago joined the race toward retail central bank digital currency (CBDC).

Touted as the digital equivalent of cash, CBDC risks eroding the established banking system and, among many other problems, is likely to be vulnerable to hackers’ attacks which, should a foreign government use this as a tactic in “hybrid” warfare, might prove capable of destabilizing a target country’s economy.

Considering such acute risks, it would be reasonable to expect that the explosion of worldwide interest in CBDC is justified by its special qualities that address obvious pressing needs of the citizenry. The purported consumer and other needs for CBDC, however, seem to be entirely fabricated, while the qualities that actually differentiate CBDC from the money we use now are hushed and obscured by virtue-signalling.

CBDC’s main advertised feature is equivalency to cash. It is everywhere marketed as a means to advance “financial inclusion” – a convenient way for the “unbanked” to access financial services – both a stand-in and replacement for cash, which it is claimed is about to disappear from use.

The Bank of Canada admits, however, that CBDC cannot actually replace cash or make an “unbanked” person “banked”. That’s because CBDC does nothing to address the two key reasons people still use cash: the need for privacy and independence from technology. CBDC does the opposite. First, CBDC has a built-in lack of privacy as it’s designed to always leave a digital trail. Second, it requires the use of an internet-connected device – meaning it is not only technology-dependent but interruptible.

While some research suggests only 2 percent of Canadians still rely heavily on cash, a Bank of Canada survey found that 46 percent of us would find the elimination of cash anywhere from inconvenient to disastrous. What might happen if governments forcibly removed cash from circulation? We don’t need to guess, for we have a large-scale case-study available.

In Nigeria, about half of adults had no bank account when in October 2021 the government introduced eNaira, the world’s first serious CBDC implementation. Making 100 million “unbanked” Nigerians happy was no doubt intended not only as a national but as a global endorsement for CBDC. Yet it did the opposite, eventually rocking the country to its core.

A piddly 0.8 percent of already “banked” Nigerians downloaded eNaira wallets in the first year after the launch, of whom most did not engage in any transactions. Not dissuaded by such overwhelming indifference, the government doubled-down with an all-out attack on cash, demonetizing banknotes and forcing Nigerians to exchange their cash holdings for eNaira. The nation’s 100 million poorest people were left with paper money they could not use to buy food or other necessities. This triggered violent riots as desperate hungry people took to the streets, demanding reinstatement of cash. The situation persisted for more than three months until cash was re-enabled. Today Nigeria’s government is trying to boost eNaira use through artificial cash shortages.

The International Monetary Fund’s (IMF) consultants heavily pushed the “financial inclusion” narrative in Nigeria, fully endorsing it as “a key policy objective that central banks, especially those in emerging and low-income countries, are considering for retail [CBDC].” Yet bizarrely, the same IMF document notes: “The impact of CBDC for improving financial inclusion is currently speculative, where further evidence and experience are needed to fully understand benefits and limitations.”

How can the main reason for a large financial overhaul that will be life-altering for hundreds of millions of people and carries many risks be…speculative? As if dodging this question, the Bank of Canada turns the conversation on its head: instead of looking for a justifiable use case that warrants “wide adoption, acceptance and use of CBDC”, it goes into talk of “overcoming the barriers”. The Bank seems to have made its commitment to building CBDC capacity before finding a genuine need. And that leaves us with the only sensible conclusion: that the advertised justifications are just an awkward façade, hiding the real and not-so-welcome reasons.

The two major features making CBDC different from traditional money are that CBDC is centrally traceable and programmable. This makes CBDC almost infinitely dangerous. It will be only one step from monitoring your every financial move to telling you how and when to spend your money. CBDC will enable “special purposes” like spending caps or blocks, transfer limits, consumption controls, penalty taxes, forced loans, nudge economics, geo fencing and more. These things are already happening in China and, according to Russian officials, may soon begin there as well.

Those utterly undemocratic purposes should outrage any Westerner, but they fit China’s social credit system like a glove. They could be further enhanced by other privacy-intrusive measures like digital ID, surveillance and elimination of cash or alternative monetary systems such as cryptocurrency.

Canadians have expressed no desire, understanding or even, for the most part, awareness of the publicly-funded CBDC development and the reasons behind it. As in Nigeria, the nation’s central bank does not listen but simply insists on and proceeds with this affair, claiming it’s to benefit Canadians but failing or not even trying to articulate how.

The original, full-length version of this article was recently published in C2C Journal.

Gleb Lisikh is a researcher and IT management professional, and a father of three children. He lives in Vaughan, Ontario and grew up in various parts of the Soviet Union.

Racket News

Racket News

By Eric Salzman

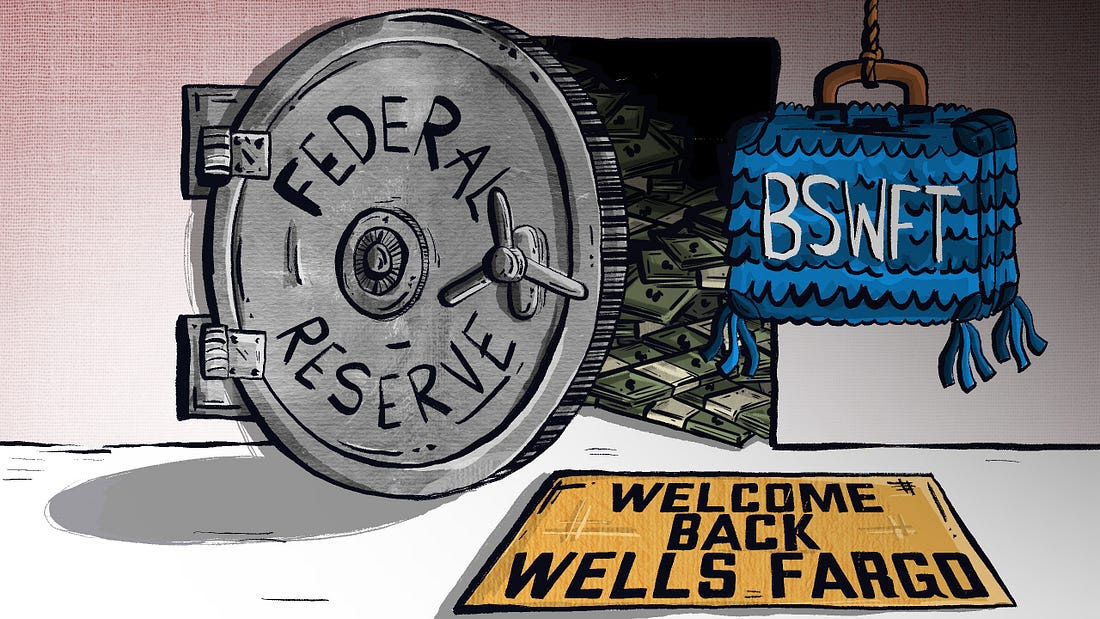

The heavyweight champion of financial crime gets seemingly its millionth chance to show it’s reformed

The past two decades have been tough ones for Wells Fargo and the many victims of its sprawling crime wave. While the banking industry is full of scammers, Wells took turning time honored street-hustles into multi-billion dollar white-collar hustles to a new level.

The Federal Reserve announced last month that Wells Fargo is no longer subject to the asset growth restriction the Fed finally enforced in 2018 after multiple scandals. This was a major enforcement action that prohibited Wells from growing existing loan portfolios, purchasing other bank branches or entering into any new activities that would result in their asset base growing.

Upon hearing the news that Wells was being released from the Fed’s penalty box, my mind turned to this pivotal moment in the classic movie “Slapshot.”

Here are some of Wells Fargo’s lowlights both before and after the Fed’s enforcement action:

- December 2022: Wells Fargo paid more than $2 billion to consumers and $1.7 billion in civil penalties after the Consumer Financial Protection Bureau (CFPB) found mismanagement — including illegal fees and interest charges — in several of its biggest product lines, such as auto loans, mortgages, and deposit accounts.

- September 2021: Wells Fargo paid $72.6 million to the Justice Department for overcharging foreign exchange customers from 2010-2017.

- February 2020: Wells Fargo paid $3 billion to settle criminal and civil investigations by the Justice Department and SEC into its aggressive sales practices between 2002 and 2016. About $500 million was eventually distributed to investors.

- January 2020: The Office of the Comptroller of the Currency (OCC) banned two senior executives, former CEO John Stumpf and ex-Head of Community Bank Carrie Tolstedt, from the banking industry. Stumpf and Tolstedt also incurred civil penalties of $17.5 million and $17 million.

- August 2018: The Justice Department levied a $2.09 billion fine on Wells Fargo for its actions during the subprime mortgage crisis, particularly its mortgage lending practices between 2005 and 2007.

- April 2018: Federal regulators at the CFPB and OCC examined Wells’ auto loan insurance and mortgage lending practices and ordered the bank to pay $1 billion in damages.

- February 2018: The aforementioned Fed enforcement action. In addition to the asset growth restriction, Wells was ordered to replace three directors.

- October 2017: Wells Fargo admitted wrongdoing after 110,000 clients were fined for missing a mortgage payment deadline — delays for which the bank was ultimately deemed at fault.

- July 2017: As many as 570,000 Wells Fargo customers were wrongly charged for auto insurance on car loans after the bank failed to verify whether those customers already had existing insurance. As a result, up to 20,000 customers may have defaulted on car loans.

- September 2016: Wells Fargo acknowledged its employees had created 1.5 million deposit accounts and 565,000 credit card accounts between 2002 and 2016 that “may not have been authorized by consumers,” according to CFPB. As a result, the lender was forced to pay $185 million in damages to the CFPB, OCC, and City and County of Los Angeles.

Additionally, somehow in 2023 Wells even managed to drop $1 billion in a civil settlement with shareholders for overstating their progress in complying with their 2018 agreement with the Fed to clean themselves up!

I imagine if Wells were in any other business, it wouldn’t be allowed to continue. But Wells is part of the “Too Big to Fail” club. Taking away its federal banking charter would be too disruptive for the financial markets, so instead they got what ended up being a seven-year growth ban. Not exactly rough justice.

While not the biggest settlement, my favorite Wells scam was the 2021 settlement of the seven-year pilfering operation, ripping off corporate customers’ foreign exchange transactions.

Like many banks, Wells Fargo offers its corporate clients with global operations foreign exchange (FX) services. For example, if a company is based in the U.S. but has extensive dealings in Canada, it may receive payments in Canadian dollars (CAD) that need to be exchanged for U.S. dollars (USD) and vice versa. Wells, like many banks, has foreign exchange specialists who do these conversions. Ideally, the banks optimize their clients’ revenue and decrease risk, in return for a markup fee, or “spread.”

There’s a lot of trust involved with this activity as the corporate customers generally have little idea where FX is trading minute by minute, nor do they know what time of day the actual orders for FX transactions — commonly called “BSwifts” — come in. For an unscrupulous bank, it’s a license to steal, which is exactly what Wells did.

According to the complaint, Wells regularly marked up transactions at higher spreads than what was agreed upon. This was just one of the variety of naughty schemes Wells used to clobber their customers. My two favorites were “The Big Figure Trick” and the “BSwift Pinata.”

The Big Figure Trick

Let’s say a client needs to sell USD for CAD, and that the $1 USD is worth $1.32 CAD. In banking parlance, the 32 cents is called the “Big Figure.” Wells would buy the CAD at $1.32 for $1 USD and then transpose the actual exchange rate on the customer statement from $1.32 to $1.23. If the customer didn’t notice, Wells would pocket the difference. On a transaction where the client is buying 5 million CAD with USD, the ill-gotten gain for Wells would be about $277,000 USD!

Conversely, if the customer did notice the difference, Wells would just blame it on the grunts in its operational back office, saying they accidentally transposed the number and “correct” the transaction. From the complaint, here is some give and take between two Wells FX specialists:

“You can play the transposition error game if you get called out.” Another FX sales specialist noted to a colleague about a previous transaction that a customer “didn’t flinch at the big fig the other day. Want to take a bit more?”

The BSwift Piñata

The way this hustle would work is, let’s say the Wells corporate customer was receiving payment from one of their Canadian clients. The Canadian client’s bank would send a BSwift message to Wells. The Wells client was in the dark about the U.S. dollar-Canadian dollar exchange rate because it had no idea what time of day the message arrived. Wells took advantage of that by purchasing U.S. dollars for Canadian dollars first. For simplicity, think of the U.S. dollar-Canadian dollar exchange rate as a widget that Wells bought for $1. If the widget increased in value, say to $1.10 during the day, Wells would sell the widget they purchased for $1 to the client for $1.10 and pocket 10 cents. If the price of the widget Wells bought for $1 fell to 95 cents, Wells would just give up their $1 purchase to the client, plus whatever markup they agreed to.

Heads, Wells wins. Tails, client loses.

The complaint notes that a Wells FX specialist wrote that he:

“Bumped spreads up a pinch,” that “these clients who are in the mode of just processing wires will most likely not notice this slight change in pricing” and that it “could have a very quick positive impact on revenue without a lot of risk.”

Talk about a boiler room operation. Personally, I think calling what you are doing to a client a “piñata” should have easily put Wells in the Fed’s penalty box another 5 years at least!

Wells has been released from the Fed’s 2018 enforcement order. I would like to think they have learned their lesson and are reformed, but I would lay good odds against it. A leopard can’t change its spots.

Racket News is a reader-supported publication.

Consider becoming a free or paid subscriber.

From the Fraser Institute

By Matthew Lau

And in January, all of Canada’s six largest banks quit the Net-Zero Banking Alliance, an alliance formerly led by Mark Carney (before he resigned to run for leadership of the Liberal Party) that aimed to align banking activities with net-zero emissions by 2050.

The Canada Pension Plan Investment Board (CPPIB) has cancelled its commitment, established just three years ago, to transition to net-zero emissions by 2050. According to the CPPIB, “Forcing alignment with rigid milestones could lead to investment decisions that are misaligned with our investment strategy.”

This latest development is good news. The CPPIB, which invest the funds Canadians contribute to the Canada Pension Plan (CPP), has a fiduciary duty to Canadians who are forced to pay into the CPP and who rely on it for retirement income. The CPPIB’s objective should not be climate activism or other environmental or social concerns, but risk-adjusted financial returns. And as noted in a broad literature review by Steven Globerman, senior fellow at the Fraser Institute, there’s a lack of consistent evidence that pursuing ESG (environmental, social and governance) objectives helps improve financial returns.

Indeed, as economist John Cochrane pointed out, it’s logically impossible for ESG investing to achieve social or environmental goals while also improving financial returns. That’s because investors push for these goals by supplying firms aligned with these goals with cheaper capital. But cheaper capital for the firm is equivalent to lower returns for the investor. Therefore, “if you don’t lose money on ESG investing, ESG investing doesn’t work,” Cochrane explained. “Take your pick.”

The CPPIB is not alone among financial institutions abandoning environmental objectives in recent months. In April, Canada’s largest company by market capitalization, RBC, announced it will cancel its sustainable finance targets and reduce its environmental disclosures due to new federal rules around how companies make claims about their environmental performance.

And in January, all of Canada’s six largest banks quit the Net-Zero Banking Alliance, an alliance formerly led by Mark Carney (before he resigned to run for leadership of the Liberal Party) that aimed to align banking activities with net-zero emissions by 2050. Shortly before Canada’s six largest banks quit the initiative, the six largest U.S. banks did the same.

There’s a second potential benefit to the CPPIB cancelling its net-zero commitment. Now, perhaps with the net-zero objective out of the way, the CPPIB can rein in some of the administrative and management expenses associated with pursuing net-zero.

As Andrew Coyne noted in a recent commentary, the CPPIB has become bloated in the past two decades. Before 2006, the CPP invested passively, which meant it invested Canadians’ money in a way that tracked market indexes. But since switching to active investing, which includes picking stocks and other strategies, the CPPIB ballooned from 150 employees and total costs of $118 million to more than 2,100 employees and total expenses (before taxes and financing) of more than $6 billion.

This administrative ballooning took place well before the rise of environmentally-themed investing or the CPPIB’s announcement of net-zero targets, but the net-zero targets didn’t help. And as Coyne noted, the CPPIB’s active investment strategy in general has not improved financial returns either.

On the contrary, since switching to active investing the CPPIB has underperformed the index to a cumulative tune of about $70 billion, or nearly one-tenth of its current fund size. “The fund’s managers,” Coyne concluded, “have spent nearly two decades and a total of $53-billion trying to beat the market, only to produce a fund that is nearly 10-per-cent smaller than it would be had they just heaved darts at the listings.”

Scrapping net-zero commitments won’t turn that awful track record around overnight. But it’s finally a step in the right direction.

Before Trudeau average annual immigration was 617,800. Under Trudeau number skyrocketted to 1.4 million annually

FDA requires new warning on mRNA COVID shots due to heart damage in young men

“This is a total fucking disaster”

News Jeffrey Epstein did not have a client list, nor did he kill himself, Trump DOJ, FBI claim

-

Also Interesting2 days ago

Also Interesting2 days ago9 Things You Should Know About PK/PD in Drug Research

-

Business2 days ago

Business2 days agoCannabis Legalization Is Starting to Look Like a Really Dumb Idea

-

Bruce Dowbiggin2 days ago

Bruce Dowbiggin2 days agoThe Covid 19 Disaster: When Do We Get The Apologies?

-

Media2 days ago

Media2 days agoCBC journalist quits, accuses outlet of anti-Conservative bias and censorship

-

Business2 days ago

Business2 days agoCarney government should recognize that private sector drives Canada’s economy

-

Alberta2 days ago

Alberta2 days agoFourteen regional advisory councils will shape health care planning and delivery in Alberta

-

Alberta1 day ago

Alberta1 day agoAlberta school boards required to meet new standards for school library materials with regard to sexual content

-

Business1 day ago

Business1 day agoUN’s ‘Plastics Treaty’ Sports A Junk Science Wrapper