Business

COVID response closed more Canadian businesses than 2008 financial crisis: gov’t report

From LifeSiteNews

StatsCan revealed that they are witnessing an increase in ‘zombie businesses,’ a phenomenon which occurs when owners never file for bankruptcy but simply walk away from their business.

Statistics Canada has revealed that more businesses closed as a result of the COVID-induced economic downturn than the 2008 financial crisis.

On October 25, Statistics Canada reported that the COVID-19 “pandemic” caused a record number of small businesses to shut down, with many owners never filing for bankruptcy but instead simply walking away from their companies, resulting in a large uptick in a phenomenon called “zombie businesses,” according to information obtained by Blacklock’s Reporter.

“This finding represents a larger increase than observed during the 2008 financial crisis when the exit rate increased by one percentage point,” wrote analysts.

The 2007- 2008 financial crisis, also called the Global Financial Crisis, is considered the most severe worldwide economic crisis since the Great Depression of 1929.

Business exits refer to the permanent closure of a business and can occur without a formal process, meaning owners can walk away from their businesses without declaring bankruptcy.

According to StatsCan, exits increased at the same time as bankruptcies fell, which is partly because courts were closed due to COVID lockdowns.

However, analysts noted that exits did not appear in bankruptcy court statistics, adding, “Formal insolvencies are not the whole story. Formal insolvency is but one path a business in distress may take.”

“The COVID-19 pandemic had a substantial impact on business dynamics leading to the temporary or permanent closure of many businesses,” analysts continued.

According to a Department of Industry estimate, Canada had 1,198,632 small businesses before COVID lockdowns. While the number has been revealed to have decreased drastically since then, federal agencies have failed to record comprehensive figures on the economic impact of COVID lockdowns and regulations.

“In my view there are hundreds of thousands of zombie businesses, businesses that are essentially dead but haven’t finalized the closure process altogether,” Dan Kelly, CEO of the Canadian Federation of Independent Business, testified at 2020 hearings of the Senate national finance committee. “We are seeing greater numbers of business failures that actually haven’t been reported. We’re only at the tip of the iceberg.”

According to a 2022 Bank of Canada survey, only an estimated half of businesses reopened after being closed by COVID lockdowns. The research tracked 12,976 businesses throughout Vancouver, Toronto and Ottawa including bars, restaurants, shops, nightclubs and motels, which were locked down by COVID regulations in April and May 2021.

“Half of businesses recorded as temporarily closed in May had reopened by the end of September,” the Bank reported. “Forty percent were still hibernating. Ten percent were closed for good.”

Statistics Canada’s report comes as Liberals MPs recently opted for a closed-door review by Minister of Health advisers of how the Canadian government handled the COVID-19 “pandemic” instead of launching a public inquiry.

In recent months, numerous reports have emerged revealing the Trudeau government’s mismanagement during the COVID-19 “pandemic.”

In a 2021 report Pandemic Preparedness, the Auditor General revealed that the cabinet was “not adequately prepared.”

Furthermore, Lessons Learned From The Public Health Agency Of Canada’s COVID-19 Response, an internal audit, condemned managers for “confusion,” “limited public health expertise” and “no clear understanding” of how to compile critical data.

Additionally, former Finance Minister Bill Morneau declared that spending programs to tackle COVID were prolonged and led to inflation under Prime Minister Justin Trudeau’s leadership.

During the so-called COVID-19 pandemic, the Trudeau government issued billions to Canadians who claimed they needed Canadian Emergency Response Benefits (CERB) as they were not permitted to work under COVID regulations.

Recently, the Canadian Revenue Agency (CRA) has worked to take back the $3.2 billion from Canadians who filed for and were given CERB despite not being eligible to receive it. However, many are fighting in court to keep their government payments.

From the Fraser Institute

Two recent events exemplify the fundamental irrationality that is Canada’s electric vehicle (EV) policy.

First, the Carney government re-committed to Justin Trudeau’s EV transition mandate that by 2035 all (that’s 100 per cent) of new car sales in Canada consist of “zero emission vehicles” including battery EVs, plug-in hybrid EVs and fuel-cell powered vehicles (which are virtually non-existent in today’s market). This policy has been a foolish idea since inception. The mass of car-buyers in Canada showed little desire to buy them in 2022, when the government announced the plan, and they still don’t want them.

Second, President Trump’s “Big Beautiful” budget bill has slashed taxpayer subsidies for buying new and used EVs, ended federal support for EV charging stations, and limited the ability of states to use fuel standards to force EVs onto the sales lot. Of course, Canada should not craft policy to simply match U.S. policy, but in light of policy changes south of the border Canadian policymakers would be wise to give their own EV policies a rethink.

And in this case, a rethink—that is, scrapping Ottawa’s mandate—would only benefit most Canadians. Indeed, most Canadians disapprove of the mandate; most do not want to buy EVs; most can’t afford to buy EVs (which are more expensive than traditional internal combustion vehicles and more expensive to insure and repair); and if they do manage to swing the cost of an EV, most will likely find it difficult to find public charging stations.

Also, consider this. Globally, the mining sector likely lacks the ability to keep up with the supply of metals needed to produce EVs and satisfy government mandates like we have in Canada, potentially further driving up production costs and ultimately sticker prices.

Finally, if you’re worried about losing the climate and environmental benefits of an EV transition, you should, well, not worry that much. The benefits of vehicle electrification for climate/environmental risk reduction have been oversold. In some circumstances EVs can help reduce GHG emissions—in others, they can make them worse. It depends on the fuel used to generate electricity used to charge them. And EVs have environmental negatives of their own—their fancy tires cause a lot of fine particulate pollution, one of the more harmful types of air pollution that can affect our health. And when they burst into flames (which they do with disturbing regularity) they spew toxic metals and plastics into the air with abandon.

So, to sum up in point form. Prime Minister Carney’s government has re-upped its commitment to the Trudeau-era 2035 EV mandate even while Canadians have shown for years that most don’t want to buy them. EVs don’t provide meaningful environmental benefits. They represent the worst of public policy (picking winning or losing technologies in mass markets). They are unjust (tax-robbing people who can’t afford them to subsidize those who can). And taxpayer-funded “investments” in EVs and EV-battery technology will likely be wasted in light of the diminishing U.S. market for Canadian EV tech.

If ever there was a policy so justifiably axed on its failed merits, it’s Ottawa’s EV mandate. Hopefully, the pragmatists we’ve heard much about since Carney’s election victory will acknowledge EV reality.

Kenneth P. Green

Senior Fellow, Fraser Institute

From the Fraser Institute

While running for the job of leading the country, Prime Minister Carney promised to defend the Canada Health Act (CHA) and build a health-care system Canadians can be proud of. Unfortunately, to have any hope of accomplishing the latter promise, he must break the former and reform the CHA.

As long as Ottawa upholds and maintains the CHA in its current form, Canadians will not have a timely, accessible and high-quality universal health-care system they can be proud of.

Consider for a moment the remarkably poor state of health care in Canada today. According to international comparisons of universal health-care systems, Canadians endure some of the lowest access to physicians, medical technologies and hospital beds in the developed world, and wait in queues for health care that routinely rank among the longest in the developed world. This is all happening despite Canadians paying for one of the developed world’s most expensive universal-access health-care systems.

None of this is new. Canada’s poor ranking in the availability of services—despite high spending—reaches back at least two decades. And wait times for health care have nearly tripled since the early 1990s. Back then, in 1993, Canadians could expect to wait 9.3 weeks for medical treatment after GP referral compared to 30 weeks in 2024.

But fortunately, we can find the solutions to our health-care woes in other countries such as Germany, Switzerland, the Netherlands and Australia, which all provide more timely access to quality universal care. Every one of these countries requires patient cost-sharing for physician and hospital services, and allows private competition in the delivery of universally accessible services with money following patients to hospitals and surgical clinics. And all these countries allow private purchases of health care, as this reduces the burden on the publicly-funded system and creates a valuable pressure valve for it.

And this brings us back to the CHA, which contains the federal government’s requirements for provincial policymaking. To receive their full federal cash transfers for health care from Ottawa (totalling nearly $55 billion in 2025/26) provinces must abide by CHA rules and regulations.

And therein lies the rub—the CHA expressly disallows requiring patients to share the cost of treatment while the CHA’s often vaguely defined terms and conditions have been used by federal governments to discourage a larger role for the private sector in the delivery of health-care services.

Clearly, it’s time for Ottawa’s approach to reflect a more contemporary understanding of how to structure a truly world-class universal health-care system.

Prime Minister Carney can begin by learning from the federal government’s own welfare reforms in the 1990s, which reduced federal transfers and allowed provinces more flexibility with policymaking. The resulting period of provincial policy innovation reduced welfare dependency and government spending on social assistance (i.e. savings for taxpayers). When Ottawa stepped back and allowed the provinces to vary policy to their unique circumstances, Canadians got improved outcomes for fewer dollars.

We need that same approach for health care today, and it begins with the federal government reforming the CHA to expressly allow provinces the ability to explore alternate policy approaches, while maintaining the foundational principles of universality.

Next, the Carney government should either hold cash transfers for health care constant (in nominal terms), reduce them or eliminate them entirely with a concordant reduction in federal taxes. By reducing (or eliminating) the pool of cash tied to the strings of the CHA, provinces would have greater freedom to pursue reform policies they consider to be in the best interests of their residents without federal intervention.

After more than four decades of effectively mandating failing health policy, it’s high time to remove ambiguity and minimize uncertainty—and the potential for politically motivated interpretations—in the CHA. If Prime Minister Carney wants Canadians to finally have a world-class health-care system then can be proud of, he should allow the provinces to choose their own set of universal health-care policies. The first step is to fix, rather than defend, the 40-year-old legislation holding the provinces back.

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

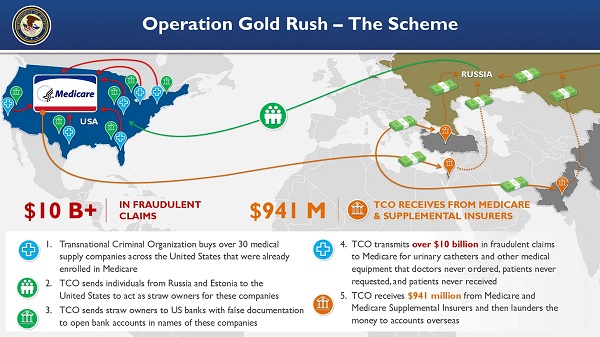

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Alberta2 days ago

Alberta2 days agoCOWBOY UP! Pierre Poilievre Promises to Fight for Oil and Gas, a Stronger Military and the Interests of Western Canada

-

Alberta2 days ago

Alberta2 days agoAlberta and Ontario sign agreements to drive oil and gas pipelines, energy corridors, and repeal investment blocking federal policies

-

Crime1 day ago

Crime1 day ago“This is a total fucking disaster”

-

International2 days ago

International2 days agoChicago suburb purchases childhood home of Pope Leo XIV

-

Fraser Institute1 day ago

Fraser Institute1 day agoBefore Trudeau average annual immigration was 617,800. Under Trudeau number skyrocketted to 1.4 million annually

-

Daily Caller2 days ago

Daily Caller2 days agoBlackouts Coming If America Continues With Biden-Era Green Frenzy, Trump Admin Warns

-

MAiD1 day ago

MAiD1 day agoCanada’s euthanasia regime is already killing the disabled. It’s about to get worse

-

Daily Caller2 days ago

Daily Caller2 days ago‘I Know How These People Operate’: Fmr CIA Officer Calls BS On FBI’s New Epstein Intel