Opinion

OPINION: Some Councillors made passionate pleas for raises. Did they make their case? You tell me.

The opinions expressed in this article are solely those of the writer and should not be interpreted as reflecting the editorial policy of Todayville, Inc.

The city of Red Deer just went through a sad episode in municipal politics. March 2017 the federal government announced the end of a subsidy for politicians, for January 1 2019. Til now politicians did not have to pay taxes on 1/3 of their earnings. Which could add up over time.

Rather than discuss it in advance, determine a proper way to deal with the end of a subsidy or determine a proper compensation package for the mayor and city councillors, they waited til the 11th hour, after they have been elected or re-elected, as in the majority of cases.

One councillor talked about working 10 hours a day everyday of the year, so he deserves a raise to $68,618.16 /yr. giving him an earning of $18.80 /hr for his 10 hours a day everyday. Kind of unbelievable that our councillors work 10 hours a day, everyday, with no days off, no holidays, etc.

Another councillor, said we should be grateful to have such great people on council, so grateful that we should give them raises to cover the end of their tax subsidy. Why this council brought us such events as the CFR and the Winter Games but he failed to mention other issues that became famous under his watch.

Red Deer never recovered from the last recession and is experiencing a continued downturn, while neighbouring communities continue to grow following the provincial growth rate of 4% annually.

Remember these stories:

Alberta on track to have worst air quality in Canada

Red Deer has worst pollution in province, while 4 other regions close to exceeding national standards

Alberta Environment Minister Shannon Phillips says the province is on track to have the worst air quality in Canada, and vows the government will put measures in place to reduce emissions from industry and vehicles.

“The time to act is long overdue,” Phillips said.

“We have a responsibility to do everything we can to protect the health of Albertans.”

Phillips made the remarks after seeing the results of the Canadian Ambient Air Quality Standards report, which show the Red Deer region has exceeded national standards. Four other regions — Lower Athabasca, Upper Athabasca, North Saskatchewan and South Saskatchewan — are close to exceeding national standards.

Phillips said there is no immediate health risk for people living in central Alberta.

“These results are concerning,” Phillips said in a news release. “We can’t keep going down the same path and expecting a different result. Our government has a responsibility to protect the health of Albertans by ensuring air pollution from all sources is addressed.”

The province will initiate an “action plan” to deal with poor air quality in the Red Deer area, a move she said is required under the Canadian Ambient Air Quality Standards.

Red Deer has one of the highest crime rate in the country

According to the local newspaper, The Red Deer Advocate, our fine city has some serious crime issues, compared to other major cities in Alberta. Following are sections of the story:

“Red Deer’s Crime Severity Index (CSI) is higher than Alberta’s other four major cities, recently released Statistics Canada information reveals.”

“The Crime Severity Index measures the volume and severity of crimes reported to police and is standardized, using the number 100 as the base, for the year 2006. It is calculated using all Criminal Code violations including offences like stolen vehicles, traffic and drug violations, and federal statutes”

“According to Statistics Canada, the overall CSI for 2015 for Red Deer is 182 (numbers have been rounded off).”

“This compares with Edmonton at 112, Lethbridge at 109, and Calgary and Medicine Hat both at 77. Alberta’s CSI is 102 and Canada overall is 70.”

“When looking specifically at violent crime, Statistics Canada shows that index for Red Deer up by almost 24 per cent (146 in 2015 from 118 in 2014). It had actually declined each year from 2012 to 2014, before increasing. There were no homicides in 2014. There were two in 2015.”

Red Deer’s population peaked in 2015 and declined in 2016

City council will be talking about growth and managing it. Let us look at the growth during the last mandate 2013-2017. The last census was done in 2016 and showed a decrease since 2015. (99,832 from 100,807) The decision was made to cancel the 2017 census since there was no sign of growth and you needed growth to justify the cost of the census.

Population of Red Deer in 2016 was 99,832 a increase of 2,723 or 2.8%over 97,109 in 2013. Not that great on the face of things, but looking deeper and you realize some neighbourhoods did not even fare that well.

For example;

Kentwood 2016=4,267 2013=4,280

Glendale 2016=4,288 2013=4,393

Normandeau 2016=3,530 2013=3,565

Pines 2016=1,718 2013=1,823

Highland Green 2016=3,920 2013=3,979

Oriole Park 2016=5,244 2013=5,308

Riverside Meadows 2016=3,686 2013=3,665

Fairview 2016=710 2013=770

Johnstone Park 2016=3,865 2013=3760

Total 2016=31,228 2013=31,543

Percentage of population 2016=31.3% 2013= 32.5%

Red Deer City Population 2016=99,832 2013=97,109

In case you did not know these are the neighbourhoods north of the river. So while the city grew for 3 of 4 years in the end it still grew over 4 years ago. The city shrank in total from 100,807 in 2015 to 99,832 in 2016. These neighbourhoods, except for Johnstone Park which grew by 105 and Riverside Meadows which grew by 21, shrank in size over the four years.

So I ask the incumbents to offer measures to stem the outward migration and encourage growth. Anyone? Perhaps build a north side Collicutt Centre? A high school?

The facts are there on reddeer.ca for anyone to study.

Did they make their case. Are they the saviours of Red Deer or not?

?

Alberta

‘Far too serious for such uninformed, careless journalism’: Complaint filed against Globe and Mail article challenging Alberta’s gender surgery law

![]()

Macdonald Laurier Institute challenges Globe article on gender medicine

The complaint, now endorsed by 41 physicians, was filed in response to an article about Alberta’s law restricting gender surgery and hormones for minors.

On June 9, the Macdonald-Laurier Institute submitted a formal complaint to The Globe and Mail regarding its May 29 Morning Update by Danielle Groen, which reported on the Canadian Medical Association’s legal challenge to Alberta’s Bill 26.

Written by MLI Senior Fellow Mia Hughes and signed by 34 Canadian medical professionals at the time of submission to the Globe, the complaint stated that the Morning Update was misleading, ideologically slanted, and in violation the Globe’s own editorial standards of accuracy, fairness, and balance. It objected to the article’s repetition of discredited claims—that puberty blockers are reversible, that they “buy time to think,” and that denying access could lead to suicide—all assertions that have been thoroughly debunked in recent years.

Given the article’s reliance on the World Professional Association for Transgender Health (WPATH), the complaint detailed the collapse of WPATH’s credibility, citing unsealed discovery documents from an Alabama court case and the Cass Review’s conclusion that WPATH’s guidelines—and those based on them—lack developmental rigour. It also noted the newsletter’s failure to mention the growing international shift away from paediatric medical transition in countries such as the UK, Sweden, and Finland. MLI called for the article to be corrected and urged the Globe to uphold its commitment to balanced, evidence-based journalism on this critical issue.

On June 18, Globe and Mail Standards Editor Sandra Martin responded, defending the article as a brief summary that provided a variety of links to offer further context. However, the three Globe and Mail news stories linked to in the article likewise lacked the necessary balance and context. Martin also pointed to a Canadian Paediatric Society (CPS) statement linked to in the newsletter. She argued it provided “sufficient context and qualification”—despite the fact that the CPS itself relies on WPATH’s discredited guidelines. Notwithstanding, Martin claimed the article met editorial standards and that brevity justified the lack of balance.

MLI responded that brevity does not excuse misinformation, particularly on a matter as serious as paediatric medical care, and reiterated the need for the Globe to address the scientific inaccuracies directly. MLI again called for the article to be corrected and for the unsupported suicide claim to be removed. As of this writing, the Globe has not responded.

Letter of complaint

June 9, 2025

To: The Globe and Mail

Attn: Sandra Martin, standards editor

CC: Caroline Alphonso, health editor; Mark Iype, deputy national editor and Alberta bureau chief

To the editors;

Your May 29 Morning Update: The Politics of Care by Danielle Groen, covering the Canadian Medical Association’s legal challenge to Alberta’s Bill 26, was misleading and ideologically slanted. It is journalistically irresponsible to report on contested medical claims as undisputed fact.

This issue is far too serious for such uninformed, careless journalism lacking vital perspectives and scientific context. At stake is the health and future of vulnerable children, and your reporting risks misleading parents into consenting to irreversible interventions based on misinformation.

According to The Globe and Mail’s own Journalistic Principles outlined in its Editorial Code of Conduct, the credibility of your reporting rests on “solid research, clear, intelligent writing, and maintaining a reputation for honesty, accuracy, fairness, balance and transparency.” Moreover, your principles go on to state that The Globe will “seek to provide reasonable accounts of competing views in any controversy.” The May 29 update violated these principles. There is, as I will show, a widely available body of scientific information that directly contests the claims and perspectives presented in your article. Yet this information is completely absent from your reporting.

The collapse of WPATH’s credibility

The article’s claim that Alberta’s law “falls well outside established medical practice” and could pose the “greatest threat” to transgender youth is both false and inflammatory. There is no global medical consensus on how to treat gender-distressed young people. In fact, in North America, guidelines are based on the Standards of Care developed by the World Professional Association for Transgender Health (WPATH)—an organization now indisputably shown to place ideology above evidence.

{kind=link}

For example, in a U.S. legal case over Alabama’s youth transition ban, WPATH was forced to disclose over two million internal emails. These revealed the organization commissioned independent evidence reviews for its latest Standards of Care (SOC8)—then suppressed those reviews when they found overwhelmingly low-quality evidence. Yet WPATH proceeded to publish the SOC8 as if it were evidence-based. This is not science. It is fraudulent and unethical conduct.

These emails also showed Admiral Rachel Levine—then-assistant secretary for Health in the Biden administration—pressured WPATH to remove all lower age recommendations from the guidelines—not on scientific grounds, but to avoid undermining ongoing legal cases at the state level. This is politics, not sound medical practice.

The U.K.’s Cass Review, a major multi-year investigation, included a systematic review of the guidelines in gender medicine. A systematic review is considered the gold standard because it assesses and synthesizes all the available research in a field, thereby reducing bias and providing a large comprehensive set of data upon which to reach findings. The systematic review of gender medicine guidelines concluded that WPATH’s standards of care “lack developmental rigour” and should not be used as a basis for clinical practice. The Cass Review also exposed citation laundering where medical associations endlessly recycled weak evidence across interlocking guidelines to fabricate a false consensus. This led Cass to suggest that “the circularity of this approach may explain why there has been an apparent consensus on key areas of practice despite the evidence being poor.”

Countries like Sweden, Finland, and the U.K. have now abandoned WPATH and limited or halted medicalized youth transitions in favour of a therapy-first approach. In Norway, UKOM, an independent government health agency, has made similar recommendations. This shows the direction of global practice is moving away from WPATH’s medicalized approach—not toward it. As part of any serious effort to “provide reasonable accounts of competing views,” your reporting should acknowledge these developments.

Any journalist who cites WPATH as a credible authority on paediatric gender medicine—especially in the absence of contextualizing or competing views—signals a lack of due diligence and a fundamental misunderstanding of the field. It demonstrates that either no independent research was undertaken, or it was ignored despite your editorial standards.

Puberty blockers don’t ‘buy time’ and are not reversible

Your article repeats a widely debunked claim: that puberty blockers are a harmless pause to allow young people time to explore their identity. In fact, studies have consistently shown that between 98 per cent and 100 per cent of children placed on puberty blockers go on to take cross-sex hormones. Before puberty blockers, most children desisted and reconciled with their birth sex during or after puberty. Now, virtually none do.

This strongly suggests that blocking puberty in fact prevents the natural resolution of gender distress. Therefore, the most accurate and up-to-date understanding is that puberty blockers function not as a pause, but as the first step in a treatment continuum involving irreversible cross-sex hormones. Indeed, a 2022 paper found that while puberty suppression had been “justified by claims that it was reversible … these claims are increasingly implausible.” Again, adherence to the Globe’s own editorial guidelines would require, at minimum, the acknowledgement of the above findings alongside the claims your May 29 article makes.

Moreover, it is categorically false to describe puberty blockers as “completely reversible.” Besides locking youth into a pathway of further medicalization, puberty blockers pose serious physical risks: loss of bone density, impaired sexual development, stunted fertility, and psychosocial harm from being developmentally out of sync with peers. There are no long-term safety studies. These drugs are being prescribed to children despite glaring gaps in our understanding of their long-term effects.

Given the Globe’s stated editorial commitment to principles such as “accuracy,” the crucial information from the studies linked above should be provided in any article discussing puberty blockers. At a bare minimum, in adherence to the Globe’s commitment to “balance,” this information should be included alongside the contentious and disputed claims the article makes that these treatments are reversible.

No proof of suicide prevention

The most irresponsible and dangerous claim in your article is that denying access to puberty blockers could lead to “depression, self-harm and suicide.” There is no robust evidence supporting this transition-or-suicide narrative, and in fact, the findings of the highest-quality study conducted to date found no evidence that puberty suppression reduces suicide risk.

Suicide is complex and attributing it to a single cause is not only false—it violates all established suicide reporting guidelines. Sensationalized claims like this risk creating contagion effects and fuelling panic. In the public interest, reporting on the topic of suicide must be held to the most rigorous standards, and provide the most high-quality and accurate information.

Euphemism hides medical harm

Your use of euphemistic language obscures the extreme nature of the medical interventions being performed in gender clinics. Calling double mastectomies for teenage girls “paediatric breast surgeries for gender-affirming reasons” sanitizes the medically unnecessary removal of a child’s healthy organs. Referring to phalloplasty and vaginoplasty as “gender-affirming surgeries on lower body parts” conceals the fact that these are extreme operations involving permanent disfigurement, high complication rates, and often requiring multiple revisions.

Honest journalism should not hide these facts behind comforting language. Your reporting denies youth, their parents, and the general public the necessary information to understand the nature of these interventions. Members of the general public rely greatly on the news media to equip them with such information, and your own editorial standards claim you will fulfill this core responsibility.

Your responsibility to the public

As a flagship Canadian news outlet, your responsibility is not to amplify activist messaging, but to report the truth with integrity. On a subject as medically and ethically fraught as paediatric gender medicine, accuracy is not optional. The public depends on you to scrutinize claims, not echo ideology. Parents may make irreversible decisions on behalf of their children based on the narratives you promote. When reporting is false or ideologically distorted, the cost is measured in real-world harm to some of our society’s most vulnerable young people.

I encourage the Globe and Mail to publish an updated version on this article in order to correct the public record with the relevant information discussed above, and to modify your reporting practices on this matter going forward—by meeting your own journalistic standards—so that the public receives balanced, correct, and reliable information on this vital topic.

Trustworthy journalism is a cornerstone of public health—and on the issue of paediatric gender medicine, the stakes could not be higher.

Sincerely,

Mia Hughes

Senior Fellow, Macdonald-Laurier Institute

Author of The WPATH Files

The following 41 physicians have signed to endorse this letter:

Dr. Mike Ackermann, MD

Dr. Duncan Veasey, Psy MD

Dr. Rick Gibson, MD

Dr. Benjamin Turner, MD, FRCSC

Dr. J.N. Mahy, MD, FRCSC, FACS

Dr. Khai T. Phan, MD, CCFP

Dr. Martha Fulford, MD

Dr. J. Edward Les, MD, FRCPC

Dr. Darrell Palmer, MD, FRCPC

Dr. Jane Cassie, MD, FRCPC

Dr. David Lowen, MD, FCFP

Dr. Shawn Whatley, MD, FCFP (EM)

Dr. David Zitner, MD

Dr. Leonora Regenstreif, MD, CCFP(AM), FCFP

Dr. Gregory Chan, MD

Dr. Alanna Fitzpatrick, MD, FRCSC

Dr. Chris Millburn, MD, CCFP

Dr. Julie Curwin, MD, FRCPC

Dr. Roy Eappen, MD, MDCM, FRCP (c)

Dr. York N. Hsiang, MD, FRCSC

Dr. Dion Davidson, MD, FRCSC, FACS

Dr. Kevin Sclater, MD, CCFP (PC)

Dr. Theresa Szezepaniak, MB, ChB, DRCOG

Dr. Sofia Bayfield, MD, CCFP

Dr. Elizabeth Henry, MD, CCFP

Dr. Stephen Malthouse, MD

Dr. Darrell Hamm, MD, CCFP

Dr. Dale Classen, MD, FRCSC

Dr. Adam T. Gorner, MD, CCFP

Dr. Wesley B. Steed, MD

Dr. Timothy Ehmann, MD, FRCPC

Dr. Ryan Torrie, MD

Dr. Zachary Heinricks, MD, CCFP

Dr. Jessica Shintani, MD, CCFP

Dr. Mark D’Souza, MD, CCFP(EM), FCFP*

Dr. Joanne Sinai, MD, FRCPC*

Dr. Jane Batt, MD*

Dr. Brent McGrath, MD, FRCPC*

Dr. Leslie MacMillan MD FRCPC (emeritus)*

Dr. Ian Mitchell, MD, FRCPC*

Dr. John Cunnington, MD

*Indicates physician who signed following the letter’s June 9 submission to the Globe and Mail, but in advance of this letter being published on the MLI website.

From the Fraser Institute

Two recent events exemplify the fundamental irrationality that is Canada’s electric vehicle (EV) policy.

First, the Carney government re-committed to Justin Trudeau’s EV transition mandate that by 2035 all (that’s 100 per cent) of new car sales in Canada consist of “zero emission vehicles” including battery EVs, plug-in hybrid EVs and fuel-cell powered vehicles (which are virtually non-existent in today’s market). This policy has been a foolish idea since inception. The mass of car-buyers in Canada showed little desire to buy them in 2022, when the government announced the plan, and they still don’t want them.

Second, President Trump’s “Big Beautiful” budget bill has slashed taxpayer subsidies for buying new and used EVs, ended federal support for EV charging stations, and limited the ability of states to use fuel standards to force EVs onto the sales lot. Of course, Canada should not craft policy to simply match U.S. policy, but in light of policy changes south of the border Canadian policymakers would be wise to give their own EV policies a rethink.

And in this case, a rethink—that is, scrapping Ottawa’s mandate—would only benefit most Canadians. Indeed, most Canadians disapprove of the mandate; most do not want to buy EVs; most can’t afford to buy EVs (which are more expensive than traditional internal combustion vehicles and more expensive to insure and repair); and if they do manage to swing the cost of an EV, most will likely find it difficult to find public charging stations.

Also, consider this. Globally, the mining sector likely lacks the ability to keep up with the supply of metals needed to produce EVs and satisfy government mandates like we have in Canada, potentially further driving up production costs and ultimately sticker prices.

Finally, if you’re worried about losing the climate and environmental benefits of an EV transition, you should, well, not worry that much. The benefits of vehicle electrification for climate/environmental risk reduction have been oversold. In some circumstances EVs can help reduce GHG emissions—in others, they can make them worse. It depends on the fuel used to generate electricity used to charge them. And EVs have environmental negatives of their own—their fancy tires cause a lot of fine particulate pollution, one of the more harmful types of air pollution that can affect our health. And when they burst into flames (which they do with disturbing regularity) they spew toxic metals and plastics into the air with abandon.

So, to sum up in point form. Prime Minister Carney’s government has re-upped its commitment to the Trudeau-era 2035 EV mandate even while Canadians have shown for years that most don’t want to buy them. EVs don’t provide meaningful environmental benefits. They represent the worst of public policy (picking winning or losing technologies in mass markets). They are unjust (tax-robbing people who can’t afford them to subsidize those who can). And taxpayer-funded “investments” in EVs and EV-battery technology will likely be wasted in light of the diminishing U.S. market for Canadian EV tech.

If ever there was a policy so justifiably axed on its failed merits, it’s Ottawa’s EV mandate. Hopefully, the pragmatists we’ve heard much about since Carney’s election victory will acknowledge EV reality.

Kenneth P. Green

Senior Fellow, Fraser Institute

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

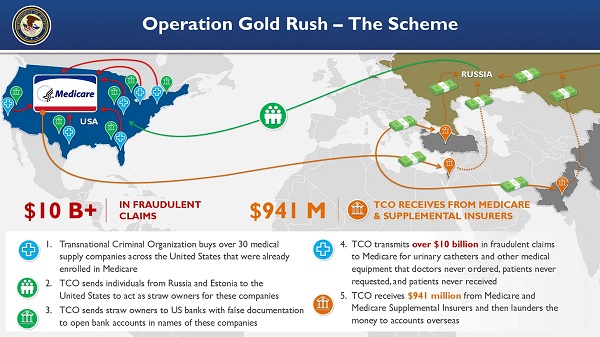

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Crime2 days ago

Crime2 days agoEyebrows Raise as Karoline Leavitt Answers Tough Questions About Epstein

-

Alberta2 days ago

Alberta2 days agoCOWBOY UP! Pierre Poilievre Promises to Fight for Oil and Gas, a Stronger Military and the Interests of Western Canada

-

Alberta2 days ago

Alberta2 days agoAlberta and Ontario sign agreements to drive oil and gas pipelines, energy corridors, and repeal investment blocking federal policies

-

Crime1 day ago

Crime1 day ago“This is a total fucking disaster”

-

International2 days ago

International2 days agoChicago suburb purchases childhood home of Pope Leo XIV

-

Fraser Institute1 day ago

Fraser Institute1 day agoBefore Trudeau average annual immigration was 617,800. Under Trudeau number skyrocketted to 1.4 million annually

-

Daily Caller2 days ago

Daily Caller2 days agoBlackouts Coming If America Continues With Biden-Era Green Frenzy, Trump Admin Warns

-

MAiD1 day ago

MAiD1 day agoCanada’s euthanasia regime is already killing the disabled. It’s about to get worse