Housing

Conservative leader Pierre Poilievre’s video on Canada’s housing crisis under Trudeau gov’t goes viral

From LifeSiteNews

‘Housing hell: How we got here and how we get out’ has been viewed more than four million times.

A video by Conservative Party of Canada (CPC) leader Pierre Poilievre exposing the country’s housing prices and supply crisis, which a taxpayer watchdog said is being fueled by high-interest rates from bad fiscal policy by Prime Minister Justin Trudeau’s government, has reached over 4 million views.

“Something new and strange has happened in Canada. Canada is sitting on probably one of the largest housing bubbles of all times, something we haven’t seen before,” Poilievre said in his 15-minute video titled Housing hell: How we got here and how we get out.

“An entire generation of youth now say they will never be able to afford a home. This is not normal for Canada.”

Housing hell: How we got here and how we get out. pic.twitter.com/vVLsXMVM35

— Pierre Poilievre (@PierrePoilievre) December 2, 2023

The video goes deep into Canada’s housing market and includes statistics on why it is in such a dire state. It currently has 4.2 million views on X (formerly Twitter) after it was released on December 2.

Poilievre documents in his video, using facts to back him up, that in the coming months and years “tens of thousands of Canadians could default on their mortgages” due to skyrocketing interest rates.

He noted how the “nightmare scenario” after “generations of affordable and stable Canadian home prices” means that 66% of a person’s average monthly income is to simply “make payments on the average single detached Canadian house.”

“Given that most of the remaining 34 percent of the family paycheck is taken out by taxes, there’s literally nothing left for food and recreation,” Poilievre noted.

Taxpayer watchdog says high house prices due to Trudeau’s out of ‘control’ government

Franco Terrazzano, federal director for the Canadian Taxpayers Federation (CTF), told LifeSiteNews that the reason house prices, along with everything else, are more expensive is due to Trudeau’s “out of control” governmental spending.

“Trudeau’s never-ending deficits and the hundreds of billions of dollars the Bank of Canada printed during the pandemic are driving up the cost of everything,” Terrazzano told LifeSiteNews.

“Life is more expensive because the cost of government is out of control.”

Terrazzano noted that governmental fiscal policy is making home prices more expensive and thus out of reach for most. He said what needs to happen is a reduction in red tape.

“Taxes and onerous government regulations are making homes more expensive,” Terrazzano told LifeSiteNews.

“If governments want to make homes more affordable, they would cut taxes and the red tape that makes it harder and more expensive to build homes.”

Terrazzano highlighted a report from the C.D. Howe Institute that shows the cost of excessive government regulations on home building.

As for Poilievre, he observed how it now would take a staggering 25 years just to save enough money to make a downpayment for a simple home in Toronto.

He continued, noting how newlyweds now on average pay $1,000 per month to rent a “single room in a townhouse that they share with two other couples.”

He also raised the issue of how 35-year-olds “live in their parent’s basements” and “rents are so high in Toronto that students live in homeless shelters.”

When it comes to middle-class workers, Poilievre emphasized how “people like nurses and carpenters now live in their vehicles.”

While housing falls primarily under provincial and municipal jurisdiction, some areas, such as interest rates, are directly influenced by the federal government.

House prices have shot up in Canada due to short supply in the market, and speculative buying and interest rates have risen to highs not seen for decades. As it stands, Canada’s interest rate sits at 5%. At this same time in 2021, interest rates were 0.25%.

This past Wednesday, the Bank of Canada decided to keep rates at 5% but did not rule out future rate increases, as it “is still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed.”

Interestingly, Trudeau put out a video the same day as Poilievre that he said was to address housing challenges. This video only has 264,000 views, however.

Curiously, Poilievre made no mention of Canada’s high immigration levels, which critics say has put a strain on an already tight supply.

Maxime Bernier, leader of the People’s Party of Canada, has been one of the only party leaders to call out high immigration levels and their effects on housing.

Trudeau’s ‘money printing’ pouring fuel on ‘inflationary fire’

According to Poilievre in his video, in the past one could save enough to buy a house by their mid-20s but said this “changed” about “eight years ago” when Trudeau came to power.

“When the government borrows and spends, it builds up the goods we buy and the interest we pay. The Trudeau government has doubled Canada’s debt, adding more debt than all prime ministers combined. Our finance minister has conceded that this deficit spending pours fuel on the inflationary fire,” Poilievre said.

He observed how excessive money printing through a banking scheme called “quantitative easing” has only benefited well-connected banking insiders and financial institutions that are awash with money.

“In recent years, the Trudeau government spending has exploded, and they’ve been borrowing more than lenders will lend. So, the Bank of Canada has started creating the cash. The money supply has therefore grown eight times faster than the economy over the last three years,” Poilievre said.

“More money bidding on fewer goods, including fewer houses, equals higher prices.”

Poilievre ended his video by stating that the “good news is housing costs were not like this before Justin Trudeau.”

“And they won’t be like this after he’s gone,” he added.

He said that the solution, besides a change in leadership, is for all levels of government to work together to cut red tape and taxes to encourage the construction of new homes.

Under Trudeau, mainly due to excessive COVID money printing, inflation has skyrocketed.

A recent report from September 5 by Statistics Canada shows food prices are rising faster than headline inflation at a rate of between 10% and 18% per year.

Earlier this year, the Bank of Canada acknowledged that Trudeau’s federal “climate change” programs, which have been deemed “extreme” by some provincial leaders, are indeed helping to fuel inflation.

![]()

Governments are not real estate developers, and Canada should take note of the failure of New Zealand’s cancelled program, highlights a new MEI publication.

“The prospect of new homes is great, but execution is what matters,” says Renaud Brossard, vice president of Communications at the MEI and contributor to the report. “New Zealand’s government also thought more government intervention was the solution, but after seven years, its project had little to show for it.”

During the federal election, Prime Minister Mark Carney promised to establish a new Crown corporation, Build Canada Homes, to act as a developer of affordable housing. His plan includes $25 billion to finance prefabricated homes and an additional $10 billion in low-cost financing for developers building affordable homes.

This idea is not novel. In 2018, the New Zealand government launched the KiwiBuild program to address a lack of affordable housing. Starting with a budget of $1.7 billion, the project aimed to build 100,000 affordable homes by 2028.

In its first year, KiwiBuild successfully completed 49 units, a far cry from the 1,000-home target for that year. Experts estimated that at its initial rate, it would take the government 436 years to reach the 100,000-home target.

By the end of 2024, just 2,389 homes had been built. The program, which was abandoned in October 2024, has achieved barely 3 per cent of its goal, when including units still under construction.

One obstacle for KiwiBuild was how its target was set. The 100,000-home objective was developed with no rigorous process and no consideration for the availability of construction labour, leading to an overestimation of the program’s capabilities.

“What New Zealand’s government-backed home-building program shows is that building homes simply isn’t the government’s expertise,” said Mr. Brossard. “Once again, the source of the problem isn’t too little government intervention; it’s too much.”

According to the Canadian Mortgage and Housing Corporation, Canada needs an additional 4.8 million homes to restore affordability levels. This would entail building between 430,000 to 480,000 new units annually. Figures on Canada’s housing starts show that we are currently not on track to meet this goal.

The MEI points to high development charges and long permitting delays as key impediments to accelerating the pace of construction.

Between 2020 and 2022 alone, development charges rose by 33 per cent across Canada. In Toronto, these charges now account for more than 25 per cent of the total cost of a home.

Canada also ranks well behind most OECD countries on the time it takes to obtain a construction permit.

“KiwiBuild shows us the limitations of a government-led approach,” said Mr. Brossard. “Instead of creating a whole new bureaucracy, the government should focus on creating a regulatory environment that allows developers to build the housing Canadians need.”

The MEI viewpoint is available here.

* * *

The MEI is an independent public policy think tank with offices in Montreal, Ottawa, and Calgary. Through its publications, media appearances, and advisory services to policymakers, the MEI stimulates public policy debate and reforms based on sound economics and entrepreneurship.

Fraser Institute

Federal government’s ‘affordable housing’ strategy doomed without strong income growth

From the Fraser Institute

By Jake Fuss and Austin Thompson

Economist Mike Moffatt estimated that, if Canadian wages grow at the average rate seen over the past two decades—and if home prices remain stable—it would still take 20 years for Canada to achieve housing affordability levels of 2005… In other words, reality remains at odds with the Carney government’s ambitious rhetoric about delivering so-called “affordable homes.”

In a recent media scrum, the Carney government’s new federal housing minister Gregor Robertson—former mayor of Vancouver—was asked: “Should home prices go down?” His response: “No, I think that we need to deliver more supply, make sure the market is stable. We need to be delivering more affordable housing.”

Robertson’s response raises a follow-up question: what does the Carney government mean when it promises “affordable housing”?

Rising house prices are nothing new. The sticker price for the average Canadian home has increased in most years, barring periods such as the 2008–09 Global Financial Crisis. And house prices aren’t expected to fall anytime soon; forecasts point to continued house price growth. But for homebuyers, the key issue isn’t that prices are increasing; it’s whether they’re rising faster than incomes. By that measure, housing in Canada has become much less affordable in recent years.

Consider Minister Robertson’s tenure as Vancouver mayor from 2008 to 2018. During that time, the price of a typical single- or semi-detached Vancouver home grew from $690,000 to $1,980,000—a 187 per cent increase. Meanwhile, the after-tax income of a typical Vancouver family rose by just 15 per cent. Today, the typical single- or semi-detached home in Vancouver costs $2,380,000. Vancouver’s housing market is somewhat unique, but strong price increases reflect a broader national trend: home prices have risen dramatically even as income growth has stagnated, largely because housing demand—driven by immigration-fuelled population growth—continues to far exceed new housing construction.

Which takes us back to the question of “affordability.” Housing can become more “affordable” even as home prices rise, so long as the after-tax incomes of Canadians grow even faster. This has happened before—after-tax wage growth exceeded house price increases in the late 1980s, for example. Unfortunately, this seems unlikely to happen in the 2020s.

In fact, while house prices have soared, wage growth in Canada has stagnated. Consequently, in 2022 (the latest year of available comparable data), the typical worker in Alberta—Canada’s highest-wage province—earned less than the typical worker in low-wage U.S. states such as Mississippi and West Virginia. And from 2014 to 2024, Canada’s GDP per-person, an indicator of incomes and living standards, grew by a mere 2.0 per cent compared to 19.6 per cent in the United States.

In a recent analysis, economist Mike Moffatt estimated that, if Canadian wages grow at the average rate seen over the past two decades—and if home prices remain stable—it would still take 20 years for Canada to achieve housing affordability levels of 2005. And of course, much could go wrong—if wage-growth estimates fall short, mortgage rates rise or house prices rise, then that slow march towards housing affordability may never end for many Canadians including young people looking to start a family.

In other words, reality remains at odds with the Carney government’s ambitious rhetoric about delivering so-called “affordable homes.”

Again, the government wants to double the rate of homebuilding in Canada in a decade. Is that possible? Currently, Canada lacks the required savings and investment to fund that level of building. And due to tepid growth of our construction workforce, we currently do not have the manpower to build twice as many homes. And as always, local opposition to rapid housing development in certain neighbourhoods and public lands may also prove hard to overcome.

But even if somehow Canada was able to marshal the resources and political capital required for such a feat, according to Minister Robertson, the end result would only be to “make sure the market is stable.” Stable, based on today’s prices, means unaffordable for many Canadians unless incomes rise. Clearly, housing supply is only half the battle. To achieve housing affordability on any reasonable timeline, the government must not only help facilitate a major expansion in homebuilding but also substantial growth in Canadian incomes—something the Trudeau government failed to do.

The key is investment, which is required to expand the housing supply, grow Canada’s economy and boost wages. In a capital-scarce economy such as Canada’s, these goals may compete with one another. So governments in Canada, including the Carney government, must adopt policies that attract investment, such as streamlining regulation and reforming capital gains taxes. And crucially, rising incomes will only translate into improved affordability if Canadians can keep more of what they earn, which will difficult given that anticipated increases in federal spending will ultimately result in a higher tax burden. Ottawa must also craft immigration and residency policies so population growth doesn’t continue to overwhelm housing supply and further increase prices.

Canadians should think about housing affordability not just in terms of housing supply but as part of a broader economic challenge—one that also depends on growing the economy, increasing savings and investment, and limiting how much governments take in taxes. Only a comprehensive strategy, centered on broad-based growth, will make the dream of homeownership a reality for generations of Canadians.

Jake Fuss

Director, Fiscal Studies, Fraser Institute

Austin Thompson

Senior Policy Analyst, Fraser Institute

New Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

The permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

Canada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Alberta9 hours ago

Alberta9 hours agoAlberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

-

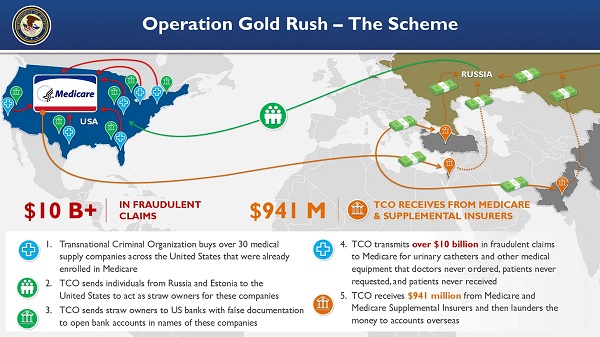

Crime8 hours ago

Crime8 hours agoNational Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Health7 hours ago

Health7 hours agoRFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

-

Bruce Dowbiggin10 hours ago

Bruce Dowbiggin10 hours agoThe Game That Let Canadians Forgive The Liberals — Again

-

Alberta1 day ago

Alberta1 day agoCOVID mandates protester in Canada released on bail after over 2 years in jail

-

Crime2 days ago

Crime2 days agoProject Sleeping Giant: Inside the Chinese Mercantile Machine Linking Beijing’s Underground Banks and the Sinaloa Cartel

-

Alberta2 days ago

Alberta2 days agoAlberta uncorks new rules for liquor and cannabis

-

Business1 day ago

Business1 day agoCanada’s loyalty to globalism is bleeding our economy dry