Business

Canada’s finances deteriorated faster than any other G7 country

From the Fraser Institute

By Jake Fuss and Grady Munro

Some analysts compare Canada’s fiscal health with other countries in the Group of Seven (G7) to downplay concerns with how Canadian governments run their finances. And while it’s true that Canada’s finances aren’t as bad some other countries, the data show Canada’s finances are deteriorating fastest in the G7, and if we’re not careful we may lose any advantage we currently have.

The G7 (Canada, France, Germany, Italy, Japan, the United Kingdom and the United States) represents seven of the world’s most advanced economies and some of Canada’s closest peer countries. As such, many commentators, organizations and governments use Canada’s standing within the group as a barometer of our fiscal health. Indeed, based on his oft-repeated goal to “build the strongest economy in the G7,” Prime Minister Carney himself clearly sees the G7 as a good comparator group for Canada.

Two key indicators of a country’s finances are government spending and debt, both of which are often measured as a share of gross domestic product (GDP) to allow for comparability across jurisdictions with various sized economies. Government spending as a share of GDP is a measure of the overall size of government in a country, while government debt-to-GDP is a measure of a country’s debt burden. Both the size of government in Canada and the country’s overall debt burden have grown over the last decade.

This is a problem because, in recent years, government spending and debt in Canada have reached or exceeded thresholds beyond which any additional spending or debt will most likely harm economic growth and living standards. Indeed, research suggests that when government spending exceeds 32 per cent of GDP, government begins to take over functions and resources better left to the private sector, and economic growth slows. However, the issues of high spending and debt are often downplayed by comparisons showing that Canada’s finances aren’t as bad as other peer countries—namely the rest of the G7.

It’s true that Canada ranks fairly well among the G7 when comparing the aforementioned measures of fiscal health. Based on the latest data from the International Monetary Fund (IMF), a new study shows that Canada’s general government (federal, provincial and local) total spending as a share of GDP was 44.7 per cent in 2024, while Canada’s general government gross debt was 110.8 per cent of GDP. Compared to the G7, Canada’s size of government ranked 4th highest while our overall debt burden ranked 5th highest.

But while Canada’s size of government and overall debt burden rank middle-of-the-pack among G7 countries, that same study reveals that Canada is not in the clear. Consider the following charts.

The first chart shows the overall change in general government total spending as a share of GDP in G7 countries from 2014 to 2024. Canada observed the largest increase in the size of government of any G7 country, as total spending compared to GDP increased 6.34 percentage points over the decade. This increase was nearly three times larger than the increase in the U.S., and both France and Italy were actually reduced their size of government during this time.

The second chart shows the overall change in general government gross debt as a share of GDP over the same decade, and again Canada experienced the largest increase of any G7 country at 25.23 percentage points. That’s considerably higher than the next closest increases in France (16.97 percentage points), the U.S. (16.36 percentage points) and the U.K. (14.13 percentage points).

Simply put, the study shows that Canada’s finances have deteriorated faster than any country in the G7 over the last decade. And if we expand this comparison to a larger group of 40 advanced economies worldwide, the results are very similar—Canada experienced the 2nd highest increase in its size of government and 3rd highest increase in its overall debt burden, from 2014 to 2024. Some analysts downplay mismanagement of government finances in Canada by pointing to other countries that have worse finances. However, if Canada continues as it has for the last decade, we’ll be joining those other countries before too long.

Jake Fuss

Director, Fiscal Studies, Fraser Institute

Grady Munro

Alberta

Pierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

From Pierre Poilievre

The Port of Prince Rupert on the north coast of British Columbia. Photo courtesy Prince Rupert Port Authority

From the Canadian Energy Centre

By Will Gibson

Moratorium does little to improve marine safety while sending the wrong message to energy investors

In 2019, Martha Hall Findlay, then-CEO of the Canada West Foundation, penned a strongly worded op-ed in the Globe and Mail calling the federal ban of oil tankers on B.C.’s northern coast “un-Canadian.”

Six years later, her opinion hasn’t changed.

“It was bad legislation and the government should get rid of it,” said Hall Findlay, now director of the University of Calgary’s School of Public Policy.

The moratorium, known as Bill C-48, banned vessels carrying more than 12,500 tonnes of oil from accessing northern B.C. ports.

Targeting products from one sector in one area does little to achieve the goal of overall improved marine transport safety, she said.

“There are risks associated with any kind of transportation with any goods, and not all of them are with oil tankers. All that singling out one part of one coast did was prevent more oil and gas from being produced that could be shipped off that coast,” she said.

Hall Findlay is a former Liberal MP who served as Suncor Energy’s chief sustainability officer before taking on her role at the University of Calgary.

She sees an opportunity to remove the tanker moratorium in light of changing attitudes about resource development across Canada and a new federal government that has publicly committed to delivering nation-building energy projects.

“There’s a greater recognition in large portions of the public across the country, not just Alberta and Saskatchewan, that Canada is too dependent on the United States as the only customer for our energy products,” she said.

“There are better alternatives to C-48, such as setting aside what are called Particularly Sensitive Sea Areas, which have been established in areas such as the Great Barrier Reef and the Galapagos Islands.”

The Business Council of British Columbia, which represents more than 200 companies, post-secondary institutions and industry associations, echoes Hall Findlay’s call for the tanker ban to be repealed.

“Comparable shipments face no such restrictions on the East Coast,” said Denise Mullen, the council’s director of environment, sustainability and Indigenous relations.

“This unfair treatment reinforces Canada’s over-reliance on the U.S. market, where Canadian oil is sold at a discount, by restricting access to Asia-Pacific markets.

“This results in billions in lost government revenues and reduced private investment at a time when our economy can least afford it.”

The ban on tanker traffic specifically in northern B.C. doesn’t make sense given Canada already has strong marine safety regulations in place, Mullen said.

Notably, completion of the Trans Mountain Pipeline expansion in 2024 also doubled marine spill response capacity on Canada’s West Coast. A $170 million investment added new equipment, personnel and response bases in the Salish Sea.

“The [C-48] moratorium adds little real protection while sending a damaging message to global investors,” she said.

“This undermines the confidence needed for long-term investment in critical trade-enabling infrastructure.”

Indigenous Resource Network executive director John Desjarlais senses there’s an openness to revisiting the issue for Indigenous communities.

“Sentiment has changed and evolved in the past six years,” he said.

“There are still concerns and trust that needs to be built. But there’s also a recognition that in addition to environmental impacts, [there are] consequences of not doing it in terms of an economic impact as well as the cascading socio-economic impacts.”

The ban effectively killed the proposed $16-billion Eagle Spirit project, an Indigenous-led pipeline that would have shipped oil from northern Alberta to a tidewater export terminal at Prince Rupert, B.C.

“When you have Indigenous participants who want to advance these projects, the moratorium needs to be revisited,” Desjarlais said.

He notes that in the six years since the tanker ban went into effect, there are growing partnerships between B.C. First Nations and the energy industry, including the Haisla Nation’s Cedar LNG project and the Nisga’a Nation’s Ksi Lisims LNG project.

This has deepened the trust that projects can mitigate risks while providing economic reconciliation and benefits to communities, Dejarlais said.

“Industry has come leaps and bounds in terms of working with First Nations,” he said.

“They are treating the rights of the communities they work with appropriately in terms of project risk and returns.”

Hall Findlay is cautiously optimistic that the tanker ban will be replaced by more appropriate legislation.

“I’m hoping that we see the revival of a federal government that brings pragmatism to governing the country,” she said.

“Repealing C-48 would be a sign of that happening.”

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

Federal fiscal anchor gives appearance of prudence, fails to back it up

The Passage of Bill C-5 Leaves the Conventional Energy Sector With as Many Questions as Answers

-

Business1 day ago

Business1 day agoOttawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

COVID-192 days ago

COVID-192 days agoNew Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Business1 day ago

Business1 day agoWorld Economic Forum Aims to Repair Relations with Schwab

-

Alberta2 days ago

Alberta2 days agoThe permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

-

Alberta1 day ago

Alberta1 day agoAlberta’s government is investing $5 million to help launch the world’s first direct air capture centre at Innisfail

-

Business1 day ago

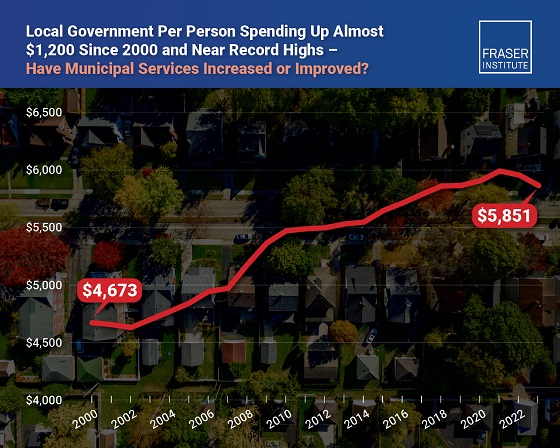

Business1 day agoMunicipal government per-person spending in Canada hit near record levels

-

Business1 day ago

Business1 day agoA new federal bureaucracy will not deliver the affordable housing Canadians need