Business

Canadian Taxpayer Federation calls on Ottawa to rescind recent Carbon Tax hike

From the Canadian Taxpayer Federation

Ottawa’s carbon tax hike out of step with global reality

by Aaron Wudrick, Federal Director and Franco Terrazzano, Alberta Director

(This column originally appeared in the Financial Post)

Prime Minister Justin Trudeau has chosen to make life more expensive by increasing the federal carbon tax by 50 per cent amidst the COVID-19 economic and health crisis. Meanwhile, governments around the world are moving in the opposite direction because hiking taxes during a global pandemic is a bad idea.

Provinces have already tapped the breaks on their own carbon tax hikes. British Columbia Premier John Horgan announced that he would not be going forward with his planned April 1 carbon tax hike. Instead of mirroring the federal carbon tax hike, Newfoundland and Labrador is maintaining its tax at $20 per tonne. The price of carbon allowances in the Quebec-California cap and trade system have also fallen due to COVID-19 and the current macroeconomic realities.

The European Union’s cap and trade scheme, which applies to 30 countries, has also seen its carbon tax rate drop significantly. For most of 2019 and early 2020, EU carbon prices traded around €25 per tonne before nosediving to around €15 per tonne in March. The EU’s cap and trade carbon tax rate has fallen 32 per cent below its 2020 peak, according to the most recent data available on the ICAP Allowance Price Explorer. While the tax rate has increased since bottoming out, S&P Global Platts Analytics forecasts the COVID-19 shock keeping downward pressure on the cap and trade market.

Other counties are providing further carbon tax relief. The Norwegian government reduced its carbon tax rate on natural gas and liquified petroleum gas to zeroand will keep the rates below the pre-coronavirus level until 2024. Norway also deferred payments on various fuel taxes until June 18.

Estonia Finance Minister Martin Helme formally called for his country to consider leaving the EU’s cap and trade carbon tax system to provide relief. The prime minister later announced that Estonia would not seek to leave the EU’s carbon tax system, but the Estonian government lowered the excise tax on electricity to the minimum allowed by the EU and lowered its excise tax on diesel, light and heavy fuel oil, shale oil and natural gas.

“Due to the economic downturn, both people’s incomes and the revenue of companies are declining, but daily household expenses such as electricity or gas bills still need to be paid. To better cope with them, we are reducing excise duty rates on gas and electricity for two years,” Helme explained.

Outside of the EU, the United Kingdom is saving its taxpayers between £15 and £20 million per year by walking back its plan to increase its carbon tax top-up, New Zealand’s cap and trade tax rate has fallen by more than 20 per cent this year and South Africa pushed back carbon tax payments by three months.

It’s worth noting that it’s unlikely Canada’s carbon tax will have any meaningful impact on global emissions. Only 45 countries (out of 195 countries worldwide) are covered by a carbon tax, and only 15.6 per cent of total emissions are covered by these carbon taxes, according to the World Bank. Furthermore, about half of the emissions covered by carbon taxes are priced below US$10/tCO2e – significantly lower than Canada’s federal rate and too low to make a difference.

With Canada only accounting for 1.5 per cent of global emissions, it’s easy to understand Trudeau’s acknowledgement that, “even if Canada stopped everything tomorrow, and the other countries didn’t have any solutions, it wouldn’t make a big difference.”

Now more than ever, Canadian taxpayers need relief. With carbon tax burdens declining around the globe during the COVID-19 crisis, walking back the recent carbon tax hike should be a no-brainer for our federal government.

Province of Alberta replies to Joe Biden’s promise to cancel Keystone XL

Racket News

Racket News

By Eric Salzman

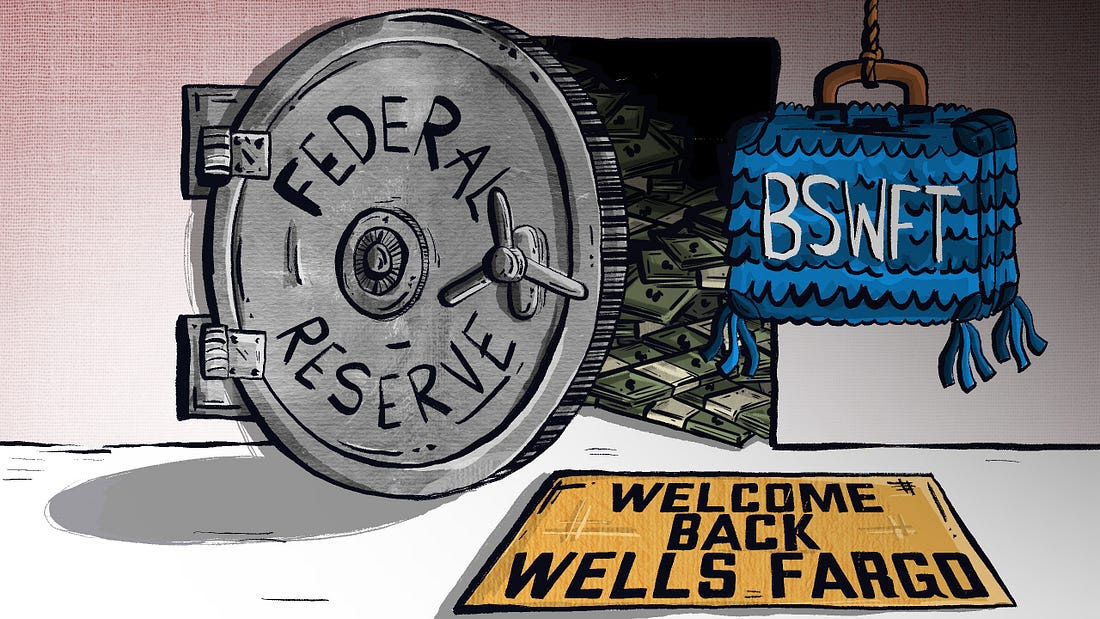

The heavyweight champion of financial crime gets seemingly its millionth chance to show it’s reformed

The past two decades have been tough ones for Wells Fargo and the many victims of its sprawling crime wave. While the banking industry is full of scammers, Wells took turning time honored street-hustles into multi-billion dollar white-collar hustles to a new level.

The Federal Reserve announced last month that Wells Fargo is no longer subject to the asset growth restriction the Fed finally enforced in 2018 after multiple scandals. This was a major enforcement action that prohibited Wells from growing existing loan portfolios, purchasing other bank branches or entering into any new activities that would result in their asset base growing.

Upon hearing the news that Wells was being released from the Fed’s penalty box, my mind turned to this pivotal moment in the classic movie “Slapshot.”

Here are some of Wells Fargo’s lowlights both before and after the Fed’s enforcement action:

- December 2022: Wells Fargo paid more than $2 billion to consumers and $1.7 billion in civil penalties after the Consumer Financial Protection Bureau (CFPB) found mismanagement — including illegal fees and interest charges — in several of its biggest product lines, such as auto loans, mortgages, and deposit accounts.

- September 2021: Wells Fargo paid $72.6 million to the Justice Department for overcharging foreign exchange customers from 2010-2017.

- February 2020: Wells Fargo paid $3 billion to settle criminal and civil investigations by the Justice Department and SEC into its aggressive sales practices between 2002 and 2016. About $500 million was eventually distributed to investors.

- January 2020: The Office of the Comptroller of the Currency (OCC) banned two senior executives, former CEO John Stumpf and ex-Head of Community Bank Carrie Tolstedt, from the banking industry. Stumpf and Tolstedt also incurred civil penalties of $17.5 million and $17 million.

- August 2018: The Justice Department levied a $2.09 billion fine on Wells Fargo for its actions during the subprime mortgage crisis, particularly its mortgage lending practices between 2005 and 2007.

- April 2018: Federal regulators at the CFPB and OCC examined Wells’ auto loan insurance and mortgage lending practices and ordered the bank to pay $1 billion in damages.

- February 2018: The aforementioned Fed enforcement action. In addition to the asset growth restriction, Wells was ordered to replace three directors.

- October 2017: Wells Fargo admitted wrongdoing after 110,000 clients were fined for missing a mortgage payment deadline — delays for which the bank was ultimately deemed at fault.

- July 2017: As many as 570,000 Wells Fargo customers were wrongly charged for auto insurance on car loans after the bank failed to verify whether those customers already had existing insurance. As a result, up to 20,000 customers may have defaulted on car loans.

- September 2016: Wells Fargo acknowledged its employees had created 1.5 million deposit accounts and 565,000 credit card accounts between 2002 and 2016 that “may not have been authorized by consumers,” according to CFPB. As a result, the lender was forced to pay $185 million in damages to the CFPB, OCC, and City and County of Los Angeles.

Additionally, somehow in 2023 Wells even managed to drop $1 billion in a civil settlement with shareholders for overstating their progress in complying with their 2018 agreement with the Fed to clean themselves up!

I imagine if Wells were in any other business, it wouldn’t be allowed to continue. But Wells is part of the “Too Big to Fail” club. Taking away its federal banking charter would be too disruptive for the financial markets, so instead they got what ended up being a seven-year growth ban. Not exactly rough justice.

While not the biggest settlement, my favorite Wells scam was the 2021 settlement of the seven-year pilfering operation, ripping off corporate customers’ foreign exchange transactions.

Like many banks, Wells Fargo offers its corporate clients with global operations foreign exchange (FX) services. For example, if a company is based in the U.S. but has extensive dealings in Canada, it may receive payments in Canadian dollars (CAD) that need to be exchanged for U.S. dollars (USD) and vice versa. Wells, like many banks, has foreign exchange specialists who do these conversions. Ideally, the banks optimize their clients’ revenue and decrease risk, in return for a markup fee, or “spread.”

There’s a lot of trust involved with this activity as the corporate customers generally have little idea where FX is trading minute by minute, nor do they know what time of day the actual orders for FX transactions — commonly called “BSwifts” — come in. For an unscrupulous bank, it’s a license to steal, which is exactly what Wells did.

According to the complaint, Wells regularly marked up transactions at higher spreads than what was agreed upon. This was just one of the variety of naughty schemes Wells used to clobber their customers. My two favorites were “The Big Figure Trick” and the “BSwift Pinata.”

The Big Figure Trick

Let’s say a client needs to sell USD for CAD, and that the $1 USD is worth $1.32 CAD. In banking parlance, the 32 cents is called the “Big Figure.” Wells would buy the CAD at $1.32 for $1 USD and then transpose the actual exchange rate on the customer statement from $1.32 to $1.23. If the customer didn’t notice, Wells would pocket the difference. On a transaction where the client is buying 5 million CAD with USD, the ill-gotten gain for Wells would be about $277,000 USD!

Conversely, if the customer did notice the difference, Wells would just blame it on the grunts in its operational back office, saying they accidentally transposed the number and “correct” the transaction. From the complaint, here is some give and take between two Wells FX specialists:

“You can play the transposition error game if you get called out.” Another FX sales specialist noted to a colleague about a previous transaction that a customer “didn’t flinch at the big fig the other day. Want to take a bit more?”

The BSwift Piñata

The way this hustle would work is, let’s say the Wells corporate customer was receiving payment from one of their Canadian clients. The Canadian client’s bank would send a BSwift message to Wells. The Wells client was in the dark about the U.S. dollar-Canadian dollar exchange rate because it had no idea what time of day the message arrived. Wells took advantage of that by purchasing U.S. dollars for Canadian dollars first. For simplicity, think of the U.S. dollar-Canadian dollar exchange rate as a widget that Wells bought for $1. If the widget increased in value, say to $1.10 during the day, Wells would sell the widget they purchased for $1 to the client for $1.10 and pocket 10 cents. If the price of the widget Wells bought for $1 fell to 95 cents, Wells would just give up their $1 purchase to the client, plus whatever markup they agreed to.

Heads, Wells wins. Tails, client loses.

The complaint notes that a Wells FX specialist wrote that he:

“Bumped spreads up a pinch,” that “these clients who are in the mode of just processing wires will most likely not notice this slight change in pricing” and that it “could have a very quick positive impact on revenue without a lot of risk.”

Talk about a boiler room operation. Personally, I think calling what you are doing to a client a “piñata” should have easily put Wells in the Fed’s penalty box another 5 years at least!

Wells has been released from the Fed’s 2018 enforcement order. I would like to think they have learned their lesson and are reformed, but I would lay good odds against it. A leopard can’t change its spots.

Racket News is a reader-supported publication.

Consider becoming a free or paid subscriber.

Alberta

Pierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

From Pierre Poilievre

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

Federal fiscal anchor gives appearance of prudence, fails to back it up

-

Business2 days ago

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

COVID-192 days ago

COVID-192 days agoNew Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Alberta2 days ago

Alberta2 days agoThe permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

-

Business2 days ago

Business2 days agoWorld Economic Forum Aims to Repair Relations with Schwab

-

Alberta2 days ago

Alberta2 days agoAlberta’s government is investing $5 million to help launch the world’s first direct air capture centre at Innisfail

-

Business2 days ago

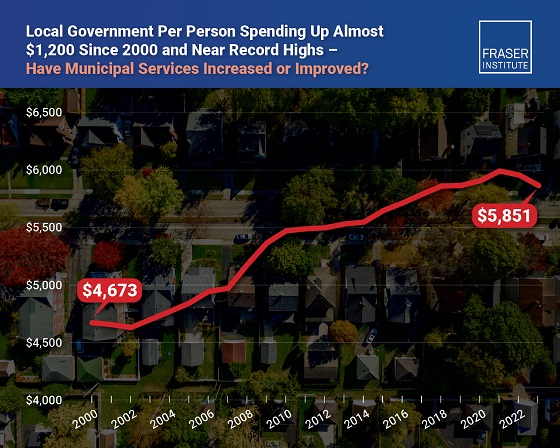

Business2 days agoMunicipal government per-person spending in Canada hit near record levels

-

Business2 days ago

Business2 days agoA new federal bureaucracy will not deliver the affordable housing Canadians need