Business

Canada’s risky and misguided bet on EV battery manufacturing

From the Macdonald Laurier Institute

By Tom McCaffrey and Denaige McDonnell for Inside Policy

By investing $52.5 billion in a handful of foreign-controlled companies, the government has failed to create a sustainable, long-term economic advantage. Instead of fostering innovation and building a robust, homegrown supply chain, Canada has committed itself to an outdated model of industrial policy that relies on foreign entities and low-value manufacturing jobs.

Two years ago, Canada’s minister of natural resources urged Canadians “to fully seize” the economic opportunity presented by the country’s abundant critical minerals.

“We must ensure that value is added to the entire supply chain, including exploration, extraction, intermediate processing, advanced manufacturing, and recycling,” Jonathan Wilkinson stated. “We must create the necessary conditions for Canadian companies to grow, scale-up, and expand globally in markets that depend on critical minerals.”

Two years later, the Canadian government has gone all-in with a $52.5 billion dollar bet on EV battery manufacturing in Ontario and Quebec. The decision goes against the recommendations of industry specialists and the government’s own departments responsible for strategic development who advised officials to go slow, steady, and think full supply chain development when targeting incentives.

Why didn’t the politicians listen?

Ottawa’s risky bet on EV battery manufacturing

By 2033, the Parliamentary Budget Officer (PBO) estimates three recent Canadian Government EV battery manufacturing subsidies will cost the country a total $37.7 billion dollars. The Northvolt, Volkswagen, Stellantis-LGES manufacturing facilities are estimated to take 15 years to pay back Canadian taxpayers.

The repayment estimate is 6 years longer than the government originally estimated because the PBO has now used the manufacturers’ production rate estimations, a more conservative number, than the originally used full production rates. In total, the national investment across the full value chain of EV battery manufacturing equates to $52.5 billion into just 13 companies.

The Canadian government is betting big on EVs, but not by investing in innovation, intellectual property, or Canadian technology. It is betting the farm on foreign entities delivering 8,500 manufacturing jobs. Capital investment for the purpose of growth in labour productivity isn’t a new strategy and it can be effective, but at $4 million per job the likelihood of return on investment is low.

Could the Bet Pay Off?

The global EV battery market is expected to surge over the next 10 years from US$132.6 billion in 2023 to US$508.8 by 2033. So far, growth has been slower than expected, and some major players, like Tesla, will be challenged to meet their sales volumes from last year according to analysts – but basing an opinion on a single year of car sales is not wise.

The truth is car manufacturing in Canada is important to our GDP ($14.6 billion) and to jobs (125,000). It is also true that Canada has lost 50 per cent of its market share in manufacturing of cars ($8 billion in 2000 to $4 billion in 2022), but it has maintained it market share in motor vehicle parts ($9 billion).

Canada appears to be betting that it can maintain it’s position in the car automotive industry rather than cementing its place in the battery metals and manufacturing value chain. But is this wager wise?

Sustainable policy development

Governments can encourage economic and industrial development in several ways. Policy-makers can set efficient regulations and approval mechanisms; create frameworks that build a bridge between government and the private sector; support the development of skilled labour and innovation ecosystems; enable direct collaboration and procurement mechanisms between industry, academia, innovation ecosystems, and government; and share a clear vision and pathway for industrial growth.

Governments can also use subsidies and tax credits to create market share, but there is growing concern that using these methods to create or protect markets will cause more harm than opportunity in developing countries. These kinds of investments risk triggering international protectionism and geopolitical trade-offs as nations turn inward rather than collaborating for development.

What’s needed is a sustainable policy approach – one that influences and benefits the largest subset of market outcomes, including start-up development, foreign direct investment, technology development, technology adoption, investment attraction, the creation of circular economy value chains, and more.

Ottawa’s misguided approach to economic investment

In the EV world, a fully integrated supply chain that includes mining, chemical processing, battery production, and recycling is critical. The battery value chain road map published by Innovation, Science and Economic Development (ISED) Canada, and the Canadian Critical Minerals Strategy published by Natural Resources Canada (NRC) both call for government to develop the full supply chain.

In 2021, a standing committee advised how best to develop the full supply chain. That same year Clean Energy Canada wrote a report on how Canada could build the domestic battery industry across the country, and in 2022 another full suite of associations including the Battery Metals Association, Energy Futures Lab, Transition Accelerator, and Accelerate ZEV developed a roadmap to develop Canada’s battery value chain.

The Canadian industrial policies being used to create the EV supply chain are a mix of production subsidies, investment tax credits, foregone corporate income tax revenue, construction capital expenses, and other monetary supports. Though large, the $52.5 billion investment ignores key aspects of the upstream supply chain (mining, refining, etc.) that would allow us to reap full value from EV battery production. Worse, it comes at a time when automakers are pulling back from EV investments due to lower than expected demands, making the investment increasingly risky given changing market conditions.

By flying in the face of the very industries it supports and specialists it employs, it raises the question: why is Canadian government failing to follow its own strategy? Why choose to support an undeveloped strategy that banks on foreign investment and manufacturing jobs when experts across Canada’s supply chain, and two government departments, had a fulsome and balanced approach to supply chain development? Why shun a balanced approach to government investment focused on building out the entire supply chain?

Where Canada continues to go astray

Canada’s investment strategies have long been plagued by short-term thinking, favouring politically motivated quick wins over sustainable, long-term value creation. The government’s $52.5 billion bet on EV battery manufacturing is a prime example—subsidizing foreign companies while neglecting the development of critical upstream supply chains and domestic innovation. This approach leaves Canada reliant on international markets for critical materials, with little to show in terms of intellectual property or R&D growth.

By ignoring expert advice and focusing on politically strategic regions, Canada misses opportunities to build fully integrated industries across the country, ultimately failing to support homegrown solutions that could foster long-term economic resilience. Instead, Canada continues to prioritize high-risk, low-return investments, with little consideration for the foundational elements needed for a competitive, innovative economy.

Research on industrial policy shows countries are better served when governments focus on delivering well-designed policies aimed at improving general business environments than attempting to artificially create new markets. This is why industrial policies went out of vogue more than two decades ago.

It raises the question – are there examples of successful government interventions that seeded new sectors?

How the Asia-Pacific region cornered the semiconductor market

In the 1980s both the South Korea and Taiwanese governments made strategic early investments in companies that were well positioned to accelerate growth of the semiconductor sector. Today, the Asia-Pacific region is dominating the global market share of what has become a US$620 billion industry. Both South Korea and Taiwan were investing in the semiconductor industry in the 1960s. From a policy perspective, the two countries took similar approaches and focused their state-directed capital allocations to companies like Samsung LG and the Taiwan Semiconductor Manufacturing Company (TSMC). Through strong government support, both countries created technology institutes, centres for research and development, infrastructure and tax incentives, tax holidays, and interest-free loans.

Those investments helped to seed highly successful sectors in each country. Both countries continue to invest tax dollars back into the sector to help maintain the competitive advantages they helped to foster. South Korea’s semiconductor industry received a $US19 billion show of support from its government earlier this year to create a comprehensive support program spanning financial, research and development, and infrastructure support. The investment is part of a decades long commitment to the semiconductor industry which now accounts for nearly 20 per cent of total exports and plays a leading role in the South Korean economy. In Taiwan, the semiconductor sector is a powerhouse that accounts for 15 per cent of the national GDP and ranks number one globally for wafer foundry and packaging and testing, and number two for integrated circuit (IC) design.

These successes were largely enabled by government-controlled economies and early, and ongoing support to industry. This support did not waiver for decades. It is unlikely that Canada will be able to maintain this level of stability and government focus.

Other factors like access to cheap labour, willingness to specialize, commitment to product quality, and streamlined manufacturing played an important role.

Policy Challenges: Economic and Political Complexities

The challenge of creating successful industrial policy is that it is complex, long-term, has uncertain benefits, and requires government departments to have deep industry expertise. Experts worry that the current federal government simply isn’t up to the task.

In 2023, more than 2,500 new industrial policies were introduced globally, and more than 70 per cent were subsidies, tariffs, or import/export restrictions. These policies create trade distortion more often than they lead to market creation. Trade distortion can unfairly tilt the playing field in favour of domestic industries, often at the expense of foreign competitors.

With Canada’s recent industrial policy on EV battery manufacturing, we are choosing to distort our own economy.

Industrial policies strain global trade and economic relations. Such policies can have wide-ranging effects on both the implementing country and the global economy. They also appear protectionist even to allied nations.

How can Canada get it right?

Many of Canada’s mature sectors have enjoyed government support or protection at some point in our nation’s history. Past Canadian governments have protected the industries of their time, be it agriculture, steel manufacturing, pulp and paper, aerospace, and even defence.

There are recent examples of small sums of government dollars creating big wins for Canada’s homegrown innovation and sustainability economy.

At the provincial level, one organization that stands out is Emissions Reduction Alberta (ERA), an arms-length provincial organization that has weather several changes in government in its 15 years. ERA uses Technology Innovation and Emissions Reduction dollars to invest in late-stage sustainable technology. To date, the organization has invested almost $1 billion dollars into 277 technologies at a ratio of 8 industry dollars to 1 ERA dollar.

Federally, Prairies Economic Development Canada (PrairiesCan) is an example of a highly innovative approach to economic development. It has invested millions of dollars in repayable interest-free loans and regional innovation ecosystem supports. Ecosystem supports include accelerators and incubators that have exponentially increased the success of start ups and mature firms alike.

PrairiesCan and ERA operate on annual budgets of $300 million and $50–200 million, respectively. These dollars employ various types of expertise and invest across large swaths of the mature and new economy. They look across hundreds of organizations, understand the regional context, varying business dynamics and make strategic investments.

If government persists in committing tax dollars to the growth of the economy, then it should draw inspiration from these kinds of organizations.

Do Governments Make Effective Market Makers?

Canadians are rightly skeptical about Ottawa’s $52.5 billion bet on EV battery manufacturing.

Ottawa is rolling the dice that it will make Canada a leader in battery supply chains. It’s one of the largest industrial policy bets we have seen in our lifetimes. However, industrial policy analysts are warning about the risk of misallocation of funds.

Expert critics say Canada’s economy is too reliant on government-driven innovation policies. These researchers believe that competition creates markets, and that the government should commit to focusing on reducing policy and regulatory barriers. Many still believe in the capitalist ethos – that fostering a cultural and economic environment that naturally supports risk-taking and competition is the best route to success. The same people would note that the natural process of business turnover is essential for innovation and growth.

Conclusion

Canada’s current strategy of picking winners through massive, targeted subsidies is not just risky – it’s short-sighted. By investing $52.5 billion in a handful of foreign-controlled companies, the government has failed to create a sustainable, long-term economic advantage. Instead of fostering innovation and building a robust, homegrown supply chain, Canada has committed itself to an outdated model of industrial policy that relies on foreign entities and low-value manufacturing jobs. This approach ignores the foundational elements that drive true competitiveness – innovation, R&D, and full value chain development.

What Canada needs is a fundamental shift in its investment strategy. Instead of betting the farm on politically motivated, high-risk subsidies, the government should focus on strengthening ecosystems that support innovation, entrepreneurship, and domestic industry. Investments should be directed at building a fully integrated supply chain that includes mining, refining, and manufacturing, while supporting Canadian companies that will keep intellectual property and jobs at home.

If Canada continues down the current path, it risks becoming a player in someone else’s game, perpetually reliant on foreign companies and global markets. The country should seize this moment to redefine its complete industrial strategy, making bold investments in innovation and infrastructure that can secure economic resilience for generations to come. Without this shift, Canada’s $52.5 billion bet may very well be remembered as one of the biggest missed opportunities in modern economic history.

Tom McCaffery, M.B.A., is the CEO and managing director of Two River Advisory and former executive director of policy and engagement for Emissions Reduction Alberta.

Denaige McDonnell, Ph.D., is an accomplished business management strategist and CEO of People Risk Management, specializing in organizational systems, culture, and psychological safety.

Business

The world is no longer buying a transition to “something else” without defining what that is

From Resource Works

Even Bill Gates has shifted his stance, acknowledging that renewables alone can’t sustain a modern energy system — a reality still driving decisions in Canada.

You know the world has shifted when the New York Times, long a pulpit for hydrocarbon shame, starts publishing passages like this:

“Changes in policy matter, but the shift is also guided by the practical lessons that companies, governments and societies have learned about the difficulties in shifting from a world that runs on fossil fuels to something else.”

For years, the Times and much of the English-language press clung to a comfortable catechism: 100 per cent renewables were just around the corner, the end of hydrocarbons was preordained, and anyone who pointed to physics or economics was treated as some combination of backward, compromised or dangerous. But now the evidence has grown too big to ignore.

Across Europe, the retreat to energy realism is unmistakable. TotalEnergies is spending €5.1 billion on gas-fired plants in Britain, Italy, France, Ireland and the Netherlands because wind and solar can’t meet demand on their own. Shell is walking away from marquee offshore wind projects because the economics do not work. Italy and Greece are fast-tracking new gas development after years of prohibitions. Europe is rediscovering what modern economies require: firm, dispatchable power and secure domestic supply.

Meanwhile, Canada continues to tell itself a different story — and British Columbia most of all.

A new Fraser Institute study from Jock Finlayson and Karen Graham uses Statistics Canada’s own environmental goods and services and clean-tech accounts to quantify what Canada’s “clean economy” actually is, not what political speeches claim it could be.

The numbers are clear:

- The clean economy is 3.0–3.6 per cent of GDP.

- It accounts for about 2 per cent of employment.

- It has grown, but not faster than the economy overall.

- And its two largest components are hydroelectricity and waste management — mature legacy sectors, not shiny new clean-tech champions.

Despite $158 billion in federal “green” spending since 2014, Canada’s clean economy has not become the unstoppable engine of prosperity that policymakers have promised. Finlayson and Graham’s analysis casts serious doubt on the explosive-growth scenarios embraced by many politicians and commentators.

What’s striking is how mainstream this realism has become. Even Bill Gates, whose philanthropic footprint helped popularize much of the early clean-tech optimism, now says bluntly that the world had “no chance” of hitting its climate targets on the backs of renewables alone. His message is simple: the system is too big, the physics too hard, and the intermittency problem too unforgiving. Wind and solar will grow, but without firm power — nuclear, natural gas with carbon management, next-generation grid technologies — the transition collapses under its own weight. When the world’s most influential climate philanthropist says the story we’ve been sold isn’t technically possible, it should give policymakers pause.

And this is where the British Columbia story becomes astonishing.

It would be one thing if the result was dramatic reductions in emissions. The provincial government remains locked into the CleanBC architecture despite a record of consistently missed targets.

Since the staunchest defenders of CleanBC are not much bothered by the lack of meaningful GHG reductions, a reasonable person is left wondering whether there is some other motivation. Meanwhile, Victoria’s own numbers a couple of years ago projected an annual GDP hit of courtesy CleanBC of roughly $11 billion.

But here is the part that would make any objective analyst blink: when I recently flagged my interest in presenting my research to the CleanBC review panel, I discovered that the “reviewers” were, in fact, two of the key architects of the very program being reviewed. They were effectively asked to judge their own work.

You can imagine what they told us.

What I saw in that room was not an evidence-driven assessment of performance. It was a high-handed, fact-light defence of an ideological commitment. When we presented data showing that doctrinaire renewables-only thinking was failing both the economy and the environment, the reception was dismissive and incurious. It was the opposite of what a serious policy review looks like.

Meanwhile our hydro-based electricity system is facing historic challenges: long term droughts, soaring demand, unanswered questions about how growth will be powered especially in the crucial Northwest BC region, and continuing insistence that providers of reliable and relatively clean natural gas are to be frustrated at every turn.

Elsewhere, the price of change increasingly includes being able to explain how you were going to accomplish the things that you promise.

And yes — in some places it will take time for the tide of energy unreality to recede. But that doesn’t mean we shouldn’t be improving our systems, reducing emissions, and investing in technologies that genuinely work. It simply means we must stop pretending politics can overrule physics.

Europe has learned this lesson the hard way. Global energy companies are reorganizing around a 50-50 world of firm natural gas and renewables — the model many experts have been signalling for years. Even the New York Times now describes this shift with a note of astonishment.

British Columbia, meanwhile, remains committed to its own storyline even as the ground shifts beneath it. This isn’t about who wins the argument — it’s about government staying locked on its most basic duty: safeguarding the incomes and stability of the families who depend on a functioning energy system.

Resource Works News

“It’s a good a bet that high-speed rail between Toronto and Quebec City isn’t even among the top 1,000 priorities for most Canadians.”

The Canadian Taxpayers Federation is criticizing Prime Minister Mark Carney for borrowing billions more for high-speed rail between Toronto and Quebec City.

“Canadians need help paying for basics, they don’t need another massive bill from the government for a project that only benefits one corner of the country,” said Franco Terrazzano, CTF Federal Director. “It’s a good a bet that high-speed rail between Toronto and Quebec City isn’t even among the top 1,000 priorities for most Canadians.

“High-speed rail will be another costly taxpayer boondoggle.”

The federal government announced today that the first portion of the high-speed rail line will be built between Ottawa and Montreal with constructing starting in 2029. The entire high-speed rail line is expected to go between Toronto and Quebec City.

The federal Crown corporation tasked with overseeing the project “estimated that the full line will cost between $60 billion and $90 billion, which would be funded by a mix of government money and private investment,” the Globe and Mail reported.

The government already owns a railway company, VIA Rail. The government gave VIA Rail $1.9 billion over the last five years to cover its operating losses, according to the Crown corporation’s annual report.

The federal government is borrowing about $78 billion this year. The federal debt will reach $1.35 trillion by the end of this year. Debt interest charges will cost taxpayers $55.6 billion this year, which is more than the federal government will send to the provinces in health transfers ($54.7 billion) or collect through the GST ($54.4 billion).

“The government is up to its eyeballs in debt and is already spending hundreds of millions of dollars bailing out its current train company, the last thing taxpayers need is to pay higher debt interest charges for a new government train boondoggle,” Terrazzano said. “Instead of borrowing billions more for pet projects, Carney needs to focus on making life more affordable and paying down the debt.”

University of Colorado will pay $10 million to staff, students for trying to force them to take COVID shots

Wayne Gretzky’s Terrible, Awful Week.. And Soccer/ Football.

Integration Or Indignation: Whose Strategy Worked Best Against Trump?

Western Campuses Help Build China’s Digital Dragnet With U.S. Tax Funds, Study Warns

-

International2 days ago

International2 days agoTrump admin wants to help Canadian woman rethink euthanasia, Glenn Beck says

-

Local Business2 days ago

Local Business2 days agoRed Deer Downtown Business Association to Wind Down Operations

-

COVID-192 days ago

COVID-192 days agoTrump DOJ seeks to quash Pfizer whistleblower’s lawsuit over COVID shots

-

Alberta2 days ago

Alberta2 days agoThe case for expanding Canada’s energy exports

-

Crime2 days ago

Crime2 days agoU.S. seizes Cuba-bound ship with illicit Iranian oil history

-

Business1 day ago

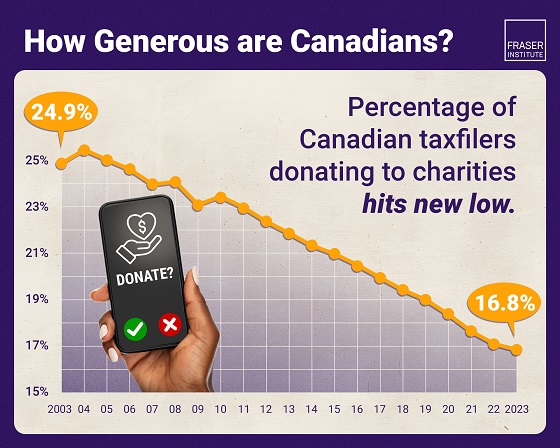

Business1 day agoAlbertans give most on average but Canadian generosity hits lowest point in 20 years

-

International2 days ago

International2 days agoMarjorie Taylor Greene’s ’60 Minutes’ interview reveals power struggle between populists and RINOs

-

Censorship Industrial Complex1 day ago

Censorship Industrial Complex1 day agoOttawa’s New Hate Law Goes Too Far