Business

Natural gas bans are fuelling higher energy costs

This article supplied by Troy Media.

![]() By Roslyn Kunin

By Roslyn Kunin

Governments are pulling the plug on natural gas with no real backup plan in place and Canadians are paying the price

Banning natural gas and pushing electricity without enough supply is a recipe for soaring energy costs and blackouts. Politicians may forget the basics of economics, but supply and demand won’t go away.

When the supply of anything goes up, its price falls. Limit or decrease supply and the price rises. Demand works in the opposite direction—high demand drives up prices, and lower demand brings them down.

Like gravity, the law of supply and demand is always there, but many politicians behave as though it doesn’t exist. Nowhere is that clearer than in energy policy, where environmental goals are prioritized while economic realities are sidelined. The drive to eliminate energy-related emissions

in just a few years may sound noble, but it ignores practical limits, and Canadians are paying the price.

Take natural gas. It emits far less carbon than coal or oil. In Canada, most natural gas comes from Alberta and British Columbia, and it’s one of the country’s most affordable and secure energy sources. Despite this, several jurisdictions in B.C. are banning its use in new and renovated buildings—moves encouraged by federal emissions targets and climate incentives.

These policies may be well-intentioned, but they ignore a basic fact: people still need to heat their homes and cook their meals. Without gas, they’ll be forced to use electricity. But unlike gas, electricity is already in short supply and getting more expensive. Our current generating capacity can’t keep up with rising demand, and that’s before we even consider the added strain from electric vehicles, data centres and energy-hungry artificial intelligence.

British Columbia’s Site C dam, a multibillion-dollar hydroelectric project under construction on the Peace River, is expected to generate enough electricity for 450,000 homes when complete. But all of that power is already spoken for. There are no Site C-scale replacements on the horizon. Meanwhile, our distribution infrastructure can’t meet today’s needs, let alone tomorrow’s.

In one recent case, buildings planning to install EV chargers were told by B.C. Hydro, the Crown corporation responsible for electricity in B.C., that there wasn’t enough power available. Major housing developments have even been blocked due to limited electricity supply.

These constraints aren’t just technical—they’re already making it harder to build new housing. Canadians may accept higher costs for environmental gains, but pushing up both housing and energy bills risks crossing a line. Banning natural gas makes it harder to build and maintain affordable homes, directly undermining what governments claim to support. In homes forced to switch from gas to electricity, heating and hot water bills could quadruple. Reliability also drops. Builders are now being advised to install backup generators to handle expected power outages—ironically, those generators will often run on the very natural gas being banned.

We can no longer assume the government will keep the lights on. That’s a serious blow to Canadians’ standard of living.

Some argue these trade-offs are justified if they cut emissions. But even that goal is questionable. The gas we don’t burn here will simply be sold elsewhere—likely to countries still relying on coal, oil or even dung. Because emissions don’t respect borders, the global climate impact remains the same, or worse.

Of course, Canada could go further and stop producing natural gas altogether. Leave it all in the ground. But doing so would deliver a major blow to our economy and standard of living: something no elected government is likely to survive. Alternatively, Canada could export more of its low-cost, lower-emission natural gas to displace dirtier fuels abroad. That would reduce global emissions more effectively than restricting gas at home.

Canadians care about the environment. But we need smart, balanced policies—ones that use our resources wisely, not wastefully. We can pursue conservation and cleaner technologies while still recognizing that economic laws apply, even when they’re inconvenient.

It’s not about choosing between prosperity and the planet. It’s about realizing that ignoring the fundamentals—like supply and demand—comes at a cost most Canadians can’t afford.

Dr. Roslyn Kunin is a respected Canadian economist known for her extensive work in economic forecasting, public policy, and labour market analysis. She has held various prominent roles, including serving as the regional director for the federal government’s Department of Employment and Immigration in British Columbia and Yukon and as an adjunct professor at the University of British Columbia. Dr. Kunin is also recognized for her contributions to economic development, particularly in Western Canada.

Troy Media empowers Canadian community news outlets by providing independent, insightful analysis and commentary. Our mission is to support local media in helping Canadians stay informed and engaged by delivering reliable content that strengthens community connections and deepens understanding across the country.

Ottawa’s story never added up. When the Canada Infrastructure Bank pushed through a $1-billion loan to BC Ferries for vessels built at a Chinese state-owned shipyard, federal ministers claimed they were “dismayed” and blindsided. Chrystia Freeland even wrote a letter to the BC government citing national security concerns. In hindsight, she and her staff were engaged in political theatre, performing shock to deflect responsibility onto Premier David Eby.

Documents later showed Freeland’s own ministry of transport had been briefed six weeks before the public rollout. In one internal exchange, her staff admitted officials had received “a confidential heads-up” well in advance. Then came testimony from Housing and Infrastructure Minister Gregor Robertson — also responsible for the Infrastructure Bank — acknowledging the loan was already “inked” in March, before he supposedly raised concerns, a claim as hollow as Freeland’s staged outrage.

The $1-billion Canadian Infrastructure Bank loan to BC Ferries flows directly to China Merchants Industry Weihai — a dual-use shipyard central to Beijing’s military-civil fusion strategy. Critics have long warned that such contracts risk entangling Canadian taxpayers with Chinese state enterprises linked to the People’s Liberation Army.

Those concerns take on new urgency with fresh revelations from Australia. ABC News reported yesterday on a classified U.S. Defense Intelligence Agency assessment showing that China’s commercial ferry fleet is being militarized for amphibious operations against Taiwan. These are not neutral passenger vessels but dual-use platforms modified to carry tanks and PLA troops. The timing of the four-ship build for BC Ferries, the nature of the shipyard, and the class of vessel all suggest that Canada could be indirectly bolstering Beijing’s invasion platform — and, at the very least, injecting Canadian funds into the industrial ecosystem driving the PLA’s buildup.

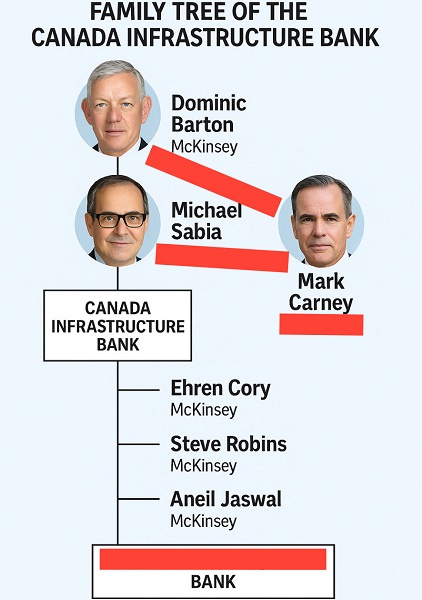

The nature of CIB’s involvement, and Ottawa’s actions that fit the pattern of an emerging cover-up, point to a deeper story that has been bubbling in the capital for nearly a decade: former McKinsey global director and Canadian ambassador to China Dominic Barton, his deep ties to Chinese state-owned and dual-use enterprises, and his founding role in the CIB.

|

Defensive “talking points” prepared for Gregor Robertson’s August 1, 2025 testimony provide a revealing glimpse. The records, obtained through freedom of information by The Bureau, are mostly boilerplate answers. But two pages on the CIB’s structure show clearly what outside reporting has long established: the Bank carries Barton’s DNA, and the imprint of his McKinsey network continues to this day. That raises a plausible theory — that Canada’s pro-Beijing trade lobby, a circle of business leaders revolving around Barton, Sabia, McKinsey, and now Prime Minister Mark Carney, looks like the hidden hand guiding this supposedly arm’s-length deal.

The records that anchor this OpEd show the Infrastructure Bank’s story can be traced like a family tree. At the top is Dominic Barton. In 2016, while serving as McKinsey’s global managing director, he chaired the federal Advisory Council on Economic Growth. That council produced the blueprint for the Canada Infrastructure Bank — and McKinsey itself was paid as a consultant during its creation. Sitting beside Barton on the council was Michael Sabia, who would later become chair of the Bank in 2020 and today serves as chief of staff to Prime Minister Mark Carney.

As the Bank moved from paper to practice, Sabia’s role became pivotal. When he took over as chair, he pulled Barton back into the fold. In June 2020, Barton joined a “strategic refresh” meeting of the CIB. Emails later revealed that McKinsey staff had arranged the session so that “Dom” could “speak freely,” even though he was then serving as Canada’s ambassador to China.

The pattern deepened as new leadership arrived. In November 2020, Ehren Cory was appointed CEO. Cory, too, had worked at McKinsey. Around him, other alumni filled senior posts: Steve Robins, now head of strategy; Aneil Jaswal, director of strategic sectors; even Cory’s executive assistant came directly from McKinsey, according to notes prepared for Gregor Robertson’s August testimony and obtained by The Bureau.

Running alongside this McKinsey chain is a side branch that loops back into the heart of Ottawa. Sabia, Barton’s colleague from the Advisory Council, now serves as Mark Carney’s right hand in the Prime Minister’s Office.

Seen this way, the CIB is not just a Crown corporation with a neutral mandate. It is an institution shaped from the start by Barton’s hand, nurtured by Sabia, and still run day to day by McKinsey-trained managers. The government’s defensive claim — that McKinsey’s influence ended in 2017, as set out in notes for Robertson’s testimony — is impossible to believe. It is as false as Chrystia Freeland’s June 2025 letter to David Eby’s government.

|

The continuity of influence is not just structural — it’s personal. On June 23, 2020, while serving as ambassador to China, Barton joined a CIB “strategic refresh” meeting. He says it was at Sabia’s invitation. But emails tabled in committee show McKinsey staff helped arrange the call and even discussed limiting participants so “Dom” could “speak freely.” Pressed in Parliament during May 2023 testimony, Barton initially failed to disclose the meeting. Only after documents surfaced did he confirm it.

That evasiveness set off a bruising clash. Conservative MP Leslyn Lewis told him flatly: “We have testimony that you gave before, and that was false indeed.” She added: “Mr. Sabia, the former chair of the CIB, testified here on Tuesday that you participated in a McKinsey seminar, led by McKinsey, while you were ambassador — and you have now confirmed this information today.”

Garnett Genuis drove the point home: “Mr. Barton is clearly lying to this committee. We have the emails in black and white. It seems McKinsey was able to infiltrate the government and shape decision making. Your presence and close relationship with the government allowed that to happen.”

Three years earlier, Barton had faced an even higher-profile grilling before the Canada–China Committee — testimony with direct geographical and geopolitical relevance to the CIB’s mysterious $1-billion loan to CMC Weihai.

Back in 2020, Genuis pressed him on McKinsey’s advisory work for Chinese state-owned enterprises, including the China Communications Construction Company — sanctioned by the World Bank for corruption and implicated in Beijing’s militarized islands in the South China Sea. Barton ducked, dissembled, and insisted he was unaware.

“At the time you were in charge of McKinsey, from 2009, it’s my understanding that you advised almost two dozen Chinese state-owned companies. According to The New York Times, one of those companies was the China Communications Construction Company,” Genuis prodded. “When you signed the China Communications Construction Company as a client in 2015, they were still under World Bank sanctions because of the corruption and bid-rigging they engaged in in the Philippines.”

Next, the Conservative MP asked directly: “McKinsey was advising a company that was carrying out the Chinese government’s policy of building militarized islands in the South China Sea. Was it your position that those islands are a violation of international law?”

“What I would say is that I am not familiar at all with our being involved in designing the islands in the South China Sea,” Barton answered. “If you want to talk to someone at McKinsey to find out more information, I’m sure we’d be happy to get someone to talk to you about it.”

McKinsey did not return with information on China’s military action in the South China Sea — the very same theater where Beijing now threatens Taiwan with its civilian ferry buildup plan.

Genuis also asked: “Would you be prepared to submit to this committee a list of all of the Chinese state-owned companies that you did work for at McKinsey?”

“McKinsey’s pretty careful about client confidentialities,” Barton answered. “I’d be happy if there were some mechanism so that it isn’t in the public domain but that some people could look at it. I’m open to that.”

That list was never provided, based on The Bureau’s follow-up in Ottawa. Given the questions surrounding the CIB’s loan to fund CMC Weihai ferries, this lack of transparency takes on a more ominous colour.

The historical record of testimony, going back to the Genuis–Barton stand-off, now casts a long shadow. There is a clear through line to the questioning still to come for Carney’s responsible ministers in the BC Ferries deal — Chrystia Freeland and Gregor Robertson. After revelations that Freeland and her staff staged their supposed shock at the deal with a Chinese military-linked shipbuilder, Freeland has been recalled.

Savvy questioners will likely look beyond her — and above her — in their probing. The CIB, seeded by Barton, staffed by McKinsey alumni, and previously steered by Mark Carney’s chief of staff Michael Sabia, has financed a project that objectively strengthens Beijing’s naval-industrial complex. Who really profits, in conjunction with Beijing? Certainly not Canadian workers, shipbuilders, or citizens, who are left carrying the burden of their government’s deals with China.

This is not just about procurement missteps or potential conflicts of interest. It is the culmination of a decade of weak, negligent thinking on China’s military aggression — stretching from the South China Sea to Canada’s Pacific, Atlantic, and Arctic coasts. Until Canadians confront Barton’s enduring imprint on the CIB, they will continue to discover — too late — that their money is underwriting Beijing’s rise.

The Bureau is a reader-supported publication.

To receive new posts and support my work, consider becoming a free or paid subscriber.

From LifeSiteNews

By Tim Hinchliffe of The Sociable

The WEF is plowing full steam ahead with the globalist agenda to monitor and monetize everything in nature, including the air we breathe, the water we drink, and the very earth we walk upon.

With billionaires Larry Fink and Andre Hoffmann as the new co-chairs, the World Economic Forum (WEF) publishes a 50-page blueprint on how to monetize everything in nature.

The WEF’s latest insight report, “Finance Solutions for Nature: Pathways to Returns and Outcomes,” provides “stakeholders” with dozens of financial solutions for monetizing everything in nature.

Nature pricing, biodiversity crediting schemes, natural asset companies, debt-for-nature swaps, and so much more are all packed into this agenda to overhaul the global financial system with nature-based activities:

The landscape of nature finance is rapidly evolving. From sovereign debt instruments and blended capital platforms to biodiversity credits and emerging asset classes, a growing range of mechanisms is being deployed to fund, finance and de-risk nature-positive action.

The WEF leadership page says that in their work on the board of trustees, “members do not represent any personal or professional interests.”

However, the target audiences for latest WEF insight report are “institutional investors, banks, asset managers, and development actors” – the very business interests that Hoffmann and Fink represent.

WEF interim co-chairs Larry Fink and Andre Hoffmann have everything to gain in their business dealings should the documentation, monetization, and tokenization of everything in nature ever come to full fruition.

And they are well on their way.

Fink’s BlackRock manages over $11 trillion in assets, and last year BlackRock said it was “conducting proprietary research on natural capital investment signals, identifying companies poised for financial advantage in avoiding nature-related risks or leaning into opportunities. Those signals cover themes such as energy management, water management, waste management and biodiversity – and can feed into portfolio construction or support custom exposures.”

Hoffmann is also a key player in a whole host of so-called green financing initiatives, including biodiversity crediting schemes, through his various roles as founder, president, and chairman at several companies and NGOs such as: Innovate 4 Nature – the “accelerator for nature-positive solutions” and Systemiq – the “system change company” established specifically to advance U.N. Agenda 2030.

“The economy depends on natural resources. Their value derives not only from their use as direct inputs to production – such as timber for construction – but also for their benefits to society like living trees that help clean the air. Economists use the term “natural capital” to refer to the total value that natural resources provide to the economy and to people.” — BlackRock, Capital at risk: nature through an investment lens, August 2024

Investigative journalist Whitney Webb: BlackRock and other companies are attempting to seize control over the natural world under the guise of "saving the planet".

"BlackRock being able to unlock and take control of as many natural assets as possible… is obviously a way for… pic.twitter.com/XgRBBqW7qr

— Wide Awake Media (@wideawake_media) February 26, 2025

“Debt-for-nature swaps [DNS] are a financial mechanism that allow countries to restructure bilateral or multilateral debt in exchange for commitments to fund local conservation and restoration. They are also known as ‘debt-for-nature conversion.’” — WEF, Finance Solutions for Nature: Pathways to Returns and Outcomes, September 2025

Is your country millions, billions, or trillions in debt? No problem!

With debt-for-nature swaps, you can restructure your nation’s debt just by letting somebody else come in and take control of your natural resources under the guise of conservation and restoration, but what they’ll really be doing is forcing you to “take out private insurance policies to ‘mitigate the financial impact of natural disasters‘ as well as ‘political risk,’” as investigative journalists Whitney Webb and Mark Goodwin report in Bitcoin Magazine.

Don’t have any money, but want to create value out of thin air, water, soil, or trees? You can set up natural asset companies that can “convert the full economic value of nature into financial flows via equity models.”

Want to help asset managers, bankers, and hedge fund execs get extremely rich while leaving you with only a tiny fraction? Go ahead and get involved in a Payment for Environmental Services (PES) scheme, where financial incentives are provided to individuals or communities in exchange for maintaining or restoring ecosystem services, like carbon sequestration or biodiversity conservation

And if you’re compliant with their rules, you can be rewarded by producing “positive nature and biodiversity outcomes (e.g. species, ecosystems and natural habitats) through the creation and sale of either land or ocean-based biodiversity units over a fixed period” with biodiversity credits, aka “environmental credits.”

Prefer to be left alone and live on the property that you worked hard for all your life? You better be compliant with all the environmental regulations that are coming in the name of preserving biodiversity, so that the $44 trillion of economic value generated by nature doesn’t diminish.

With Larry Fink & Andre Hoffmann having everything to gain, today the WEF published a blueprint for the complete monetization of everything in nature. Natural Asset Companies, Biodiversity Credits, Debt for Nature Swaps, Payments for Ecosystem Services https://t.co/bV1SBKlM41 pic.twitter.com/knqErANBlV

— Tim Hinchliffe (@TimHinchliffe) September 11, 2025

“Environmental credits are verified units of positive environmental outcomes, including biodiversity, water, carbon and nutrient credits. Though developed independently, projects increasingly blend credits via stacking, bundling or stapling.” — WEF, Finance Solutions for Nature: Pathways to Returns and Outcomes, September 2025

“Nature is rapidly emerging as a strategic investment frontier and more institutional capital is flowing into new business models and projects.” — WEF, Finance Solutions for Nature: Pathways to Returns and Outcomes, September 2025

In keeping with the own self-interests of the co-chairs and their business relations, the report highlights “10 priority financial solutions” for these stakeholders to implement:

- Sustainability-linked bonds (SLBs):

- Commercial bonds tying coupon rates to nature-related targets for corporates or governments.

- Thematic (or use-of-proceeds) bonds:

- Bonds with proceeds earmarked for nature projects. Scaling-up requires clearer guidance and aggregation to improve outcomes for issuers and investors.

- Sustainability-linked loans (SLLs):

- Flexible debt, linking interest rates to nature-related targets. SLLs need simpler verification, standardized metrics and stronger triggers to drive nature-positive lending.

- Thematic (or use-of-proceeds) loans:

- Loans for specific nature-related projects. Greater clarity on taxonomies and aggregation is needed to enhance capital flows.

- Impact funds:

- Funds investing in nature-positive outcomes, often accepting higher risk or longer pathways to returns.

- Natural asset companies (NACs):

- Publicly and privately listed companies that convert the full economic value of nature into financial flows via equity models. NACs hold significant potential but need more transactions for price discovery and replicable investment blueprints.

- Environmental credits:

- Tradeable certificates for verified environmental benefits, used in compliance or voluntary markets.

- Debt-for-nature swaps (DNS):

- Mechanisms to restructure sovereign debt in exchange for conservation or restoration commitments, with investable components including bonds and loans.

- Payments for ecosystem services (PES):

- Contracts rewarding conservation for specific ecosystem services, driven by the public sector. Private sector schemes require longer contracts, aggregation and supply chain integration to scale up.

- Internal nature pricing (INP):

- Unexplored, voluntary shadow pricing or fee-based tools to incentivize nature-positive performance in companies or across investment portfolios, similar to internal carbon pricing (ICP).

“While some components of nature – such as food, timber and ecotourism are priced and traded in global markets, the value of many critical ecosystem services remains undervalued….

Carbon sequestration, water filtration, flood protection and pollination are often treated as ‘free’ inputs, despite underpinning our economies and societies.” — WEF, Finance Solutions for Nature: Pathways to Returns and Outcomes, September 2025

“The natural capital approach extends the economic concept of capital to the environment, conceptualizing stocks of natural resources as conventional goods worth restoring, maintaining and enhancing for their productive flows.

This approach includes both accounting – embedding nature in national and corporate balance sheets – and valuation – pricing nature’s contributions into cost-benefit and investment analysis.” — WEF, Finance Solutions for Nature: Pathways to Returns and Outcomes, September 2025

Putting prices on water, air, and soil is a hot topic among globalists at the U.N., the G20, the World Economic Forum (WEF), and the COP meetings.

At the WEF Annual Meeting in Davos this year, Singapore’s President Tharman Shanmugaratnam said that water credits and biodiversity credits should be “stapled” on to carbon credits.

Singapore President Tharman Shanmugaratnam tells the WEF he wants to put a price on everything in nature: "Just like we've got carbon credits, WE NEED TO DEVELOP THE MARKET FOR WATER CREDITS & BIODIVERSITY CREDITS" #wef25 https://t.co/wv04rzht3K pic.twitter.com/UuSiDBSuu3

— Tim Hinchliffe (@TimHinchliffe) January 21, 2025

"Much better that we work on a reliable CARBON CREDIT system with the stapling on of WATER & BIODIVERSITY CREDITS": Singapore President Tharman Shanmugaratnam at the WEF #wef25 https://t.co/wv04rzht3K pic.twitter.com/EhWCvZAsxj

— Tim Hinchliffe (@TimHinchliffe) January 21, 2025

The year prior, at the 2024 WEF Annual Meeting of the New Champions, aka “Summer Davos” meeting in communist China, University of Cambridge Institute for Sustainability Leadership CEO Lindsay Hooper told the panel on “Understanding Nature’s Ledger” that every part of the economy depends on nature, and that in order to protect natural systems, one solution would be to “bring nature onto the balance sheet.”

"We can't do business on a dead planet. If we're going to protect natural systems, one of the solutions is to bring nature onto the balance sheet; bring nature into the ways that decisions are made within business to allocate a value to it" Lindsay Hooper WEF #AMNC Summer Davos pic.twitter.com/Y1dpjMgmS6

— Tim Hinchliffe (@TimHinchliffe) June 27, 2024

In addition to putting “nature on the balance sheet,” another proposal coming at the end of the panel discussion suggested putting a tax on natural systems like water in the same vein as carbon taxes.

"Beyond carbon [taxes] let's think about other aspects of nature that are easier to quantify.. What about water? That's quite possible for us to start integrating systematically into current trading carbon pricing mechanisms" WEF managing director Gim Neo #AMNC24 Summer Davos pic.twitter.com/0rlomVk3ph

— Tim Hinchliffe (@TimHinchliffe) June 27, 2024

With putting prices on nature comes tokenization and derivatives.

At least that’s what former Bank of England adviser Michael Sheren said at COP27 in November 2022.

'Carbon is moving very quickly into a system where it's going to be very close to a currency' …

Next, 'We start thinking about putting prices on water, on trees, on biodiversity … How do we start tokenizing?': Michael Sheren, Former Bank of England Advisor #COP27 pic.twitter.com/r5Nw3b2aeo— Tim Hinchliffe (@TimHinchliffe) November 9, 2022

“Carbon, we already figured out, and carbon is moving very quickly into a system where it’s going to be very close to a currency, basically being able to take a ton of absorbed or sequestered carbon and being able to create a forward-pricing curve, with financial service architecture, documentation,” said Sheren.

And with carbon being close to a currency, “There are going to be derivatives.”

"The biggest challenge is how do we move from a SHAREHOLDER ECONOMY to a STAKEHOLDER ECONOMY" Andre Hoffmann WEF interim co-chair. Agenda 2030 advocate, Club of Rome member, Chatham House Adviser, heir to the 5th largest pharma company in the world, Roche https://t.co/NQlEF36IRy pic.twitter.com/kPI2jtDNxL

— Tim Hinchliffe (@TimHinchliffe) August 20, 2025

Now, under the newfound leadership of Fink and Hoffmann, whose personal business dealings stand everything to gain, the WEF is plowing full steam ahead with the globalist agenda to monitor and monetize everything in nature, including the air we breathe, the water we drink, and the very earth that we walk upon.

Reprinted with permission from The Sociable.

Over $2B California Solar Plant Built To Last, Now Closing Over Inefficiency

Secretive Lockheed Martin Skunk Works reveals latest high-tech military drone

24 years later: Tucker Carlson releases interview with retired CIA agent claiming the CIA KNEW 9/11 was coming

Everything has changed. Again.

-

Business6 hours ago

Over $2B California Solar Plant Built To Last, Now Closing Over Inefficiency

-

Alberta2 days ago

Alberta2 days agoFederal policies continue to block oil pipelines

-

Autism2 days ago

Autism2 days agoAutism – what we know

-

Business5 hours ago

WEF has a plan to overhaul the global financial system by monetizing nature

-

espionage1 day ago

espionage1 day agoCanada Under Siege: Sparking a National Dialogue on Security and Corruption

-

COVID-192 days ago

COVID-192 days agoSecond Massive Population Study Finds COVID-19 “Vaccines” Increase Risk of 6 Major Cancers

-

Business1 day ago

Business1 day agoGoogle Admits Biden White House Pressured Content Removal, Promises to Restore Banned YouTube Accounts

-

Business7 hours ago

Business7 hours agoThe Leaked Conversation at the heart of the federal Gun Buyback Boondoggle