Opinion

The American Experiment Has Gone Down In Flames

From the Daily Caller News Foundation

From the Daily Caller News Foundation

What are we to do about it?

In the late eighteenth century, a group of unusually enlightened men gathered to plot rebellion against the most powerful military power of the day. Their grievances were many, set down in the Declaration of Independence. This storied document was many things, but above all it was a cry of rebellion against tyranny: against the arbitrary, capricious and unwelcome rule of the English over the colonies. It was a cry for liberty.

Against all odds, their rebellion succeeded and, a few years later, they met once again to devise a form of government that would be strong enough to see to those things that only government can do, such as military defense and the enablement of trade between the states. They were, however, leery of the dangers of tyranny, and so they crafted a unique form of government: a federal republic, with power dispersed among the several states, and numerous checks and balances to prevent abuse.

It was a noble experiment, and it served us well for centuries, but it is essential that we understand that this experiment has now failed in its primary purpose: to secure our liberties and to forestall tyrannical rule.

The evidence of this failure is indisputable to anyone with eyes to see. Unelected bureaucrats can impose their will on the citizenry in a way that so far exceeds the arbitrary and capricious rule of the English as to stagger the imagination.

They are imposing upon us regulations to all but outlaw vehicles powered by fossil fuels. They have decreed that a woman can become a man, and a man can become a woman, with utter disregard for biological reality.

They have colluded with the internet oligarchs to censor dissent and to silence their political opponents. They are using the mechanisms of law enforcement to protect their friends and to persecute their enemies.

The intelligence services are spying on Americans, and the FBI looks more and more like the secret police with every passing day. I am afraid of my government; I fear the knock on the door in the middle of the night. The grievances listed in the Declaration of Independence look trifling by comparison.

If the Democrats get their way, it will get even worse. They have made it clear that they intend to undo the system of checks and balances that have kept tyrants at bay for centuries. They will eliminate the Senate filibuster.

They will pack the Supreme Court and turn it into something like the Soviet Politburo, an organ of political power unaccountable to the people with absolute authority over every aspect of life. They will continue to push for non-citizen voting rights, allowing millions of illegal immigrants to vote in key local and state elections.

And, perhaps worst of all, power will be further centralized in Washington under the Democrats, who will willingly crackdown on local and state governments that don’t adopt their left-wing vision. In short, a form of absolute tyranny will be established.

Our constitution was designed to prevent this from happening. It is time for us to recognize that our experiment in self-rule has failed, and that we must do something about it before it is too late.

How did we get here? It all starts with federal money. Money is, and always has been, a profoundly corrupting influence in government. This has been true throughout history, going back to the Romans and even before.

Money is power. Money is control. Money gives you the ability to reward your friends and punish your enemies. Federal money has become a lever used by the bureaucrats to impose their will on state and local government, emasculating the federal system.

The Biden administration is giving away trillions of dollars in public funds to support its allies and to buy votes with the money they’ve taken from us. But no matter how many trillions of dollars they fritter away, it’s never enough, and they are on the verge of spending the country into bankruptcy. The system they have constructed will inevitably collapse, and take us down with it.

What then shall we do? How can we reclaim our lost freedom and save ourselves from the coming tyranny?

To do this, we need to be as bold as our opposition. They have stated that the American system is to be burned to the ground and replaced with something new. I agree, in part. Yes, burn it to the ground — but replace it instead with something old: the Federal Republic the founders intended us to have. This will require a massive — and I mean massive — reduction in the size and the scope of the government, and a return to its stated purpose, as eloquently laid out in the Preamble to the Constitution of the United States:

“We the People of the United States, in Order to form a more perfect Union, establish Justice, insure domestic Tranquility, provide for the common defence, promote the general Welfare, and secure the Blessings of Liberty to ourselves and our Posterity, do ordain and establish this Constitution for the United States of America.”

This, and no more.

Craig W. Stanfill (@craigwstanfill) is a computer scientist, software entrepreneur, and the author of the AI Dystopia science fiction series.

The views and opinions expressed in this commentary are those of the author and do not reflect the official position of the Daily Caller News Foundation.

Racket News

Racket News

By Eric Salzman

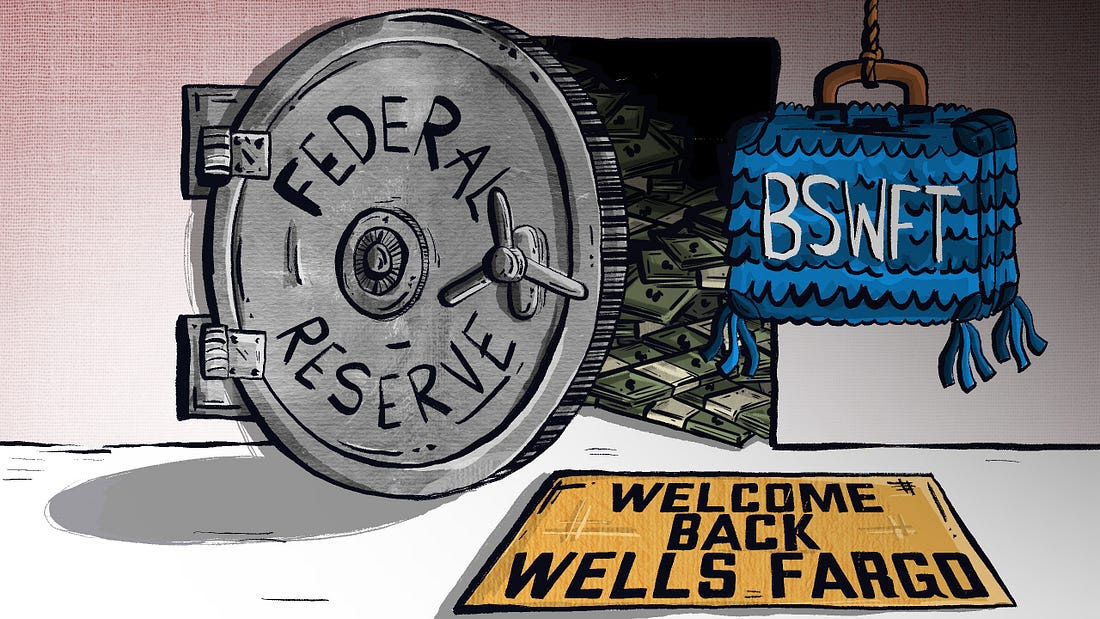

The heavyweight champion of financial crime gets seemingly its millionth chance to show it’s reformed

The past two decades have been tough ones for Wells Fargo and the many victims of its sprawling crime wave. While the banking industry is full of scammers, Wells took turning time honored street-hustles into multi-billion dollar white-collar hustles to a new level.

The Federal Reserve announced last month that Wells Fargo is no longer subject to the asset growth restriction the Fed finally enforced in 2018 after multiple scandals. This was a major enforcement action that prohibited Wells from growing existing loan portfolios, purchasing other bank branches or entering into any new activities that would result in their asset base growing.

Upon hearing the news that Wells was being released from the Fed’s penalty box, my mind turned to this pivotal moment in the classic movie “Slapshot.”

Here are some of Wells Fargo’s lowlights both before and after the Fed’s enforcement action:

- December 2022: Wells Fargo paid more than $2 billion to consumers and $1.7 billion in civil penalties after the Consumer Financial Protection Bureau (CFPB) found mismanagement — including illegal fees and interest charges — in several of its biggest product lines, such as auto loans, mortgages, and deposit accounts.

- September 2021: Wells Fargo paid $72.6 million to the Justice Department for overcharging foreign exchange customers from 2010-2017.

- February 2020: Wells Fargo paid $3 billion to settle criminal and civil investigations by the Justice Department and SEC into its aggressive sales practices between 2002 and 2016. About $500 million was eventually distributed to investors.

- January 2020: The Office of the Comptroller of the Currency (OCC) banned two senior executives, former CEO John Stumpf and ex-Head of Community Bank Carrie Tolstedt, from the banking industry. Stumpf and Tolstedt also incurred civil penalties of $17.5 million and $17 million.

- August 2018: The Justice Department levied a $2.09 billion fine on Wells Fargo for its actions during the subprime mortgage crisis, particularly its mortgage lending practices between 2005 and 2007.

- April 2018: Federal regulators at the CFPB and OCC examined Wells’ auto loan insurance and mortgage lending practices and ordered the bank to pay $1 billion in damages.

- February 2018: The aforementioned Fed enforcement action. In addition to the asset growth restriction, Wells was ordered to replace three directors.

- October 2017: Wells Fargo admitted wrongdoing after 110,000 clients were fined for missing a mortgage payment deadline — delays for which the bank was ultimately deemed at fault.

- July 2017: As many as 570,000 Wells Fargo customers were wrongly charged for auto insurance on car loans after the bank failed to verify whether those customers already had existing insurance. As a result, up to 20,000 customers may have defaulted on car loans.

- September 2016: Wells Fargo acknowledged its employees had created 1.5 million deposit accounts and 565,000 credit card accounts between 2002 and 2016 that “may not have been authorized by consumers,” according to CFPB. As a result, the lender was forced to pay $185 million in damages to the CFPB, OCC, and City and County of Los Angeles.

Additionally, somehow in 2023 Wells even managed to drop $1 billion in a civil settlement with shareholders for overstating their progress in complying with their 2018 agreement with the Fed to clean themselves up!

I imagine if Wells were in any other business, it wouldn’t be allowed to continue. But Wells is part of the “Too Big to Fail” club. Taking away its federal banking charter would be too disruptive for the financial markets, so instead they got what ended up being a seven-year growth ban. Not exactly rough justice.

While not the biggest settlement, my favorite Wells scam was the 2021 settlement of the seven-year pilfering operation, ripping off corporate customers’ foreign exchange transactions.

Like many banks, Wells Fargo offers its corporate clients with global operations foreign exchange (FX) services. For example, if a company is based in the U.S. but has extensive dealings in Canada, it may receive payments in Canadian dollars (CAD) that need to be exchanged for U.S. dollars (USD) and vice versa. Wells, like many banks, has foreign exchange specialists who do these conversions. Ideally, the banks optimize their clients’ revenue and decrease risk, in return for a markup fee, or “spread.”

There’s a lot of trust involved with this activity as the corporate customers generally have little idea where FX is trading minute by minute, nor do they know what time of day the actual orders for FX transactions — commonly called “BSwifts” — come in. For an unscrupulous bank, it’s a license to steal, which is exactly what Wells did.

According to the complaint, Wells regularly marked up transactions at higher spreads than what was agreed upon. This was just one of the variety of naughty schemes Wells used to clobber their customers. My two favorites were “The Big Figure Trick” and the “BSwift Pinata.”

The Big Figure Trick

Let’s say a client needs to sell USD for CAD, and that the $1 USD is worth $1.32 CAD. In banking parlance, the 32 cents is called the “Big Figure.” Wells would buy the CAD at $1.32 for $1 USD and then transpose the actual exchange rate on the customer statement from $1.32 to $1.23. If the customer didn’t notice, Wells would pocket the difference. On a transaction where the client is buying 5 million CAD with USD, the ill-gotten gain for Wells would be about $277,000 USD!

Conversely, if the customer did notice the difference, Wells would just blame it on the grunts in its operational back office, saying they accidentally transposed the number and “correct” the transaction. From the complaint, here is some give and take between two Wells FX specialists:

“You can play the transposition error game if you get called out.” Another FX sales specialist noted to a colleague about a previous transaction that a customer “didn’t flinch at the big fig the other day. Want to take a bit more?”

The BSwift Piñata

The way this hustle would work is, let’s say the Wells corporate customer was receiving payment from one of their Canadian clients. The Canadian client’s bank would send a BSwift message to Wells. The Wells client was in the dark about the U.S. dollar-Canadian dollar exchange rate because it had no idea what time of day the message arrived. Wells took advantage of that by purchasing U.S. dollars for Canadian dollars first. For simplicity, think of the U.S. dollar-Canadian dollar exchange rate as a widget that Wells bought for $1. If the widget increased in value, say to $1.10 during the day, Wells would sell the widget they purchased for $1 to the client for $1.10 and pocket 10 cents. If the price of the widget Wells bought for $1 fell to 95 cents, Wells would just give up their $1 purchase to the client, plus whatever markup they agreed to.

Heads, Wells wins. Tails, client loses.

The complaint notes that a Wells FX specialist wrote that he:

“Bumped spreads up a pinch,” that “these clients who are in the mode of just processing wires will most likely not notice this slight change in pricing” and that it “could have a very quick positive impact on revenue without a lot of risk.”

Talk about a boiler room operation. Personally, I think calling what you are doing to a client a “piñata” should have easily put Wells in the Fed’s penalty box another 5 years at least!

Wells has been released from the Fed’s 2018 enforcement order. I would like to think they have learned their lesson and are reformed, but I would lay good odds against it. A leopard can’t change its spots.

Racket News is a reader-supported publication.

Consider becoming a free or paid subscriber.

International

Woman wins settlement after YMCA banned her for complaining about man in girls’ locker room

From LifeSiteNews

Julie Jaman will receive $65,000 as part of the settlement after being banned from a local swimming pool for objecting to a man in a female shower with little girls present

A Washington State grandmother won a $65,000 settlement from the City of Port Townsend and the Olympic Peninsula YMCA after she was banned from a swimming pool for objecting to a cross-dressing man watching small girls change clothes.

As covered by LifeSiteNews in 2022, Julie Jaman testified before the Port Townsend City Council about her experience showering in the local pool’s facilities when she heard “a man’s voice in the women’s dressing area.” When she investigated, she said that she saw “a man in a women’s swimsuit, watching little girls pull down their bathing suits in order to use the toilets in the dressing room.”

She also told a local newspaper, “There were gaps in the curtain and there I was, naked, with soap and water on me, and this guy, right there very close to me. I asked, ‘Do you have a penis?’ He said, ‘That’s none of your business.’ That’s when I told him, ‘Get out of here, right now.” She appealed to a nearby female manager, who she says replied, “you’re discriminating and you can’t use the pool anymore and I’m calling the police.”

After speaking to police and reviewing police reports, the Port Townsend FreePress reported that Jaman had an “emotional response to a strange male being in the bathroom and helping a young girl take off her bathing suit,” and was described as “screaming” by a complainant.

“In an effort by the city and the YMCA to apply the neo-cultural gender rules at Mountain View Pool dressing, shower room facilities, women and children are being put at risk,” Jaman declared at the time.

A YMCA marketing and communications manager responded at the time by disputing her version of events, claiming the male was not “engaging” with the young girls but was simply escorting them to the dressing room, and that the confrontation was just one in a series of many that led to her ban.

She sued, however, and on June 30 the group representing her, the Center for American Liberty (CAL), announced that the city and the YMCA chapter had agreed to a $65,000 settlement, which also provides that the city will “remove certain information about Ms. Jaman from its website, further underscoring the baselessness of the actions taken against her.”

“This case was never just about one woman being banned from a publicly owned pool, it was about the fundamental right of every American to speak truth without fear of retaliation,” said Mark Trammell, CEO of CAL. “Julie Jaman bravely stood her ground, endured attacks on her character, and today’s settlement affirms that government officials cannot silence dissenting voices through intimidation or retribution.”

“I never imagined that expressing concerns about the safety and privacy of women and girls would lead to me being shunned and banned,” Jaman added. “I’m grateful that justice has been served and that my voice was heard. This is a victory for common sense, women’s rights, and the right to speak the truth.”

Despite being demanded by LGBT activists as a matter of “fairness,” policies forcing girls to share intimate facilities such as bathrooms, showers, or changing areas with males who “identify” as the opposite sex violates their privacy rights, subjects them to needless emotional stress, and gives potential male predators a viable pretext to enter female bathrooms or lockers by simply claiming transgender status.

What Connor Should Say To Oilers: It’s Not You. It’s Me.

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

Federal fiscal anchor gives appearance of prudence, fails to back it up

-

Business2 days ago

Ottawa Funded the China Ferry Deal—Then Pretended to Oppose It

-

COVID-192 days ago

COVID-192 days agoNew Peer-Reviewed Study Affirms COVID Vaccines Reduce Fertility

-

MAiD2 days ago

MAiD2 days agoCanada’s euthanasia regime is not health care, but a death machine for the unwanted

-

Alberta2 days ago

Alberta2 days agoThe permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

-

Business2 days ago

Business2 days agoWorld Economic Forum Aims to Repair Relations with Schwab

-

Alberta2 days ago

Alberta2 days agoAlberta’s government is investing $5 million to help launch the world’s first direct air capture centre at Innisfail

-

Business2 days ago

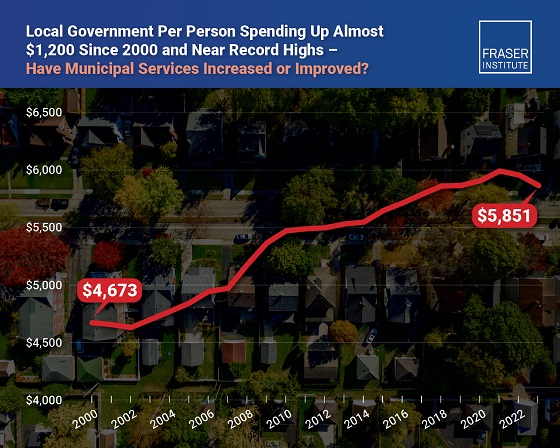

Business2 days agoMunicipal government per-person spending in Canada hit near record levels

-

Business2 days ago

Business2 days agoA new federal bureaucracy will not deliver the affordable housing Canadians need