Economy

Panama Canal drying up woes could have benefited Canadian LNG – If only we had any

From the Frontier Centre for Public Policy

There’s a disturbance in the force of global shipping, as if a major transit point started slipping away.

There’s a very serious problem occurring a few thousand miles to the south of us, one that Canada could have taken tremendous advantage of, if only we had built and completed some liquified natural gas (LNG) terminals by now.

The Panama Canal, one of the wonders of the modern world that utterly changed trade and geopolitics, is drying up.

The canal, which usually handles about 36 ships a day, has in recent days reduced that to 24. By Feb. 1, it is expected to fall to 18. And the largest ships who do transit the canal have to reduce their cargoes, lest they scrape bottom.

That’s because the canal uses fresh water, captured by dams and forming the massive Gatun Lake. That fresh water is collected from ample rains. Every single time a ship passes through the canal, water used to operate the locks is flushed into the ocean. While the greatly expanded third set of locks allows much, much larger ships to use the more than 100 year-old canal, they also use a lot of water despite an innovative water recovery system. And the Canal Authority says they’ve had the lowest rains in 73 years, since 1950.

So when you add up the additional, much larger locks, with a local drought, the canal is rapidly falling into crisis. And the world is starting to take notice.

As they should, since soon half of all ships that usually use the canal will be turned away.

No one depends on the canal more than the Americans. They built it, after all, for a reason. And one of the biggest is it allows for quick access for Gulf Coast ports to Pacific markets. This was a very real reason why building a half dozen large LNG terminals made so much sense (in addition to their proximity to gas production.)

Well, a lot of that just got thrown out the window. Cutting ship transit numbers by half means a dramatic curtailment of the ability of US LNG cargoes to access the Pacific markets. Their alternative is to add something like 8,000 miles going around South America’s Cape Horn, which absolutely no one wants to do due to the treacherous weather and seas.. Otherwise, they have to cross the Atlantic, Mediterranean, Red Sea, Indian Ocean and Straits of Malacca to get to east Asia markets.

The net effect will be some cargoes from the Gulf Coast destined for Asia will have to go much, much further to deliver their product. That means fewer cargoes per ship per year. It’ll tighten up ship availability, and likely put pressure on LNG prices.

And if Canada had moved quicker on building out LNG terminals, particularly on the West Coast, we would be perfectly positioned to cash in on this situation. Not only is Kitimat, Prince Rupert and the like much, much closer to China and Japan, there’s no drying up Panama Canal to contend with, either.

Small wonder, then, Conservative Leader Pierre Poilievre chose on November 10 to post on his various social media channels, “Since Trudeau took office: 18 LNG terminals have been proposed. 0 have been completed.”

To be fair, LNG Canada, the largest proposal, is in the finishing stretch. In July they reported 85 per cent completion. In recent weeks, TC Energy reported the completion of the “golden weld” on the Coastal GasLink pipeline that will supply LNG Canada and presumably other facilities on the West Coast. Without pipeline, which was both massively delayed and overbudget, no small thanks to pipeline protesters, LNG Canada would be useless.

Other projects are finally gaining traction – Woodfibre LNG at Squamish on the south coast, and Ksi Lisims LNG right on the Alaska/BC border, and Cedar LNG, a floating LNG terminal adjacent to LNG Canada and served by Coastal GasLink.

Remember when the German chancellor came to Canada, seeking LNG, and was told by Prime Minister Justin Trudeau there was “no business case?” And then the Japanese prime minister was told something similar a few weeks later?

The Ukraine War has proven a business case for almost two years in the Atlantic basin. The Panama Canal reduction in service will soon prove it in the Pacific. What more do we need?

Canada should have built these projects years ago. We’d be securing markets and cashing in today.

No business case, indeed.

Brian Zinchuk is editor and owner of PipelineOnline.ca, and occasional contributor to the Frontier Centre for Public Policy. He can be reached at [email protected].

![]()

From the Daily Caller News Foundation

During the latest marathon cabinet meeting on Dec. 2, Energy Secretary Chris Wright made news when he told President Donald Trump that “The biggest determinant of the price of energy is politicians, political leaders, and polices — that’s what drives energy prices.”

He’s right about that, and it is why the back-and-forth struggle over federal energy and climate policy plays such a key role in America’s economy and society. Just 10 months into this second Trump presidency, the administration’s policies are already having a profound impact, both at home and abroad.

While the rapid expansion of AI datacenters over the past year is currently being blamed by many for driving up electric costs, power bills were skyrocketing long before that big tech boom began, driven in large part by the policies of the Obama and Biden administration designed to regulate and subsidize an energy transition into reality. As I’ve pointed out here in the past, driving up the costs of all forms of energy to encourage conservation is a central objective of the climate alarm-driven transition, and that part of the green agenda has been highly effective.

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

Please consider making a small donation of any amount here.

Thank you!

President Trump, Wright, and other key appointees like Interior Secretary Doug Burgum and EPA Administrator Lee Zeldin have moved aggressively throughout 2025 to repeal much of that onerous regulatory agenda. The GOP congressional majorities succeeded in phasing out Biden’s costly green energy subsidies as part of the One Big Beautiful Bill Act, which Trump signed into law on July 4. As the federal regulatory structure eases and subsidy costs diminish, it is reasonable to expect a gradual easing of electricity and other energy prices.

This year’s fading out of public fear over climate change and its attendant fright narrative spells bad news for the climate alarm movement. The resulting cracks in the green facade have manifested rapidly in recent weeks.

Climate-focused conflict groups that rely on public fears to drive donations have fallen on hard times. According to a report in the New York Times, the Sierra Club has lost 60 percent of the membership it reported in 2019 and the group’s management team has fallen into infighting over elements of the group’s agenda. Greenpeace is struggling just to stay afloat after losing a huge court judgment for defaming pipeline company Energy Transfer during its efforts to stop the building of the Dakota Access Pipeline.

350.org, an advocacy group founded by Bill McKibben, shut down its U.S. operations in November amid funding woes that had forced planned 25 percent budget cuts for 2025 and 2026. Employees at EDF voted to form their own union after the group went through several rounds of budget cuts and layoffs in recent months.

The fading of climate fears in turn caused the ESG management and investing fad to also fall out of favor, leading to a flood of companies backtracking on green investments and climate commitments. The Net Zero Banking Alliance disbanded after most of America’s big banks – Goldman Sachs, J.P. Morgan Chase, Citigroup, Wells Fargo and others – chose to drop out of its membership.

The EV industry is also struggling. As the Trump White House moves to repeal Biden-era auto mileage requirements, Ford Motor Company is preparing to shut down production of its vaunted F-150 Lightning electric pickup, and Stellantis cancelled plans to roll out a full-size EV truck of its own. Overall EV sales in the U.S. collapsed in October and November following the repeal of the $7,500 per car IRA subsidy effective Sept 30.

The administration’s policy actions have already ended any new leasing for costly and unneeded offshore wind projects in federal waters and have forced the suspension or abandonment of several projects that were already moving ahead. Capital has continued to flow into the solar industry, but even that industry’s ability to expand seems likely to fade once the federal subsidies are fully repealed at the end of 2027.

Truly, public policy matters where energy is concerned. It drives corporate strategies, capital investments, resource development and movement, and ultimately influences the cost of energy in all its forms and products. The speed at which Trump and his key appointees have driven this principle home since Jan. 20 has been truly stunning.

David Blackmon is an energy writer and consultant based in Texas. He spent 40 years in the oil and gas business, where he specialized in public policy and communications.

““He knows nothing; and he thinks he knows everything. That points clearly to a political career.” George Bernard Shaw

In the days immediately following Donald Trump’s rude intervention into the 2025 Canadian federal election— suggesting Canada might best choose American statehood— two schools of thought emerged.

The first and most impactful school in the short term was the fainting-goat response of Canadian’s elites. Sensing an opening in which to erode Pierre Poilievre’s massive lead in the 2024 polls over Justin Trudeau, the Laurentian elite concocted Elbows Up, a self-pity response long on hurt feelings and short on addressing the issues Trump had cited in his trashing of the Canadian nation state.

In short order they fired Trudeau into oblivion, imported career banker Mark Carney as their new leader in a sham convention and convinced Canada’s Boomers that Trump had the tanks ready to go into Saskatchewan at a moment’s notice. The Elbows Up meme— citing Gordie Howe— clinched the group pout.

(In fact, Trump has said that America is the world’s greatest market, and if those who’ve used it for free in the past [Canada] want to keep special access they need to pay tariffs to the U.S. or drop protectionist charges on dairy and more against the U.S.)

The ruse worked out better than they could have ever imagined with Trump even saying he preferred to negotiate with Carney over Poilievre. In short order the Tories were shoved aside, the NDP kneecapped and the pet media anointed Carney the genius skewing Canada away from its largest trade partner to the Eurosphere. We remain in that bubble, although the fulsome promises of Carney’s first days are now coming due.

Which brings us to the second reaction. That was Alberta premier Danielle Smith bolting to Mar A Lago in the days following Trump’s comments. Her goal was to put pride aside and accept that a new world order was in play for Canada. She met with U.S. officials and, briefly, with Trump to remind them that Canada’s energy industry was integral to American prosperity and Canadian stability.

Needless to say, the fainting goats pitched a fit that not everyone was clutching pearls and rending garments in the wake of Trump’s dismissive assessment of his northern neighbours. Their solution to Trump was to join China in retaliatory tariffs— the only two nations to do so— and to boycott American products and travel. Like the ascetic monks they cut themselves off from real life. Trump has yet to get back to Carney the Magnificent

And Smith? She was a “traitor” or a “subversive” who should be keel hauled in the North Saskatchewan. For much of the intervening months she has been attacked at home in Alberta by the N-Deeps and in Ottawa by just about everyone on CBC, CTV, Global and the Globe & Mail. “How could she meet with the Cheeto?”

Nonetheless conservatives in the province moved toward a more independence within Canada. Smith articulated her demands for Alberta to prevent a referendum on whether to remain within Confederation. At the top of her list were pipelines and access to tidewater. Ergo, a no-go for BC’s squish premier David Eby who is the process of handing over his province to First Nations.

It became obvious that for all of Carney’s alleged diplomacy in Europe and Asia (is the man ever home?) he had a brewing disaster in the West with Alberta and Saskatchewan growing restless. In a striking move against the status quo, Nutrien announced it would ship its potash to tidewater via the U.S., thereby bypassing Vancouver’s strike-prone, outdated port and denying them billions.

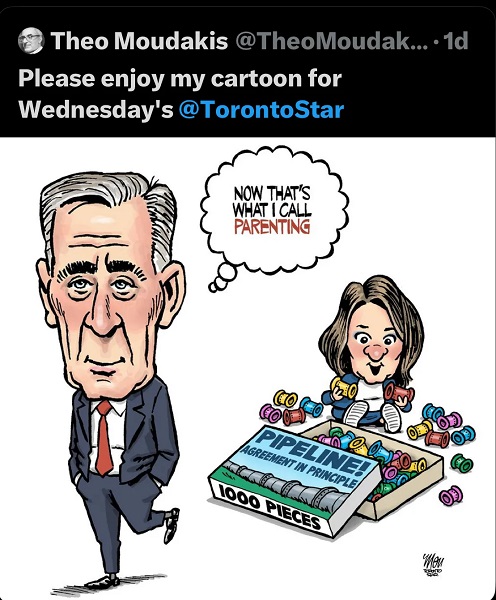

Suddenly, Smith’s business approach began making eminent good sense if the goal is to keep Canada as one. So we saw last week’s “memorandum of understanding” between Alberta and Ottawa trading off carbon capture and carbon taxes for potential pipelines to tidewater on the B.C. coast. A little bit of something for everyone and a surrender on other things.

The most amazing feature of the Mark Carney/Danielle Smith MOU is that both politicians probably need the deal to fail. Carney can tell fossil-fuel enemy Quebec that he tried to reason with Smith, and Smith can say she tried to meet the federalists halfway. Failure suits their larger purposes. Which is for Carney to fold Canada into Euro climate insanity and Smith into a strong leverage against the pro-Canada petitioners in her province.

Soon enough, at the AFN Special Chiefs Assembly, FN Chief Cindy Woodhouse Nepinak told Carney that “Turtle Island” (the FN term for North America popularized by white hippy poet Gary Snyder) belongs to the FN people “from coast to coast to coast.” The pusillanimous Eby quickly piped up about tanker bans and the sanctity of B.C. waters etc.

Others pointed out the massive flaw in a plan to attract private interests to build a vital bitumen pipeline if the tankers it fills are not allowed to sail through the Dixon Entrance to get to Asia.

But then Eby got Nutrien’s message that his power-sharing with the indigenous might cause other provinces to bypass B.C. (imagine California telling Texas it can’t ship through its ports over moral objections to a product). He’s now saying he’s open to pipelines but not to lift the tanker ban along the coast. Whatever.

Meanwhile the kookaburras of isolation back east continue with virtue signalling on American booze— N.S. to sell off its remains stocks — while dreaming that Trump’s departure will lead to the good-old days of reliance on America’s generosity.

But Smith looks to be wining the race. B.C.’s population shrank 0.04 percent in the second quarter of 2025, the only jurisdiction in Canada to do so. Meanwhile, Alberta is heading toward five million people, with interprovincial migrants making up 21 percent of its growth.

But what did you expect from the Carney/ Eby Tantrum Tandem? They keep selling fear in place of GDP. As GBS observed, “You have learnt something. That always feels at first as if you have lost something.”

Bruce Dowbiggin @dowbboy is the editor of Not The Public Broadcaster A two-time winner of the Gemini Award as Canada’s top television sports broadcaster, his new book Deal With It: The Trades That Stunned The NHL And Changed hockey is now available on Amazon. Inexact Science: The Six Most Compelling Draft Years In NHL History, his previous book with his son Evan, was voted the seventh-best professional hockey book of all time by bookauthority.org . His 2004 book Money Players was voted sixth best on the same list, and is available via brucedowbigginbooks.ca.

Is there a cure for Alzheimer’s Disease?

Learning the Truth about “Children’s Graves” and Residential Schools is More Important than Ever

The Unmasking of Vaccine Science

Media bound to pay the price for selling their freedom to (selectively) offend

-

MAiD2 days ago

MAiD2 days agoFrom Exception to Routine. Why Canada’s State-Assisted Suicide Regime Demands a Human-Rights Review

-

Business2 days ago

Business2 days agoCarney government should privatize airports—then open airline industry to competition

-

Alberta2 days ago

Alberta2 days agoCarney’s pipeline deal hits a wall in B.C.

-

Alberta2 days ago

Alberta2 days agoAlberta Sports Hall of Fame Announces Class of 2026 Inductees

-

Censorship Industrial Complex1 day ago

Censorship Industrial Complex1 day agoConservative MP Leslyn Lewis slams Liberal plan targeting religious exemption in hate speech bil

-

Business2 days ago

Business2 days agoWhat’s Going On With Global Affairs Canada and Their $392 Million Spending Trip to Brazil?

-

Business2 days ago

Business2 days agoIs Carney Falling Into The Same Fiscal Traps As Trudeau?

-

Energy2 days ago

Energy2 days agoCanada following Europe’s stumble by ignoring energy reality