Business

US firms like BlackRock are dropping their climate obsession while Europe ramps theirs up

Larry Fink on stage at the 2022 New York Times DealBook on November 30, 2022. in New York CityPhoto by Thos Robinson/Getty Images for The New York Times

From LifeSiteNews

By David James

As U.S. firms such as BlackRock and JPMorgan Chase continue to distance themselves from the ESG and ‘climate change’ agendas, Europe has been moving aggressively in the opposite direction, suggesting a rift is forming on the global economic landscape.

The climate change debate is usually thought to be focused on scientific analyses of the earth’s atmosphere. But that is only what is on the surface. It is also very much about money and politics and there has been a big shift that looks likely to threaten support for the net zero initiative. It may lead to a deep economic and political rift between the U.S. and Europe.

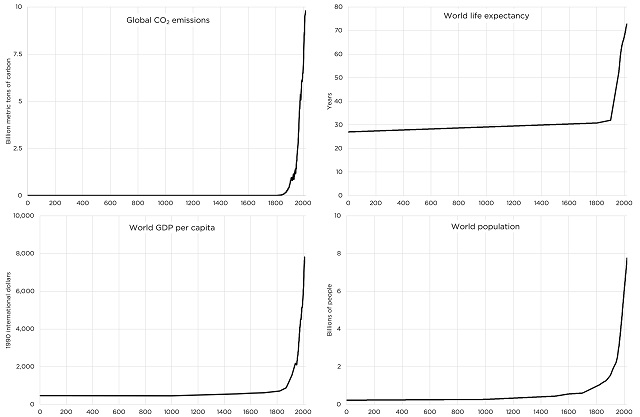

Estimates of the cost of decarbonizing the economy by 2050 have varied, but it is generally agreed that it is a financial bonanza. Goldman Sachs is at the low end with a modest $80 trillion while Bank of America estimates an extraordinary $275 trillion, about 10 times the current value of the U.S. stock market.

The finance sector, dizzy with the prospect of a huge investment opportunity, imposed a metric on corporations called Environmental, Social and Governance (ESG), a mechanism for demanding that companies go down the net zero route – and also comply with diversity equity and inclusion (DEI) requirements, the “S” part of ESG. Corporations that did not cooperate were threatened with a loss of support in the market and lower relative share prices.

That trend is starting to reverse. BlackRock, JPMorgan Chase, and State Street recently exited from Climate Action 100+, a coalition of the world’s largest institutional investors that pledges to “ensure the world’s largest corporate greenhouse gas emitters take necessary action on climate change.” The passive fund Vanguard, the world’s second largest, exited over a year ago.

These four fund managers oversee assets of about $25 trillion, which is approximately a quarter of the entire funds under management in the world.

They are changing direction for two reasons. First, there was an implicit bargain with ESG, whereby compliant companies would not only get to save the environment but also get to see their share prices outperform non-compliant companies. It is not turning out that way. In fact, better returns have come from investing against ESG-compliant companies.

More compellingly, 16 conservative state attorneys general in the U.S. have demanded answers from BlackRock’s directors regarding the Climate Action and ESG initiatives. Other fund managers and banks have also attracted unwanted scrutiny.

Nothing concentrates the mind of fund managers more than the prospect of clients withdrawing their funds – in this case state government pension money. Larry Fink, chief executive of BlackRock, is now saying he does not think it is helpful to use the term ESG, having been one of the most aggressive advocates. In his 2022 letter to CEOs he was issuing veiled threats to companies not complying with ESG. In 2024, he omitted the term entirely.

Meanwhile in Europe, very different choices are being made. The European Union (EU) is looking to impose sustainability reporting standards on all medium and large businesses. The intention is to have European companies set up a new accounting system by the end of the decade. Rather than recording financial transactions, it will instead aggregate data related to climate, pollution, especially carbon dioxide emissions, biodiversity and social issues.

As one (anonymous) analyst writes: “It is a very detailed control system for European companies where the European Commission can, in the future, dictate anything it wants – and punish for any violations any way it wants. Apart from the crazy regulatory load, this initiative can only be seen as a direct seizure of operational control of European companies, and thereby the European economy.”

So, while the U.S. looks to restore an unsteady version of capitalism, Europe is heading towards some kind of climate-driven socialism.

The EU plan seems to be to eventually direct their banks’ lending, which would radically undermine the region’s free-market system and establish something more like communist-style centralized control.

This does not mean U.S. governments and bureaucrats will stop pushing their climate agenda. A court case brought by the city of Honolulu, for example, is one of several attempts to bankrupt the American energy industry. But when the big institutional money changes direction then corporations and governments eventually follow.

The situation is further complicated by the emergence of the expanded BRICS alliance, which will soon represent a bigger proportion of the world economy than the G7. Saudi Arabia, Iran, United Arab Emirates, Ethiopia and Egypt will be added to the original group of Brazil, Russia, India, China and South Africa.

The BRICS nations will not allow the West’s climate change agenda to reshape their polities. Most of them are either sellers or heavy consumers of fossil fuels. Both India and China are increasing their use of coal, for instance, which makes Western attempts to reduce emissions largely pointless.

The promise that hundreds of trillions of investment opportunities would come from converting to net zero was always just a financial projection, mere speculation. The scale of transiting to a decarbonized economy would be so enormous it would inevitably become a logistical nightmare, if not an impossibility.

Energy expenditure represents about an eighth of the world’s GDP. Oil, natural gas and coal still provide 84 percent of the world’s energy, down just two per cent from 20 years ago. Production of renewable energy has increased but so has overall consumption. Oil powers 97 percent of all transportation.

Relying solely on renewable energy was never realistic and now that the financial dynamic is changing the prospects of achieving net zero have become even more remote. As the finance website ZeroHedge opines: “Both the DEI and ESG gravy trains on Wall Street are finally coming to an unceremonious end.” Financial markets continually get seduced by fads; the ESG agenda is starting to look like yet another example.

From LifeSiteNews

Canadians’ disinterest in electric vehicles comes as the Trudeau government recently mandated that all new light-duty vehicles in Canada are zero emission by 2035.

Research has revealed that Canadians are increasingly unwilling to purchase an electric vehicle (EV).

According to an April 22 survey from AutoTrader, Canadians remain skeptical of Prime Minister Justin Trudeau’s electric vehicle mandate and ongoing advertisement surrounding electric vehicles, as interest in owning one dropped for a second year in a row.

“Overall, while almost half of non-EV owners are open to buying an EV for their next vehicle, interest in EVs has declined for the second year in a row,” reported Tiffany Ding, director of insights and intelligence at AutoTrader.

In 2022, at least 68 percent of Canadians were interested in buying an electric vehicle. However, by 2023, the number declined to 56 percent. So far in 2024, there is even less interest, with only 46 percent saying they were open to purchasing one.

“AutoTrader data shows a direct correlation to gas prices and EV interest, and since gas prices have normalized from their peak in 2022, EV interest has also dropped,” a summary of the survey explained.

However, Canadians did show a slight increase of interest in hybrid vehicles, with 62 percent of those looking to purchase an electric vehicle saying they would look at a gas-electric hybrid, compared with 60 percent in 2023.

The survey also questioned Canadians regarding Trudeau’s Zero Emission Vehicle (ZEV) mandate, which requires all new light-duty vehicles in Canada are zero-emission by 2035, essentially banning the sale of new gasoline/diesel-only powered cars.

The mandate comes despite warnings that it would cause massive chaos by threatening to collapse the nation’s power grids.

“Over 75 percent of respondents are aware of the federal government’s ZEV mandate, which requires all new light-duty vehicles sold in Canada to be zero-emission by 2035,” the survey found.

However, the respondents revealed that they believe it’s “unlikely that Canada will be able to meet the federal government’s ZEV target due to the current inadequate charging infrastructure or a change in political power that could revoke or amend the ZEV mandate timeline.”

Canadians’ concerns in buying an electric vehicle include limited travel range/distance, inadequate availability of charging stations, higher purchasing costs, and concerns that they do not perform well in cold weather.

Indeed, this winter, western Canadians experienced firsthand the unreliability of Trudeau’s “renewable” energy scheme as Alberta’s power grid nearly collapsed due to a failure of wind and solar power.

Trudeau’s plan has been roundly condemned by Canadians, including Alberta Premier Danielle Smith. In 2022, Smith denounced a federal mandate that will require all new cars sold after 2035 to be “zero emission” electric (EVs) vehicles and promised that Albertans will always have the choice to buy gasoline-powered cars.

Since taking office in 2015, Trudeau has continued to push a radical environmental agenda similar to the agendas being pushed the World Economic Forum’s “Great Reset” and the United Nations’ “Sustainable Development Goals.”

The reduction and eventual elimination of the use of so-called “fossil fuels” and a transition to unreliable “green” energy has also been pushed by the World Economic Forum (WEF) – the globalist group behind the socialist “Great Reset” agenda – an organization in which Trudeau and some of his cabinet are involved.

The Trudeau government’s electric vehicle plan comes despite the fact Canada has the third largest oil reserves in the world. Electric cars cost thousands more to make and buy, are largely considered unsuitable for Canada’s climate as they offer poor range and long charging times during cold winters and have batteries that take tremendous resources to make and are difficult to recycle.

From the Fraser Institute

By Tegan Hill and Jake Fuss

From 2014 to 2022, inflation-adjusted total business investment (in plants, machinery, equipment and new technologies but excluding residential construction) in Canada declined by C$34 billion. During the same period, after adjusting for inflation, business investment declined by a total of $3,748 per worker

According to the recent federal budget, the Trudeau government plans to increase the inclusion rate from 50 per cent to 66.7 per cent on capital gains over $250,000 for individuals and on all capital gains realized by corporations and trusts. Unfortunately, this tax hike will be the final nail in the coffin for business investment in Canada, which likely means even harder economic times ahead.

Canada already faces a business investment crisis. From 2014 to 2022, inflation-adjusted total business investment (in plants, machinery, equipment and new technologies but excluding residential construction) in Canada declined by C$34 billion. During the same period, after adjusting for inflation, business investment declined by a total of $3,748 per worker—from $20,264 per worker in 2014 to $16,515 per worker in 2022.

While business investment has declined in Canada since 2014, in other countries, including the United States, it’s continued to grow. This isn’t a post-COVID problem—this is a Canada problem.

And Canadians should be worried. Businesses investment is key for strong economic growth and higher living standards because when businesses invest in physical and intellectual capital they equip workers with the tools and technology (e.g. machinery, computer programs, artificial intelligence) to produce more and provide higher quality goods and services, which fuels innovation and higher productivity. And as firms become more efficient and increase profits, they’re able to pay higher wages, which is why business investment remains a key factor for higher incomes and living standards.

The Trudeau government’s policies—increased regulation, particularly in the energy and mining sectors (which makes Canada a relatively unattractive place to do business), higher and uncompetitive taxes, and massive federal deficits (which imply future tax increases)—have damaged business investment.

Unsurprisingly, weak business investment has correlated with a weak economy. In the fourth quarter of 2023, real economic growth per person ($58,111) officially fell below 2014 levels ($58,162). In other words, Canadian living standards have completely stagnated. In fact, over the last decade economic growth per person has been the weakest on record since the 1930s.

Instead of helping fix the problem, the Trudeau government’s capital gains tax hike will further damage Canada’s economy by reducing the return on investment and encouraging an exodus of capital from the country. Indeed, capital gains taxes are among the most economically-damaging forms of taxation because they reduce the incentive to invest.

Once again, the Trudeau government has enacted a policy that will deter business investment, which Canada desperately needs for strong economic growth. The key takeaway for Canadians? Barring a change in policy, you can expect harder times ahead.

Authors:

A Wealth-Creating Way of Reducing Global CO2 Emissions

Reflections on Earth Day

Col. Douglas Macgregor torches Trump over support for bill funding wars in Ukraine and Israel

Trudeau’s 2024 budget could drive out investment as housing bubble continues

Alberta government should create flat 8% personal and business income tax rate in Alberta

Alberta’s baby name superstar steals the show again

Low and middle income Canadians hit hardest by high marginal effective tax rates

-

Automotive2 days ago

Automotive2 days agoThe EV ‘Bloodbath’ Arrives Early

-

Brownstone Institute1 day ago

Brownstone Institute1 day agoThe Numbers Favour Our Side

-

Frontier Centre for Public Policy1 day ago

Frontier Centre for Public Policy1 day agoHow much do today’s immigrants help Canada?

-

Fraser Institute10 hours ago

Fraser Institute10 hours agoFederal government’s fiscal record—one for the history books

-

Alberta10 hours ago

Alberta10 hours agoPrincipal at Calgary Elementary School charged with possession of child pornography

-

Bruce Dowbiggin10 hours ago

Bruce Dowbiggin10 hours agoIn Toronto The Leafs Always Fall In Spring: 2024 Edition

-

Alberta9 hours ago

Alberta9 hours agoRed Deer Company fined $360,000.00 after 2022 workplace fatality

-

Alberta5 hours ago

Alberta5 hours agoAlberta threatens to fight Trudeau government restrictions on Canada’s plastics industry