CBDC Central Bank Digital Currency

Senator Ted Cruz introduces bill to ban CBDCs to prevent US from becoming ‘surveillance state’

From LifeSiteNews

Heritage Action for America warned that ‘anti-CBDC legislation is necessary to safeguard Americans’ financial privacy in the face of potential surveillance, control, and political intimidation.’

U.S. Sen. Ted Cruz introduced the CBDC Anti-Surveillance State Act to prohibit the Federal Reserve from issuing a central bank digital currency (CBDC) that Republican sponsors of the bill believe could turn the nation into a “surveillance state” by handing over control of personal finances to federal government agencies.

While digital currency offers some attractive features, it also would grant the federal government unlimited opportunity to weaponize the technology against citizens, allowing it to both spy on the spending habits of everyday Americans and block access to the money in their personal bank accounts.

U.S. House Majority Whip Tom Emmer of Minnesota described the threat of a U.S. CBDC last fall:

Unlike decentralized cryptocurrencies, like Bitcoin, a CBDC is a digital form of sovereign currency that is designed and issued by a government and transacts on a digital ledger that is controlled by that government. In short, a CBDC is government-controlled programmable money that, if not designed to emulate cash, could give the federal government the ability to surveil Americans’ transactions and choke out politically unpopular activity.

A government-issued CBDC is nothing more than a CCP-style surveillance tool that would be used to undermine the American way of life.

“While Americans across the country are being punished for thinking, speaking, and voting the ‘wrong’ way, the last thing we need is the government surveilling personal finances,” explained a statement from Heritage Action for America concerning the new legislation. “Anti-CBDC legislation is necessary to safeguard Americans’ financial privacy in the face of potential surveillance, control, and political intimidation.”

“CBDCs present major privacy concerns for everyday Americans, including granting the government the ability to collect intimate personal details on U.S. citizens, and potentially track and freeze funds for any reason,” the Blockchain Association noted.

Sen. Cruz, chief sponsor of the bill, said, “The Biden administration salivates at the thought of infringing on our freedom and intruding on the privacy of citizens to surveil their personal spending habits, which is why Congress must clarify that the Federal Reserve has no authority to implement a CBDC.”

“Big government has no business spying on Americans to control their personal finances and track their transactions,” said Republican U.S. Sen. Rick Scott of Florida, a co-sponsor of the bill. “It is a massive overreach.”

In early 2022, the Biden administration urged the Fed to investigate the creation of a CBDC.

“Over 100 countries are exploring or piloting Central Bank Digital Currencies (CBDCs),” said Biden, warning that the U.S. “must play a leading role in international engagement and global governance of digital assets consistent with democratic values and U.S. global competitiveness.”

But many Republicans see this as nothing more than a means to turn America into a totalitarian state.

Pushback against a U.S. CBDC has become an integral part of the messaging of 2024’s presidential hopefuls.

Last month, former President Donald Trump pledged to ban a CBDC if re-elected to the White House.

“As your president, I will never allow the creation of a Central Bank Digital Currency,” Trump told a crowd during a campaign event in New Hampshire.

“Such a currency would give a federal government — our federal government — absolute control over your money,” Trump said. “They could take your money, and you wouldn’t even know it was gone.”

“This would be a dangerous threat to freedom, and I will stop it from coming to America,” he vowed.

Even Robert F. Kennedy Jr., a former Democrat now running as an Independent presidential candidate, has warned that CBCDs are “a calamity for human rights and for civil rights” while similarly promising to halt progress by the Fed from creating a CBDC.

Eleven countries have already fully implemented CBDCs, including China, where digital currency is tied to a person’s “social credit score.”

The CCP (Chinese Communist Party) uses its extensive network of digital cameras —estimated to be over one billion — combined with facial-recognition capabilities to monitor the daily movements and actions of its citizens. That along with other information collecting capabilities used in conjunction with government-controlled digital currency allows the CCP to punish those who transgress desired social norms.

While Democrats in Congress have sought to pass legislation authorizing the Fed to institute a CBDC, Republicans have similarly made sought to preempt such a move.

Last fall, Emmer introduced a bill in the U.S. House with the same name as Cruz’s bill, “CBDC Anti-Surveillance State Act,” to” halt the efforts of unelected bureaucrats in Washington, D.C. from issuing a central bank digital currency (CBDC) that dismantles Americans’ right to financial privacy.”

Co-sponsoring the bill with Cruz are Republican Sens. Bill Hagerty of Tennessee, Scott, Ted Budd of North Carolina, and Mike Braun of Indiana.

From LifeSiteNews

A new report released by the Bank of Canada proposed a ‘promising architecture well-suited for basic payments’ through the use of a digital dollar, though most Canadians are wary of such an idea.

Canada’s central bank has been studying ways to introduce a central bank digital currency (CBDC) for use for online retailers, according to a new report, despite the fact that recent research suggests Canadians are wary of any type of digital dollar.

In a new 47-page report titled, “A Retail CBDC Design For Basic Payments Feasibility Study,” which was released on June 13, 2025, the Bank of Canada (BOC) identified a “promising architecture well-suited for basic payments” through the use of a digital dollar.

The report reads that CBDCs “can be fast and cheap for basic payments, with high privacy, although some areas such as integration with retail payments systems, performance of auditing and resilience of the core system state require further investigation.”

While the report authors stopped short of fully recommending a CBDC, they noted it is a decision that could happen “outside the scope of this analysis.”

“Our framing highlights other promising architectures for an online retail CBDC, whose analysis we leave as an area for further exploration,” reads the report.

When it comes to a digital Canadian dollar, the Bank of Canada last year found that Canadians are very wary of a government-backed digital currency, concluding that a “significant number” of citizens would resist the implementation of such a system.

Indeed, a 2023 study found that most Canadians, about 85 percent, do not want a digital dollar, as previously reported by LifeSiteNews.

The study found that a “significant number” of Canadians are suspicious of government overreach and would resist any measures by the government or central bank to create digital forms of official money.

The BOC has said that it would continue to look at other countries’ use and development of CBDCs and will work with other “central banks” to improve so-called cross border payments.

Last year, as reported by LifeSiteNews, the BOC has already said that plans to create a digital “dollar,” also known as a central bank digital currency (CBDC), have been shelved.

Digital currencies have been touted as the future by some government officials, but, as LifeSiteNews has reported before, many experts warn that such technology would restrict freedom and could be used as a “control tool” against citizens, similar to China’s pervasive social credit system.

The BOC last August admitted that the creation of a CBDC is not even necessary, as many people rely on cash to pay for things. The bank concluded that the introduction of a digital currency would only be feasible if consumers demanded its release.

Conservative Party leader Pierre Poilievre has promised, should he ever form the government, he would oppose the creation of a digital dollar.

Contrast this to Canada’s current Liberal Prime Minister Mark Carney. He has a history of supporting central bank digital currencies and in 2022 supported “choking off the money” donated to the Freedom Convoy protests against COVID mandates.

From LifeSiteNews

By

“central bank digital currency could hand incredible power to the Government and Bank of Canada to monitor financial transactions, punish whatever behaviours the government deems undesirable, and penalize those on the wrong side of government ambitions”

The Justice Centre for Constitutional Freedoms released a new report examining how the adoption of a central bank digital currency in Canada could undermine the rights and freedoms of Canadians, including their privacy, autonomy, security, equality, and access to economic participation.

Financial transactions are increasingly conducted digitally. In 2023, a mere 11 percent of transactions were conducted with cash, according to Payments Canada.

This trend is not limited to individual consumers. Government entities, including government departments, agencies, and Crown Corporations, have rapidly digitized access to, and delivery of, their goods and services over the past decade.

READ: Mark Carney has history of supporting CBDCs, endorsed Freedom Convoy crackdown

Against this backdrop, in 2017, the Bank of Canada (a Crown Corporation) began exploring the possibility of implementing its own government-issued and government-controlled cashless currency – a central bank digital currency (CBDC).

In a 2023 Bank of Canada survey on CBDCs, however, 82 percent of 89,423 respondents strongly disagreed that the Bank of Canada should be researching or building the capability to issue a CBDC. Despite these results, the Bank of Canada continues to research a CBDC for Canada.

The Justice Centre’s report critically evaluates the impact a CBDC could have on Canadians’ fundamental rights and freedoms. Absent robust legislative protections and oversight, a CBDC could allow the Government and Bank of Canada to monitor Canadians’ purchases, donations, investments and other financial transactions.

A CBDC has the potential to empower government to reward and punish the behaviours and lifestyle choices of individual Canadians, as Communist China does with its “social credit” system. Allowing the government to peer into and influence Canadians’ purchasing behaviours could have a profoundly damaging impact on their privacy and autonomy, cautions the report.

READ: Financial expert warns all-digital monetary system would enable ‘complete control’ of citizens

Canada is not the first jurisdiction to explore a CBDC. This report evaluates the Bank of Canada’s exploration within a global context, applying lessons learned from jurisdictions like Nigeria, the Caribbean, and others.

After analyzing negative outcomes of “going cashless” in jurisdictions such as Australia, Sweden, Finland, and Norway, this report advocates for the value of cash and the need for robust institutional and legislative protections for the use of cash.

Ben Klassen, Education Programs Coordinator at the Justice Centre and lead author of the report, stated, “Many Canadian politicians and policy designers would have us participate in a frantic (and global) race to digitize goods and services, including our dollar. The finish line, we are told, promises heightened profitability, convenience, and security. While the pursuit of innovation and efficiency can deliver worthwhile rewards, we must always remember the values of privacy, autonomy, security, equality, and access to economic participation. Adopting a central bank digital currency risks excluding the homeless, the elderly, the ‘internetless,’ the technologically illiterate, and the conscientious objector.”

“Most seriously, a central bank digital currency could hand incredible power to the Government and Bank of Canada to monitor financial transactions, punish whatever behaviours the government deems undesirable, and penalize those on the wrong side of government ambitions,” continued Mr. Klassen. “This issue should be framed as a contrast between a ‘digital dollar’ and a ‘human dollar’ – our currency cannot be designed without regard for the humans and human values that will be profoundly impacted by its design.”

READ: RFK Jr. warns Americans ‘will be slaves’ if central bank digital currency is established

This report was produced in collaboration with Sharon Polsky – President of AMINAcorp.ca, President of the Privacy & Access Council of Canada, and a Privacy by Design Ambassador with more than 30 years’ experience in advising governments and policy designers on privacy and access matters.

Reprinted with permission from the Justice Centre for Constitutional Freedoms.

Elon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

CBS settles with Trump over doctored 60 Minutes Harris interview

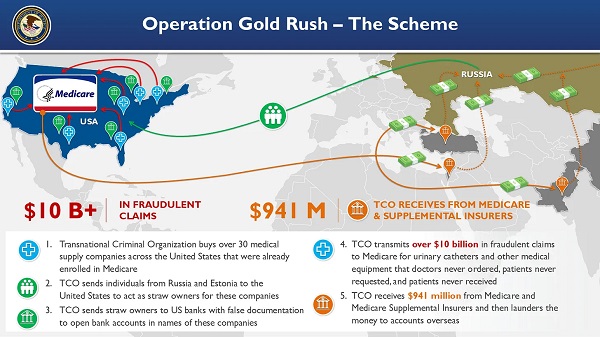

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

Alberta Provincial Police – New chief of Independent Agency Police Service

-

Disaster2 days ago

Disaster2 days agoTexas flood kills 43 including children at Christian camp

-

Daily Caller2 days ago

Daily Caller2 days agoTrump’s One Big Beautiful Bill Resets The Energy Policy Playing Field

-

Alberta1 day ago

Alberta1 day agoAlberta Next: Immigration

-

Business2 days ago

Business2 days agoThe Digital Services Tax Q&A: “It was going to be complicated and messy”

-

International2 days ago

International2 days agoElon Musk forms America Party after split with Trump

-

Crime14 hours ago

Crime14 hours agoNews Jeffrey Epstein did not have a client list, nor did he kill himself, Trump DOJ, FBI claim

-

COVID-1912 hours ago

COVID-1912 hours agoFDA requires new warning on mRNA COVID shots due to heart damage in young men

-

Alberta Sports Hall of Fame and Museum23 hours ago

Alberta Sports Hall of Fame and Museum23 hours agoAlberta Sports Hall of Fame 2025 Inductee Profiles – Para Nordic Skiing – Brian and Robin McKeever