Alberta

Why the oilsands’ weaknesses are turning into strengths

From the MacDonald Laurier Institute

By Heather Exner-Pirot

Global oil prices are recovering from a multi-year bust

Few industrial projects have been more maligned than Canada’s oilsands. It has been called tar sands, a carbon bomb, the “dirtiest oil on the planet.” It’s suffered through the shale revolution, the COVID-19 shutdown, and a torrent of ESG (Environmental, Social and Governance) divestment. Its grade of heavy oil has been discounted and shunned.

But despite the challenges, things are coming up roses. In almost every aspect of the sector that has looked weak in the past decade—costs, grade, carbon intensity—the oilsands are coming on strong, and poised to provide unprecedented revenue streams for Canadian public coffers.

Oilsands are known as “unconventional” oil, which is extraction from anything other than traditional, vertical wells. In northern Alberta, the expansive hydrocarbon resources are in bitumen form, a molasses-like consistency too heavy to flow on its own. It takes a lot of capital and energy to turn the oilsands’ oil into a product that can be transported, refined and used by consumers.

For this reason, the oilsands were seen in the early 2010s as an expensive form of oil, with high up-front costs and a high break-even price: up to USD$75/barrel for new oilsands mines. This made it difficult to compete with cheaper American shale, which came online at scale at the same time as the oilsands, to great chagrin in Calgary.

However, global oil prices are recovering from a multi-year bust, and new “in-situ” extraction technologies have greatly reduced oilsands recovery costs. Break-even prices now average less than USD$40/barrel, and BMO Capital Markets assessed in September that the average oilsands producers could cover their capital budgets and base dividends at USD$46/barrel. By contrast the average large U.S. producer requires USD$53.50/barrel. For new shale wells outside of Texas last year, it was $69/barrel.

Another advantage is that oilsands are low-decline, which means they have decades of inventory, or oil available to be extracted. Shale oil sites have declined as high as 50 percent in the first year. While the oilsands reap the benefits of past investments, shale producers need to continuously drill and invest in new production. (But they haven’t been of late: the U.S. oil rig count has fallen 21 percent since December 2022, largely because of new well costs.)

Another challenge for the oilsands has been its grade: “heavy” or dense, and “sour” or high in sulfur. Light, sweet crudes are easier to refine and have historically sold at a premium. The difference can be stark: at its worst in 2018, West Texas Intermediate (WTI) oil sold for USD$57 a barrel, compared to just USD$11 for heavy Western Canada Select (WCS).

But heavy oil has qualities that are desirable, even necessary for some refined products. Whereas light crude is primarily made into fuels, heavy oil is advantageous for plastics, petrochemicals, other fuels, and road surfacing: things we will still need in a post-combustion, net-zero world. Many American refineries are configured to process heavy oil. Because the U.S. produces virtually none itself, they depend on cheap Canadian sources.

Geopolitical factors are also bolstering heavy and sour oil. Recent production cuts by OPEC+, designed to lift global oil prices, have limited supply of medium and heavy sour grades, which matches the kind of oil the Biden Administration released in its big Strategic Petroleum Reserve sell-off last year. This has brought higher prices for heavy, sour oil, more good news for the oilsands.

As for the oilsands’ biggest Achilles heel, its carbon intensity, this is another weakness turning into a strength. The oilsands are geographically concentrated, with a small number of facilities producing large amounts of emissions. This makes them far easier to decarbonize than conventional oil, which needs huge fleets of rigs creating hundreds of emissions sources in order to produce comparable amounts of oil. Seizing the opportunity, the major oilsands producers are working together on one of the biggest carbon capture projects in the world, building a 400-km CO₂ pipeline that could link over 20 CCS facilities with a carbon storage hub in northeast Alberta. Small modular reactors are another option being explored to reduce emissions. It’s not easy or cheap, but it’s possible to reach net zero, which producers plan to do by 2050.

All of this is not just good news for the oilsands, but for Albertans and Canadians as well. In 2022, royalties going into public coffers from oil and gas extraction hit a record $33.8 billion; that’s more than all royalties from 2016-20 combined. The boost comes not just from higher prices but from Alberta’s strategy to charge significantly higher royalties—up to 40 percent—from oilsands facilities whose upfront development costs have been paid off and revenues are exceeding operating expenses.

A large number of facilities have already reached this threshold, and more are added each year. This flexible new paradigm of permanently higher royalties helps governments moderate the budget rollercoaster of volatile oil prices: nine times more at $55/barrel, and four and half times more at $120/barrel. Next year, when the TMX pipeline adds more than half a million barrels a day of capacity from the oilsands to new markets, the value of royalties will also increase, along with corporate taxes.

Of course, the oilsands still face headwinds from Ottawa, none bigger than a proposal to reduce oil and gas emissions by 42 percent (from 2019 levels) by 2030. Although the oil and gas sector has invested heavily in emissions reductions, and greenhouse gas intensity per barrel fell 20 percent between 2009 and 2020, there is no way to meet the new target without cutting production. S&P Global estimates that 1.3 million barrels of daily output will need to be slashed, which would be an existential threat to the sector. Fortunately, the political tide in Canada is turning in such a way that the oilsands could hang on long enough to see friendlier policies.

Finally, the oilsands remain unloved by investors, although the tide has been turning with higher prices. Their enterprise multiple (EV/DACF), a standard valuation formula, is on average 5.8x as of September and was even lower in 2022. This is much lower than the S&P 500, which has averaged between 11 to 16x in the last few years. In Calgary this has been called the Ottawa penalty box: the only logical explanation for their low valuation seems to be the lack of confidence investors associate with the Canadian energy policy landscape. At any rate, oilsands companies are currently free cashflow machines and are rewarding the shareholders they do have with share buybacks.

After nearly a decade on their back foot, the oilsands have reason for optimism. Lots of people still love to hate them, but they’re starting to rack up some wins.

Heather Exner-Pirot is the director of energy, natural resources and environment at the Macdonald-Laurier Institute.

From the Canadian Energy Centre

Canada’s energy landscape changed significantly in 2025, with mounting U.S. economic pressures reinforcing the central role oil and gas can play in safeguarding the country’s independence.

Here are the Canadian Energy Centre’s top five most-viewed stories of the year.

5. Alberta’s massive oil and gas reserves keep growing – here’s why

The Northern Lights, aurora borealis, make an appearance over pumpjacks near Cremona, Alta., Thursday, Oct. 10, 2024. CP Images photo

Analysis commissioned this spring by the Alberta Energy Regulator increased the province’s natural gas reserves by more than 400 per cent, bumping Canada into the global top 10.

Even with record production, Alberta’s oil reserves – already fourth in the world – also increased by seven billion barrels.

According to McDaniel & Associates, which conducted the report, these reserves are likely to become increasingly important as global demand continues to rise and there is limited production growth from other sources, including the United States.

4. Canada’s pipeline builders ready to get to work

Photo courtesy Coastal GasLink

Canada could be on the cusp of a “golden age” for building major energy projects, said Kevin O’Donnell, executive director of the Mississauga, Ont.-based Pipe Line Contractors Association of Canada.

That eagerness is shared by the Edmonton-based Progressive Contractors Association of Canada (PCA), which launched a “Let’s Get Building” advocacy campaign urging all Canadian politicians to focus on getting major projects built.

“The sooner these nation-building projects get underway, the sooner Canadians reap the rewards through new trading partnerships, good jobs and a more stable economy,” said PCA chief executive Paul de Jong.

3. New Canadian oil and gas pipelines a $38 billion missed opportunity, says Montreal Economic Institute

Steel pipe in storage for the Trans Mountain Pipeline expansion in 2022. Photo courtesy Trans Mountain Corporation

In March, a report by the Montreal Economic Institute (MEI) underscored the economic opportunity of Canada building new pipeline export capacity.

MEI found that if the proposed Energy East and Gazoduq/GNL Quebec projects had been built, Canada would have been able to export $38 billion worth of oil and gas to non-U.S. destinations in 2024.

“We would be able to have more prosperity for Canada, more revenue for governments because they collect royalties that go to government programs,” said MEI senior policy analyst Gabriel Giguère.

“I believe everybody’s winning with these kinds of infrastructure projects.”

2. Keyera ‘Canadianizes’ natural gas liquids with $5.15 billion acquisition

Keyera Corp.’s natural gas liquids facilities in Fort Saskatchewan, Alta. Photo courtesy Keyera Corp.

In June, Keyera Corp. announced a $5.15 billion deal to acquire the majority of Plains American Pipelines LLP’s Canadian natural gas liquids (NGL) business, creating a cross-Canada NGL corridor that includes a storage hub in Sarnia, Ontario.

The acquisition will connect NGLs from the growing Montney and Duvernay plays in Alberta and B.C. to markets in central Canada and the eastern U.S. seaboard.

“Having a Canadian source for natural gas would be our preference,” said Sarnia mayor Mike Bradley.

“We see Keyera’s acquisition as strengthening our region as an energy hub.”

1. Explained: Why Canadian oil is so important to the United States

Enbridge’s Cheecham Terminal near Fort McMurray, Alberta is a key oil storage hub that moves light and heavy crude along the Enbridge network. Photo courtesy Enbridge

The United States has become the world’s largest oil producer, but its reliance on oil imports from Canada has never been higher.

Many refineries in the United States are specifically designed to process heavy oil, primarily in the U.S. Midwest and U.S. Gulf Coast.

According to the Alberta Petroleum Marketing Commission, the top five U.S. refineries running the most Alberta crude are:

- Marathon Petroleum, Robinson, Illinois (100% Alberta crude)

- Exxon Mobil, Joliet, Illinois (96% Alberta crude)

- CHS Inc., Laurel, Montana (95% Alberta crude)

- Phillips 66, Billings, Montana (92% Alberta crude)

- Citgo, Lemont, Illinois (78% Alberta crude)

Pathways Alliance CEO Kendall Dilling is interviewed at the World Petroleum Congress in Calgary, Monday, Sept. 18, 2023.THE CANADIAN PRESS/Jeff McIntosh

From Resource Works

Carbon capture gives biggest bang for carbon tax buck CCS much cheaper than fuel switching: report

Canada’s climate change strategy is now joined at the hip to a pipeline. Two pipelines, actually — one for oil, one for carbon dioxide.

The MOU signed between Ottawa and Alberta two weeks ago ties a new oil pipeline to the Pathways Alliance, which includes what has been billed as the largest carbon capture proposal in the world.

One cannot proceed without the other. It’s quite possible neither will proceed.

The timing for multi-billion dollar carbon capture projects in general may be off, given the retreat we are now seeing from industry and government on decarbonization, especially in the U.S., our biggest energy customer and competitor.

But if the public, industry and our governments still think getting Canada’s GHG emissions down is a priority, decarbonizing Alberta oil, gas and heavy industry through CCS promises to be the most cost-effective technology approach.

New modelling by Clean Prosperity, a climate policy organization, finds large-scale carbon capture gets the biggest bang for the carbon tax buck.

Which makes sense. If oil and gas production in Alberta is Canada’s single largest emitter of CO2 and methane, it stands to reason that methane abatement and sequestering CO2 from oil and gas production is where the biggest gains are to be had.

A number of CCS projects are already in operation in Alberta, including Shell’s Quest project, which captures about 1 million tonnes of CO2 annually from the Scotford upgrader.

What is CO2 worth?

Clean Prosperity estimates industrial carbon pricing of $130 to $150 per tonne in Alberta and CCS could result in $90 billion in investment and 70 megatons (MT) annually of GHG abatement or sequestration. The lion’s share of that would come from CCS.

To put that in perspective, 70 MT is 10% of Canada’s total GHG emissions (694 MT).

The report cautions that these estimates are “hypothetical” and gives no timelines.

All of the main policy tools recommended by Clean Prosperity to achieve these GHG reductions are contained in the Ottawa-Alberta MOU.

One important policy in the MOU includes enhanced oil recovery (EOR), in which CO2 is injected into older conventional oil wells to increase output. While this increases oil production, it also sequesters large amounts of CO2.

Under Trudeau era policies, EOR was excluded from federal CCS tax credits. The MOU extends credits and other incentives to EOR, which improves the value proposition for carbon capture.

Under the MOU, Alberta agrees to raise its industrial carbon pricing from the current $95 per tonne to a minimum of $130 per tonne under its TIER system (Technology Innovation and Emission Reduction).

The biggest bang for the buck

Using a price of $130 to $150 per tonne, Clean Prosperity looked at two main pathways to GHG reductions: fuel switching in the power sector and CCS.

Fuel switching would involve replacing natural gas power generation with renewables, nuclear power, renewable natural gas or hydrogen.

“We calculated that fuel switching is more expensive,” Brendan Frank, director of policy and strategy for Clean Prosperity, told me.

Achieving the same GHG reductions through fuel switching would require industrial carbon prices of $300 to $1,000 per tonne, Frank said.

Clean Prosperity looked at five big sectoral emitters: oil and gas extraction, chemical manufacturing, pipeline transportation, petroleum refining, and cement manufacturing.

“We find that CCUS represents the largest opportunity for meaningful, cost-effective emissions reductions across five sectors,” the report states.

Fuel switching requires higher carbon prices than CCUS.

Measures like energy efficiency and methane abatement are included in Clean Prosperity’s calculations, but again CCS takes the biggest bite out of Alberta’s GHGs.

“Efficiency and (methane) abatement are a portion of it, but it’s a fairly small slice,” Frank said. “The overwhelming majority of it is in carbon capture.”

From left, Alberta Minister of Energy Marg McCuaig-Boyd, Shell Canada President Lorraine Mitchelmore, CEO of Royal Dutch Shell Ben van Beurden, Marathon Oil Executive Brian Maynard, Shell ER Manager, Stephen Velthuizen, and British High Commissioner to Canada Howard Drake open the valve to the Quest carbon capture and storage facility in Fort Saskatchewan Alta, on Friday November 6, 2015. Quest is designed to capture and safely store more than one million tonnes of CO2 each year an equivalent to the emissions from about 250,000 cars. THE CANADIAN PRESS/Jason Franson

Credit where credit is due

Setting an industrial carbon price is one thing. Putting it into effect through a workable carbon credit market is another.

“A high headline price is meaningless without higher credit prices,” the report states.

“TIER credit prices have declined steadily since 2023 and traded below $20 per tonne as of November 2025. With credit prices this low, the $95 per tonne headline price has a negligible effect on investment decisions and carbon markets will not drive CCUS deployment or fuel switching.”

Clean Prosperity recommends a kind of government-backstopped insurance mechanism guaranteeing carbon credit prices, which could otherwise be vulnerable to political and market vagaries.

Specifically, it recommends carbon contracts for difference (CCfD).

“A straight-forward way to think about it is insurance,” Frank explains.

Carbon credit prices are vulnerable to risks, including “stroke-of-pen risks,” in which governments change or cancel price schedules. There are also market risks.

CCfDs are contractual agreements between the private sector and government that guarantees a specific credit value over a specified time period.

“The private actor basically has insurance that the credits they’ll generate, as a result of making whatever low-carbon investment they’re after, will get a certain amount of revenue,” Frank said. “That certainty is enough to, in our view, unlock a lot of these projects.”

From the perspective of Canadian CCS equipment manufacturers like Vancouver’s Svante, there is one policy piece still missing from the MOU: eligibility for the Clean Technology Manufacturing (CTM) Investment tax credit.

“Carbon capture was left out of that,” said Svante co-founder Brett Henkel said.

Svante recently built a major manufacturing plant in Burnaby for its carbon capture filters and machines, with many of its prospective customers expected to be in the U.S.

The $20 billion Pathways project could be a huge boon for Canadian companies like Svante and Calgary’s Entropy. But there is fear Canadian CCS equipment manufacturers could be shut out of the project.

“If the oil sands companies put out for a bid all this equipment that’s needed, it is highly likely that a lot of that equipment is sourced outside of Canada, because the support for Canadian manufacturing is not there,” Henkel said.

Henkel hopes to see CCS manufacturing added to the eligibility for the CTM investment tax credit.

“To really build this eco-system in Canada and to support the Pathways Alliance project, we need that amendment to happen.”

Resource Works News

Alberta Next Panel calls for less Ottawa—and it could pay off

“Magnitude cannot be overstated”: Minnesota aid scam may reach $9 billion

Largest fraud in US history? Independent Journalist visits numerous daycare centres with no children, revealing massive scam

US Under Secretary of State Slams UK and EU Over Online Speech Regulation, Announces Release of Files on Past Censorship Efforts

Sweden Fixed What Canada Won’t Even Name

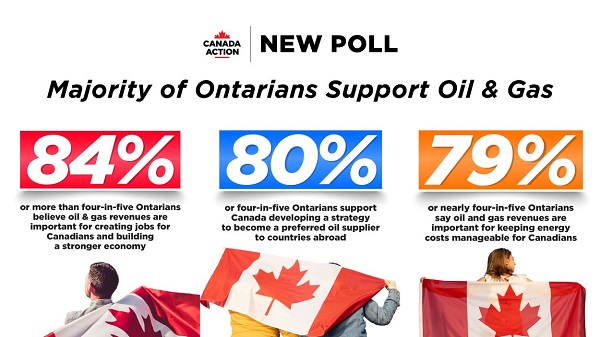

New Poll Shows Ontarians See Oil & Gas as Key to Jobs, Economy, and Trade

Socialism vs. Capitalism

-

Alberta2 days ago

The Canadian Energy Centre’s biggest stories of 2025

-

Business2 days ago

Business2 days agoOttawa Is Still Dodging The China Interference Threat

-

Business2 days ago

Business2 days agoResurfaced Video Shows How Somali Scammers Used Day Care Centers To Scam State

-

Business1 day ago

Business1 day agoDark clouds loom over Canada’s economy in 2026

-

Business1 day ago

Business1 day agoThe Real Reason Canada’s Health Care System Is Failing

-

Business2 days ago

Business2 days agoMinneapolis day care filmed empty suddenly fills with kids

-

Business2 days ago

Business2 days agoDisclosures reveal Minnesota politician’s husband’s companies surged thousands-fold amid Somali fraud crisis

-

Addictions22 hours ago

Addictions22 hours agoCoffee, Nicotine, and the Politics of Acceptable Addiction