National

The documentary rocking Vancouver and shocking Canadians

From Aaron Gunn of Politics Explained

SUBSCRIBE:  / aarongunnbc

/ aarongunnbc

SUPPORT ME: https://www.aarongunn.ca/contribute

FOLLOW ME: Instagram: https://www.instagram.com/aarongunnbc Facebook: https://www.facebook.com/aarongunn.ca Twitter: https://www.twitter.com/aarongunn

AARON IS AN INDEPENDENT JOURNALIST, AND ADVOCATE FOR TAXPAYERS AND COMMON SENSE

Aaron is Producer/Director of the hit online series, Politics Explained.

His videos have targeted, among others, the Insurance Corporation of British Columbia (ICBC) for dramatically raising rates on BC drivers; Victoria Mayor Lisa Helps for tearing down the statue of Sir John A. Macdonald; Canada’s Justice System for its treatment of child murderers; and Prime Minister Justin Trudeau for his massive deficits, destructive energy policy and obsession with political correctness.

Throughout, Aaron has demonstrated his commitment to lower taxes, less waste and a stronger Canada. His content, which he writes and produces himself, is funded by the generous contributions of ordinary, taxpaying Canadians. His videos, which are filmed across the country, have together been shared hundreds of thousands of times.

Prior to his work as Spokesperson for BC Proud (2017-19), Aaron worked for the Canadian Taxpayers Federation (CTF) where he founded and became Executive Director of the Generation Screwed initiative, fighting back against government debt and its impact on future generations.

By the end of his tenure at the CTF, Generation Screwed had achieved a considerable online following and established a physical presence at over 30 university campuses across Canada.

Aaron has a Bachelor’s Degree of Commerce from the University of Victoria. He served three years in the Canadian Army Reserves and operated his own company, which he founded at age 15, for over ten years. Victoria, BC is home.

For media requests or to inquire about public speaking, contact Aaron here.

[This article was originally published in City Journal, a public policy magazine and website published by the Manhattan Institute for Policy Research]

By Adam Zivo

A Canadian poll finds that racial minorities don’t believe drug enforcement is bigoted.

Is drug prohibition racist? Many left-wing institutions seem to think so. But their argument is historically illiterate—and it contradicts recent polling data, too, which show that minorities overwhelmingly reject that view.

Policies and laws are tools to establish order. Like any tool, they can be abused. The first drug laws in North America, dating back to the late nineteenth and early twentieth centuries, arguably fixated on opium as a legal pretext to harass Asian immigrants, for example. But no reasonable person would argue that laws against home invasion, murder, or theft are “racist” because they have been misapplied in past cases. Absent supporting evidence, leaping from “this tool is sometimes used in racist ways” to “this tool is essentially racist” is kindergarten-level reasoning.

Yet this is precisely what institutions and activist groups throughout the Western world have done. The Drug Policy Alliance, a U.S.-based organization, suggests that drug prohibition is rooted in “racism and fear.” Harm Reduction International, a British NGO, argues for legalization on the grounds that drug prohibition entrenches “racialized hierarchies, which were established under colonial control and continue to dominate today.” In Canada, where I live, the top public health official in British Columbia, our most drug-permissive province, released a pro-legalization report last summer claiming that prohibition is “based on a history of racism, white supremacy, paternalism, colonialism, classism and human rights violations.”

These claims ignore how drug prohibition has been and remains popular in many non-European societies. Sharia law has banned the use of mind-altering substances since the seventh century. When Indigenous leaders negotiated treaties with Canadian colonists in the late 1800s, they asked for “the exclusion of fire water (whiskey)” from their communities. That same century, China’s Qing Empire banned opium amid a national addiction crisis. “Opium is a poison, undermining our good customs and morality,” the Daoguang emperor wrote in an 1810 edict.

Today, Asian and Muslim jurisdictions impose much stiffer penalties on drug offenders than do Western nations. In countries like China, Saudi Arabia, Iran, Singapore, and Thailand, addicts and traffickers are given lengthy prison sentences or executed. Meantime, in Canada and the United States, de facto decriminalization has left urban cores littered with syringes and shrouded in clouds of meth.

The anti-drug backlash building in North America appears to be spearheaded by racial minorities. When Chesa Boudin, San Francisco’s former district attorney, was recalled in 2022, support for his ouster was highest among Asian voters. Last fall, 73 percent of Latinos backed California’s Proposition 36, which heightened penalties for drug crimes, while only 58 percent of white respondents did.

In Canada, the first signs of a parallel trend emerged during Vancouver’s 2022 municipal election, where an apparent surge in Chinese Canadian support helped install a slate of pro-police candidates. Then, in British Columbia’s provincial election last autumn, nonwhite voters strongly preferred the BC Conservatives, who campaigned on stricter drug laws. And in last month’s federal election, within both Vancouver and Toronto’s metropolitan areas, tough-on-crime conservatives received considerable support from South Asian communities.

These are all strong indicators that racial minorities do not, in fact, universally favor drug legalization. But their small population share means there is relatively little polling data to measure their preferences. Since only 7.6 percent of Americans are Asian, for example, a poll of 1,000 randomly selected people will yield an average of only 76 Asian respondents—too small a sample from which to draw meaningful conclusions. You can overcome this barrier by commissioning very large polls, but that’s expensive.

Nonetheless, last autumn, the Centre for Responsible Drug Policy (a nonprofit I founded and operate) did just that. In partnership with the Macdonald-Laurier Institute, we contracted Mainstreet Research to ask over 12,000 British Columbians: “Do you agree or disagree that criminalizing drugs is racist?”

The results undermine progressives’ assumptions. Only 26 percent of nonwhite respondents agreed (either strongly or weakly) that drug criminalization is racist, while over twice as many (56 percent) disagreed. The share of nonwhite respondents who strongly disagreed was three times larger than the share that strongly agreed (43.2 percent versus 14.3 percent). These results are fairly conclusive for this jurisdiction, given the poll’s sample size of 2,233 nonwhite respondents and a margin of error of 2 percent.

Notably, Indigenous respondents seemed to be the most anti-drug ethnic group: only 20 percent agreed (weakly or strongly) with the “criminalization is racist” narrative, while 61 percent disagreed. Once again, those who disagreed were much more vehement than those who agreed. With a sample size of 399 respondents, the margin of error here (5 percent) is too small to confound these dramatic results.

We saw similar outcomes for other minority groups, such as South Asians, Southeast Asians, Latinos, and blacks. While Middle Eastern respondents also seemed to follow this trend, the poll included too few of them to draw definitive conclusions. Only East Asians were divided on the issue, though a clear majority still disagreed that criminalization is racist.

As this poll was limited to British Columbian respondents, our findings cannot necessarily be assumed to hold throughout Canada and the United States. But since the province is arguably the most drug-permissive jurisdiction within the two countries, these results could represent the ceiling of pro-drug, anti-criminalization attitudes among minority communities.

Legalization proponents and their progressive allies take pride in being “anti-racist.” Our polling, however, suggests that they are not listening to the communities they profess to care about.

The Bureau is a reader-supported publication.

To receive new posts and support my work, consider becoming a free or paid subscriber.

Invite your friends and earn rewards

![]()

The 21 st century is going to be overshadowed by a crisis that human beings have never faced before. I don’t mean war, pestilence, famine or climate change. Those are perennial troubles. Yes, even climate change, despite the hype, is nothing new as anyone who’s heard of the Roman Warm Period, the Mediaeval Warm Period or the Little Ice Age will know. Climate change and the others are certainly problems, but they aren’t new.

But the crisis that’s coming is new.

The global decline in fertility rates has grown so severe that some demographers now talk about “peak humanity” – a looming maximum from which the world’s population will begin to rapidly decline. Though the doomsayers who preach the dangers of overpopulation may think that’s a good development, it is in fact a grave concern.

In the Canadian context, it is doubly worrisome. Our birth rates have been falling steadily since 1959. It was shortly after that in the 1960s when we began to build a massive welfare state, and we did so despite a shrinking domestically-born population and the prospect of an ever-smaller pool of taxable workers to pay for the expanding social programs.

Immigration came to the rescue, and we became adept at recruiting a surplus population of young, skilled, economically focused migrants seeking their fortune abroad. The many newcomers meant a growing population and with it a larger tax base.

But what would happen if Canada could no longer depend on a steady influx of newcomers? The short answer is that our population would shrink, and our welfare state would come under intolerable strain. The long answer is that Canadian businesses, which have become addicted to abundant, cheap foreign labour through the Temporary Foreign Worker Program, would be obliged to invest in hiring, training and retaining Canadian workers.

Provincial and federal governments would scramble to keep older Canadians in the workforce for longer. And governments would be torn between demands to cut the welfare state or privatize large parts of it while raising taxes to help pay for it.

No matter what, the status quo won’t continue. And – even though Canada is right now taking in record numbers of new immigrants and temporary workers – we are going to discover this soon. The main cause is the “peak humanity” that I mentioned before. Fertility rates are falling rapidly nearly everywhere. In the industrialized West, births have fallen further in some places than in others, but all countries are now below replacement levels

(except Israel, which was at 2.9 in 2020).

Deaths have long been outpacing births in China, Japan and some Western countries like Italy. A recent study in The Lancet expects that by 2100, 97 percent of countries will be shrinking. Only Western and Eastern sub-Saharan Africa will have birth rates above replacement levels, though births will be falling in those regions also.

In a world of sub-replacement fertility, there will still be well-educated, highly skilled people abroad. But there will not be a surplus of them. Some may still be ready and willing to put down roots in Canada, but the number will soon be both small and dwindling. And it seems likely that countries which have produced Canada’s immigrants in recent years will try hard to retain domestic talent as their own populations decline. In contrast, the population of sub-Saharan Africa will be growing for a little longer. But unless education and skills-training change drastically in that region, countries there will not produce the kind of skilled immigrants that Canada has come to rely on.

And so the moment is rapidly approaching when immigration will no longer be able to make up for falling Canadian fertility. Governments will have to confront the problem directly—not years or decades hence, but now.

While many will cite keeping the welfare state solvent as the driving force, in my view this is not the reason to do it. The reason to do it is that it is in Canada’s national interest to make it easier for families to have the number of children that they want. A 2023 study by the think-tank Cardus found that nearly half of Canadian women at the end of their reproductive years had fewer children than they had wanted. This amounted to an average

of 0.5 fewer children per woman – a shortfall that would lift Canada close to replacement level.

The United Nations Population Fund (UNPF) has noticed the same challenge on a global scale. Neither Cardus nor the UNPF prescribes any specific solutions, but their analysis points to the same thing: public policy should focus on identifying and removing barriers families face to having the number of children they want.

Every future government should be vigilant against impediments to family-formation and raising a desired number of children. Making housing more abundant and affordable would surely be a good beginning. Better planning must go into making livable communities (not merely atomized dwellings) with infrastructure favouring families and designed to ease commuting. But more fundamentally, policy-makers will need to ask and answer an uncomfortable question: why did we allow barriers to fertility to arise in the first place?

The original, full-length version of this article was recently published in C2C Journal.

Michael Bonner is a political consultant with Atlas Strategic Advisors, LLC, contributing editor to the Dorchester Review, and author of In Defense of Civilization: How Our Past Can Renew Our Present.

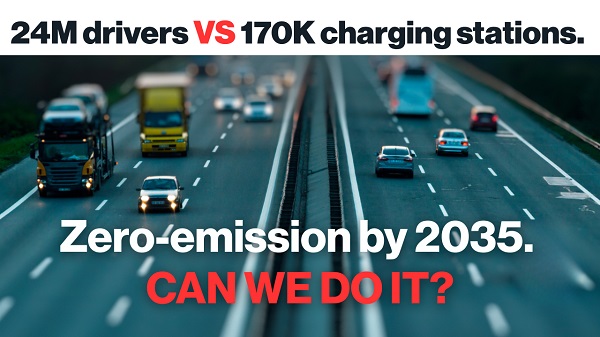

Power Struggle: Electric vehicles and reality

Elon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

China undermining American energy independence, report says

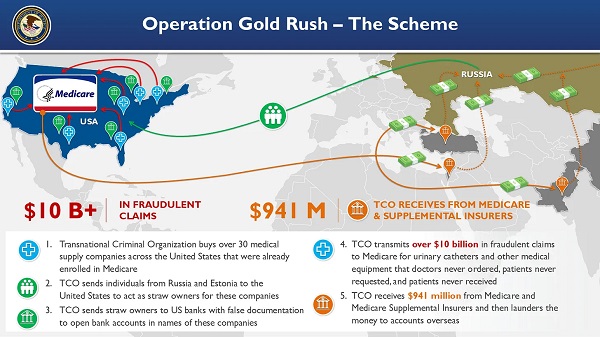

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

Trump on Canada tariff deadline: ‘We can do whatever we want’

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

Electric vehicle sales are falling hard in BC, and it is time to recognize reality.

-

Business1 day ago

Business1 day agoCanada’s loyalty to globalism is bleeding our economy dry

-

Alberta1 day ago

Alberta1 day agoCOVID mandates protester in Canada released on bail after over 2 years in jail

-

armed forces1 day ago

armed forces1 day agoCanada’s Military Can’t Be Fixed With Cash Alone

-

Alberta1 day ago

Alberta1 day agoAlberta Next: Alberta Pension Plan

-

Crime2 days ago

Crime2 days agoProject Sleeping Giant: Inside the Chinese Mercantile Machine Linking Beijing’s Underground Banks and the Sinaloa Cartel

-

International1 day ago

International1 day agoTrump transportation secretary tells governors to remove ‘rainbow crosswalks’

-

Business1 day ago

Business1 day agoCarney’s spending makes Trudeau look like a cheapskate

-

COVID-1921 hours ago

COVID-1921 hours agoCourt compels RCMP and TD Bank to hand over records related to freezing of peaceful protestor’s bank accounts