Business

Global Affairs Canada goes on real estate spending spree, taxpayers foot the bill

From the Canadian Taxpayers Federation

By Ryan Thorpe

Records obtained by the CTF show Clark’s lavish condo is just the tip of the iceberg, with the department dropping taxpayer cash on other luxury properties around the world.

Official residences in other countries: $38 million.

Properties in Afghanistan abandoned to the Taliban: $41 million.

Vacant land in Senegal: $12.5 million.

A chancery in Ukraine: $10.2 million.

Those are some of the holdings in Global Affairs Canada’s real estate portfolio, which has cost taxpayers $186 million in the past 10 years alone.

All told, Global Affairs Canada owns more than 400 properties in more than 70 countries, according to access-to-information records obtained by the Canadian Taxpayers Federation.

“Do we really need the government dropping tens of millions of dollars on official residences half-way around the world?” said Franco Terrazzano, CTF Federal Director. “Better question, does Senegal not have vacant land available for less than eight figures?

“With the government more than $1 trillion in debt, taxpayers need to know why the government is spending so much of our money overseas.”

Global Affairs Canada is embroiled in controversy after it purchased a $9-million luxury condo for New York Consul General Tom Clark amid a housing and cost-of-living crisis.

The records obtained by the CTF show Clark’s lavish condo is just the tip of the iceberg, with the department dropping taxpayer cash on other luxury properties around the world.

Global Affairs Canada has spent $38.4 million on official residences since 2014, including New Zealand ($2.4 million), Barbados ($3.8 million) and Trinidad and Tobago ($2.5 million), among others.

In London, U.K., Global Affairs Canada spent $58 million on 23 properties since 2015, all of which serve as “staff quarters,” according to the records. All told, Global Affairs Canada owns 65 properties in London purchased for $208 million.

In Kabul, Afghanistan, Global Affairs Canada spent $41 million on three properties in late 2018 and 2019, which have since been abandoned to the Taliban.

Prior to the first property in Kabul being purchased, the U.S. had already begun negotiations with the Taliban for an end to the Afghanistan War.

Seven months after Global Affairs Canada purchased the last property in Kabul, the U.S. struck a deal with the Taliban for the withdrawal of American troops from the country.

On Aug. 15, 2021, Canada pulled its presence from Afghanistan.

“We have … been unable to inspect the state of these properties since that date,” Global Affairs Canada told the CTF in a written statement.

In October 2021, the Globe and Mail reported that “Islamist militants now guard the former headquarters of Canada’s diplomatic mission in the Afghan capital.”

“This is a lot of taxpayers’ money to spend on new property in Afghanistan when our ally had already been clear it was preparing to leave,” Terrazzano said. “Canadian taxpayers are out $41 million and the Taliban now has new digs, so is anyone in government going to answer for the decision to purchase these properties?”

In Kyiv, Ukraine, Global Affairs Canada purchased a chancery for $10.2 million in 2017.

In Senegal, a country in West Africa, Global Affairs Canada bought $12.5 million worth of “vacant land” in 2022.

“Global Affairs Canada’s real estate portfolio is bloated and the taxpayer tab is ludicrous,” Terrazzano said. “Someone in government must explain what value taxpayers are supposedly getting for the hundreds of millions of dollars spent on all these lavish properties in far flung countries.

“And if Canadians aren’t getting real value, then it’s time to sell off properties so taxpayers can recoup some of this money.”

Alberta

COWBOY UP! Pierre Poilievre Promises to Fight for Oil and Gas, a Stronger Military and the Interests of Western Canada

Fr0m Energy Now

As Calgarians take a break from the incessant news of tariff threat deadlines and global economic challenges to celebrate the annual Stampede, Conservative party leader Pierre Poilievre gave them even more to celebrate.

Poilievre returned to Calgary, his hometown, to outline his plan to amplify the legitimate demands of Western Canada and not only fight for oil and gas, but also fight for the interests of farmers, for low taxes, for decentralization, a stronger military and a smaller federal government.

Speaking at the annual Conservative party BBQ at Heritage Park in Calgary (a place Poilievre often visited on school trips growing up), he was reminded of the challenges his family experienced during the years when Trudeau senior was Prime Minister and the disastrous effect of his economic policies.

“I was born in ’79,” Poilievre said. “and only a few years later, Pierre Elliott Trudeau would attack our province with the National Energy Program. There are still a few that remember it. At the same time, he hammered the entire country with money printing deficits that gave us the worst inflation and interest rates in our history. Our family actually lost our home, and we had to scrimp and save and get help from extended family in order to get our little place in Shaughnessy, which my mother still lives in.”

This very personal story resonated with many in the crowd who are now experiencing an affordability crisis that leaves families struggling and young adults unable to afford their first house or condo. Poilievre said that the experience was a powerful motivator for his entry into politics. He wasted no time in proposing a solution – build alliances with other provinces with mutual interests, and he emphasized the importance of advocating for provincial needs.

“Let’s build an alliance with British Columbians who want to ship liquefied natural gas out of the Pacific Coast to Asia, and with Saskatchewanians, Newfoundlanders and Labradorians who want to develop their oil and gas and aren’t interested in having anyone in Ottawa cap how much they can produce. Let’s build alliances with Manitobans who want to ship oil in the port of Churchill… with Quebec and other provinces that want to decentralize our country and get Ottawa out of our business so that provinces and people can make their own decisions.”

Poilievre heavily criticized the federal government’s spending and policies of the last decade, including the increase in government costs, and he highlighted the negative impact of those policies on economic stability and warned of the dangers of high inflation and debt. He advocated strongly for a free-market economy, advocating for less government intervention, where businesses compete to impress customers rather than impress politicians. He also addressed the decade-long practice of blocking and then subsidizing certain industries. Poilievre referred to a famous quote from Ronald Reagan as the modus operandi of the current federal regime.

“The Government’s view of the economy could be summed up in a few short phrases. If anything moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

The practice of blocking and then subsidizing is merely a ploy to grab power, according to Poilievre, making industry far too reliant on government control.

“By blocking you from doing something and then making you ask the government to help you do it, it makes you reliant. It puts them at the center of all power, and that is their mission…a full government takeover of our economy. There’s a core difference between an economy controlled by the government and one controlled by the free market. Businesses have to clamour to please politicians and bureaucrats. In a free market (which we favour), businesses clamour to impress customers. The idea is to put people in charge of their economic lives by letting them have free exchange of work for wages, product for payment and investment for interest.”

Poilievre also said he plans to oppose any ban on gas-powered vehicles, saying, “You should be in the driver’s seat and have the freedom to decide.” This is in reference to the Trudeau-era plan to ban the sale of gas-powered cars by 2035, which the Carney government has said they have no intention to change, even though automakers are indicating that the targets cannot be met. He also intends to oppose the Industrial Carbon tax, Bill C-69 the Impact Assessment Act, Bill C-48 the Oil tanker ban, the proposed emissions cap which will cap energy production, as well as the single-use plastics ban and Bill C-11, also known as the Online Streaming Act and the proposed “Online Harms Act,” also known as Bill C-63. Poilievre closed with rallying thoughts that had a distinctive Western flavour.

“Fighting for these values is never easy. Change, as we’ve seen, is not easy. Nothing worth doing is easy… Making Alberta was hard. Making Canada, the country we love, was even harder. But we don’t back down, and we don’t run away. When things get hard, we dust ourselves off, we get back in the saddle, and we gallop forward to the fight.”

Cowboy up, Mr. Poilievre.

Maureen McCall is an energy professional who writes on issues affecting the energy industry.

From the Fraser Institute

In his June speech announcing a major buildup of Canada’s military, Prime Minister Mark Carney repeated his belief that this country faces a “hinge moment” of the sort the allied countries confronted after the Second World War.

A better comparison might be with the beginning of the war itself.

Then, the Allies found themselves at war with an autocratic state bent on their defeat and possible destruction. Now, Carney faces an antagonistic American president bent on annexing Canada through economic warfare.

Then, Canada rose to the challenge, creating the world’s third-largest navy and landing an army at Normandy on D-Day. Now, Carney has announced the most aggressive reorienting of Canada’s economic, foreign and defence policies in generations.

Polls show strong support among Canadians for this new agenda. But the old Canada is still there. It will fight back. It may yet win.

The situation certainly would have been more encouraging had Carney not inherited Justin Trudeau’s legacy of severe economic and environmental restrictions—picking economic winners and losers rather than letting the market decide—and chronic deficits. The new prime minister would do well to dismantle as much of that legacy as he can.

Some advocate a return to the more laissez-faire approach of Stephen Harper’s government. But Harper didn’t confront a belligerent president hoping to annex Canada through the “economic force” of tariff walls.

The prime minister succeeded in getting Bill C-5, which is intended to weaken at least some of the restrictions on resource development and infrastructure, passed into law. He and the premiers pledge to finally dismantle generations of internal trade and labour mobility barriers. If we must trade less with the Americans, we can at least learn to trade with ourselves.

And the prime minister deserves high praise for reversing decades of military decline through increased spending and efforts to improve procurement. If Carney accomplishes nothing more than restoring Canada’s defences, especially in the Arctic, he will be well remembered.

That said, major challenges confront the Carney agenda.

There’s much talk about a new national energy corridor. But what does that mean? One KPMG executive defined it as a “dedicated, streamlined pathway for the energy, electricity, decarbonization, transportation and digital infrastructure.”

Yes, but what does that mean?

Whatever it means, some First Nations will oppose it tooth-and-nail. Not all of them, mind you. The First Nations Major Project Coalition is dedicated to assisting First Nations in working with government and the private sector for the benefit of all. But many First Nations people consider resource development further exploitation of their ancestral lands by a colonizing power. At the first major proposal to which they do not buy in, they will take the government to court.

What investor will be willing to commit to a project that could be blocked for years as First Nations and Ottawa fight it out all the way to the Supreme Court?

The prime minister, formerly a fervent advocate of combatting climate change, now talks about developing “conventional energy,” which means oil and gas pipelines. But environmental activists will fiercely oppose those pipelines.

There is so much that could go wrong. Sweep away those internal trade barriers? Some premiers will resist. Accelerate housing development? Some mayors will resist. Expand exports to Europe and Asia? Some businesses and entrepreneurs will say it’s not worth the risk.

As for the massive increase in defence spending, where will the money come from? What will be next year’s deficit? What will be the deficit’s impact on inflation, interest rates and sovereign creditworthiness? The obstacles are high enough to make anyone wonder how much, if any, of the government’s platform will be realized. But other factors are at work as well, factors that were also present in 1939.

To execute his mandate, Carney is surrounding himself with what, back in the Second World War, were called “dollar a year men”—executives who came to Ottawa from the private sector to mobilize the economy for wartime.

In Carney’s case he has brought in Marc-André Blanchard as chief of staff and Michael Sabia as clerk of the privy council. Both are highly experienced in government and the private sector. Both are taking very large pay cuts because, presumably, they understand the gravity of the times and believe in the prime minister’s plans.

Most important, Carney’s agenda has broad support from a public that fears for the country’s future and will have little patience toward any group seeking to block the prime minister’s agenda.

Millions of Canadians want this government’s reform efforts to succeed. Those who would put it at risk of failing will have to contend with public anger. That gives Carney a shot at making real change.

John Ibbitson

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

Elon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

CBS settles with Trump over doctored 60 Minutes Harris interview

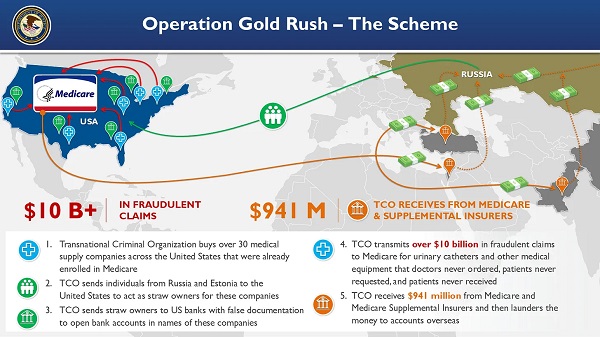

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

Alberta Provincial Police – New chief of Independent Agency Police Service

-

Alberta1 day ago

Alberta1 day agoAlberta Next: Immigration

-

International2 days ago

International2 days agoElon Musk forms America Party after split with Trump

-

Business2 days ago

Business2 days agoThe Digital Services Tax Q&A: “It was going to be complicated and messy”

-

Crime16 hours ago

Crime16 hours agoNews Jeffrey Epstein did not have a client list, nor did he kill himself, Trump DOJ, FBI claim

-

COVID-1914 hours ago

COVID-1914 hours agoFDA requires new warning on mRNA COVID shots due to heart damage in young men

-

Business12 hours ago

Carney’s new agenda faces old Canadian problems

-

Bruce Dowbiggin12 hours ago

Bruce Dowbiggin12 hours agoEau Canada! Join Us In An Inclusive New National Anthem

-

Alberta Sports Hall of Fame and Museum1 day ago

Alberta Sports Hall of Fame and Museum1 day agoAlberta Sports Hall of Fame 2025 Inductee Profiles – Para Nordic Skiing – Brian and Robin McKeever