Fraser Institute

Federal government cranked up spending up but Canadians are worse off

From the Fraser Institute

By Matthew Lau

“If spending money like water was the answer to our country’s problems,” Margaret Thatcher said in 1980, less than two years after the United Kingdom’s Winter of Discontent, “we would have no problems now. If ever a nation has spent, spent, spent, and spent again, ours has.” That a government cannot spend away the country’s problems is a clear lesson of history. The Trudeau government evidently has not learned this—it has spent, spent and spent more, and the country’s problems have gotten worse.

In 2014-15, before the Liberals took office, federal program spending was 12.8 per cent of GDP (the value of final goods and services produced in Canada). In 2023-24, it’s projected at 15.7 per cent. And relative to 2014-15, annual program spending is $89 billion higher than if it had tracked with overall economic growth.

As Thatcher would have predicted, this extra spending has not solved most problems. Consider health care. The Fraser Institute’s survey of health-care specialists found a median wait time of 27.7 weeks between referral from a general practitioner and receipt of treatment in 2023—a 51 per cent increase versus the 18.3 weeks in 2015. Relative to peer countries, Canada is a big health-care spender but with poor results, and is far below average on key metrics such as physicians and hospital beds per capita.

Another big spending area is climate change. The Liberals boast of pouring more than $120 billion into climate programs, but even with an annually increasing carbon tax and onerous regulation on top of that spending, the government is on track to miss its 2030 climate targets. Given the high cost of its climate policies relative to environmental benefits, that’s not a bad thing. Ottawa’s climate targets are wildly unrealistic, and achieving them would mean devastating the economy further.

Speaking of devasting the economy, when the Trudeau government spends, it claims it will support economic growth, increase affordability or otherwise deliver financial benefits. Eight years in, these benefits have not materialized. As of the third quarter of 2023, after five consecutive quarters of declining real GDP per capita, Canada’s cumulative growth in the past eight years is a paltry 1.6 per cent versus 14.7 per cent in the United States. One way to think about this gap: if Canada’s real GDP per-capita growth tracked with the U.S. since the Liberals took office, Canadian living standards would be about 12.8 per cent higher than they are today.

Finally, the Trudeau government has significantly ramped up child-care spending, but the effect of the national child-care program has been to severely distort and in many cases destroy the child-care sector by applying a discriminatory funding model that pushes child-care entrepreneurs out of the market and discourages private investment. The federal program is composed of separate agreements with the provinces, but with the child-care sector suffering crisis and widespread shortages from coast to coast, it’s reasonable to conclude Ottawa’s plan is fatally flawed.

Wherever you look, the pattern is the same—federal spending is up, but outcomes are worse. The government creates problems and does not solve them when it spends money like water. Margaret Thatcher well understood this fact. Justin Trudeau, unfortunately, evidently does not.

Author:

From the Fraser Institute

By Matthew Lau

It’s now more than four years since the federal Liberal government pledged $30 billion in spending over five years for $10-per-day national child care, and more than three years since Ontario’s Progressive Conservative government signed a $13.2 billion deal with the federal government to deliver this child-care plan.

Not surprisingly, with massive government funding came massive government control. While demand for child care has increased due to the government subsidies and lower out-of-pocket costs for parents, the plan significantly restricts how child-care centres operate (including what items participating centres may purchase), and crucially, caps the proportion of government funds available to private for-profit providers.

What have families and taxpayers got for this enormous government effort? Widespread child-care shortages across Ontario.

For example, according to the City of Ottawa, the number of children (aged 0 to 5 years) on child-care waitlists has ballooned by more than 300 per cent since 2019, there are significant disparities in affordable child-care access “with nearly half of neighbourhoods underserved, and limited access in suburban and rural areas,” and families face “significantly higher” costs for before-and-after-school care for school-age children.

In addition, Ottawa families find the system “complex and difficult to navigate” and “fewer child care options exist for children with special needs.” And while 42 per cent of surveyed parents need flexible child care (weekends, evenings, part-time care), only one per cent of child-care centres offer these flexible options. These are clearly not encouraging statistics, and show that a government-knows-best approach does not properly anticipate the diverse needs of diverse families.

Moreover, according to the Peel Region’s 2025 pre-budget submission to the federal government (essentially, a list of asks and recommendations), it “has maximized its for-profit allocation, leaving 1,460 for-profit spaces on a waitlist.” In other words, families can’t access $10-per-day child care—the central promise of the plan—because the government has capped the number of for-profit centres.

Similarly, according to Halton Region’s pre-budget submission to the provincial government, “no additional families can be supported with affordable child care” because, under current provincial rules, government funding can only be used to reduce child-care fees for families already in the program.

And according to a March 2025 Oxford County report, the municipality is experiencing a shortage of child-care staff and access challenges for low-income families and children with special needs. The report includes a grim bureaucratic predication that “provincial expansion targets do not reflect anticipated child care demand.”

Child-care access is also a problem provincewide. In Stratford, which has a population of roughly 33,000, the municipal government reports that more than 1,000 children are on a child-care waitlist. Similarly in Port Colborne (population 20,000), the city’s chief administrative officer told city council in April 2025 there were almost 500 children on daycare waitlists at the beginning of the school term. As of the end of last year, Guelph and Wellington County reportedly had a total of 2,569 full-day child-care spaces for children up to age four, versus a waitlist of 4,559 children—in other words, nearly two times as many children on a waitlist compared to the number of child-care spaces.

More examples. In Prince Edward County, population around 26,000, there are more than 400 children waitlisted for licensed daycare. In Kawartha Lakes and Haliburton County, the child-care waitlist is about 1,500 children long and the average wait time is four years. And in St. Mary’s, there are more than 600 children waitlisted for child care, but in recent years town staff have only been able to move 25 to 30 children off the wait list annually.

The numbers speak for themselves. Massive government spending and control over child care has created havoc for Ontario families and made child-care access worse. This cannot be a surprise. Quebec’s child-care system has been largely government controlled for decades, with poor results. Why would Ontario be any different? And how long will Premier Ford allow this debacle to continue before he asks the new prime minister to rethink the child-care policy of his predecessor?

Matthew Lau

Adjunct Scholar, Fraser Institute

From the Fraser Institute

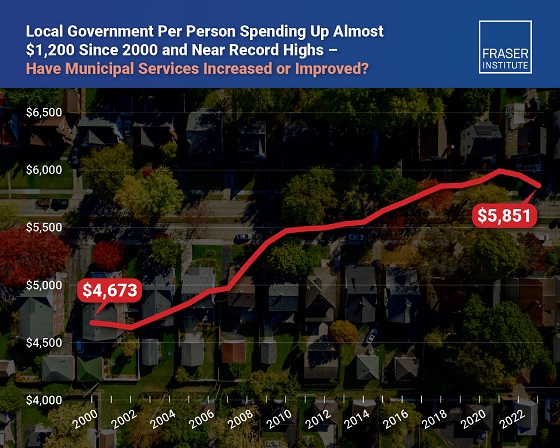

Municipal government spending in Canada hit near record levels in recent years, finds a new study by the Fraser Institute, an independent, non-partisan Canadian public policy think-tank.

“In light of record-high spending in municipalities across Canada, residents should consider whether or not crime, homelessness, public transit and other services have actually improved,” said Austin Thompson, senior policy analyst at the Fraser Institute and author of The Expanding Finances of Local Governments in Canada.

From 2000 to 2023, per-person spending (inflation-adjusted) increased by 25.2 per cent, reaching a record-high $5,974 per person in 2021 before declining slightly to $5,851 in 2023, the latest year of available data.

During that same period, municipal government revenue—generated from property taxes and transfers from other levels of government—increased by 33.7 per cent per person (inflation-adjusted).

And yet, among all three levels of government including federal and provincial, municipal government spending (adjusted for inflation) has actually experienced the slowest rate of growth over the last 10 years, underscoring the large spikes in spending at all government levels across Canada.

“Despite claims from municipal policymakers about their dire financial positions, Canadians should understand the true state of finances at city hall so they can decide whether they’re getting good value for their money,” said Jake Fuss, director of fiscal studies at the Fraser Institute.

The Expanding Finances of Local Governments in Canada, 1990–2023

- Canada’s local governments have experienced substantial fiscal growth in recent decades.

- Revenue and expenditure by local governments—including municipal governments, school boards, and Indigenous governments—have increased faster than population growth and inflation combined. From 1990 to 2023, real per-capita revenue rose by 32.7%, and expenditure by 30.0%.

- Local governments represent a significant component of Canada’s broader public sector. In 2023, net of inter-governmental transfers, municipal governments and school boards accounted for 18.6% of total government expenditure and 11.1% of revenue.

- Despite this growth, local governments’ share of overall government revenue and expenditure has declined over time—especially since the COVID-19 pandemic—as federal and provincial budgets have expanded even more rapidly.

- Nevertheless, between 2008 and 2023 the inflation-adjusted per-capita revenue of municipal governments in-creased by 10.1% and their expenditure by 12.4% , on average across the provinces.

- Over the same period, municipal governments recorded above-inflation increases in their combined annual operating surpluses, which contributed to an 88.1% inflation-adjusted rise in their net worth—raising important questions about the allocation of accumulated resources.

- In 2023, Ontario recorded the highest per-capita municipal revenue among the provinces ($4,156), while Alberta had the highest per-capita expenditure ($3,750). Prince Edward Island reported the lowest per-capita municipal revenue ($1,635) and expenditure ($1,186).

- Wide variation in per-capita municipal revenue and expenditure across the provinces reflects differences in the responsibilities provinces assign to municipalities, as well as possible disparities in the efficiency of service delivery—issues that warrant further scrutiny.

Click Here To Read The Full Study

It’s not enough to just make military commitments—we must also execute them

Alberta Next Takes A Look At Alberta Provincial Police Force

The permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

President Xi Skips Key Summit, Adding Fuel to Ebbing Power Theories

Federal government should finally cut Trudeau-era red tape

Canadian Oil Sands Production Expected to Reach All-time Highs this Year Despite Lower Oil Prices

Ontario man launches new challenge against province’s latest attempt to ban free expression on roadside billboards

-

Alberta1 day ago

Alberta1 day agoAlberta judge sides with LGBT activists, allows ‘gender transitions’ for kids to continue

-

Crime18 hours ago

Crime18 hours agoNational Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Business7 hours ago

Business7 hours agoElon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

-

Business1 day ago

Business1 day agoCanada Caves: Carney ditches digital services tax after criticism from Trump

-

Alberta1 day ago

Alberta1 day agoAlberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

-

Health18 hours ago

Health18 hours agoRFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

-

Censorship Industrial Complex6 hours ago

Censorship Industrial Complex6 hours agoGlobal media alliance colluded with foreign nations to crush free speech in America: House report

-

Crime1 day ago

Crime1 day agoSuspected ambush leaves two firefighters dead in Idaho