CBDC Central Bank Digital Currency

Don’t Gaslight Me

From the Brownstone Institute

No mention of excess mortality. No mention of the Forest of the Fallen. Nothing about the imminent WHO changes. Nothing about the dangers of Digital ID or the Misinformation Bill. Nothing about the risks of Central Bank Digital Currencies. Evidently the editor sees no “responsibility to our readers and to society in general” in respect of these issues.

An email from the editor of a major daily Melbourne newspaper has come into my possession. I won’t say how, since it might incriminate me as being part of a household that pays for a subscription. Let’s just say that it’s possible that the subscription was taken out using an email address that I have access to. Or something. The very first words of the email are:

As a subscription benefit, from today [masthead name redacted] editor [name redacted] will send you an exclusive analysis of the week’s most important stories each Friday.

That’s what I call a ‘marmalade dropper,’ a statement so utterly preposterous that to read it over breakfast would cause such a fit of apoplexy that one would choke on one’s marmalade toast and drop it on the floor, for it to be consumed by the dog.

Luckily, I’d had breakfast already. Intrigued by this alleged ‘benefit,’ which might better be regarded as a ‘threat,’ I read on. The newish editor started off by quoting a former editor:

[Masthead redacted] “does certain things differently from other newspapers simply because … we’re not there as a means of simply passing a word from a mouth to an eye, we’ve a responsibility to our readers and to society in general.”

That is an unabashed endorsement of the practice of selecting and then framing the stories they deem fit to print, rather than simply reporting the bare facts. Then this:

Readers of [masthead redacted] want more than the kind of imitable journalism they can find on countless free-to-read news sites and unoriginal, uninspiring and sometimes unhinged publications.

The editor couldn’t resist, either through spite or an inferiority complex, a swipe at other news sites. Too gutless to name those he thinks ‘unhinged.’

It goes on:

…our readers want depth and quality, excellence and rigour. They want a publication with scruples that is willing to fight for its readers, its city, and hold power to account, without fear or favour. One that will doggedly pursue public interest investigations to shine light on the darkest parts of our society, but also celebrate Melbourne’s successes and be constructive and mature in its approach to difficult subjects.

“Fight for its readers?” Did it fight for those who were shot in the back with rubber bullets when Victoria Police corralled them at the Shrine of Remembrance? “Doggedly pursue public interest investigations?” Did they doggedly pursue the hotel quarantine fiasco? As I recall it was only Peta Credlin who had the guts to ask the then Premier any hard questions about this and other Covid crimes. Did they ever get to the bottom of who ordered the curfew? Was it the Premier, the Chief Health Officer, or the Police Commissioner?

“…be constructive and mature in its approach to difficult subjects?” What a string of weasel words that is! The translation is “ignore totally any concerns about vaccine safety and smear anyone who raises the issue.”

But there’s more. The email goes on to list the things they did talk about in the last 12 months. See if you can spot what’s missing.

…war crimes of Australia’s most decorated soldier, Ben Roberts-Smith. We promoted mature discussion about the future of Melbourne and its suburbs. We broke the news that the nation’s biggest plastic bag recycling scheme was continuing to operate even though its recycling function had collapsed, resulting in millions of bags being stuffed into warehouses across the country.

We exposed huge failings in the Department of Home Affairs across a range of stories that exposed a failure to prevent human trafficking and questionable payments of Australian taxpayer money to foreign officials. When we reported that the influential head of that department, Mike Pezzullo, had attempted to influence and cosy up to politicians, he was stood down pending an investigation.

We pored over every detail of the state government’s cancellation of the Commonwealth Games and exposed the shambolic management of that decision. We sent reporters to cover a war in the Middle East with huge emotional impacts on many in Australia, and indeed on domestic politics.

We led the coverage of one of the most extraordinary murder investigations in recent history. We’ve looked at the schools we send our children to and turned our attention to the burgeoning suburbs where Melburnians are increasingly choosing to live.

We fought for our readers’ right to know what is happening within the justice system, by opposing suppression orders and battling for access to court documents in the Magistrates’, County and Supreme Courts, all the way up to the High Court of Australia.

We’ve celebrated the city’s major events. We didn’t miss a beat during one of the great AFL seasons. We took readers inside the Lord’s Long Room at one of the most controversial moments in its history and we replayed the Bairstow dismissal as frequently as we possibly could.

What great stuff. Plastic bag recycling. Australian Rules football. Cricket dismissals. Phonics in schools. A reporter sent to a war zone. A spectator at the bankruptcy of third-world Victoria, epitomised by the cancellation of the Commonwealth Games and the Airport Rail.

There’s an enormous gaping hole in the coverage, just like there’s an enormous gaping space in the foyers of office towers all over the city, as the utter destruction of our once beautiful Melbourne echoes the utter destruction of lives and livelihoods caused by mask mandates, ‘social distancing’ and vaccine mandates.

Nothing about the morality of excluding people from daily society. No mention of excess mortality. No mention of the Forest of the Fallen. Nothing about the imminent WHO changes. Nothing about the dangers of Digital ID or the Misinformation Bill. Nothing about the risks of Central Bank Digital Currencies. Evidently the editor sees no “responsibility to our readers and to society in general” in respect of these issues. I’ll be waiting for an age, I think, to get that kind of coverage.

A final quote from the email is even more chilling:

You, our subscribers, made all this and more possible by supporting our journalism. And I can assure you, this is only the start of what we believe we can accomplish as a newsroom.

So what is it that they are only at the start of accomplishing as a newsroom? What is it, other than suppressing some stories and promoting others, that they want to do?

At least I don’t pay for this stuff. Oh, wait.

Republished from the author’s Substack

Author

From LifeSiteNews

A new report released by the Bank of Canada proposed a ‘promising architecture well-suited for basic payments’ through the use of a digital dollar, though most Canadians are wary of such an idea.

Canada’s central bank has been studying ways to introduce a central bank digital currency (CBDC) for use for online retailers, according to a new report, despite the fact that recent research suggests Canadians are wary of any type of digital dollar.

In a new 47-page report titled, “A Retail CBDC Design For Basic Payments Feasibility Study,” which was released on June 13, 2025, the Bank of Canada (BOC) identified a “promising architecture well-suited for basic payments” through the use of a digital dollar.

The report reads that CBDCs “can be fast and cheap for basic payments, with high privacy, although some areas such as integration with retail payments systems, performance of auditing and resilience of the core system state require further investigation.”

While the report authors stopped short of fully recommending a CBDC, they noted it is a decision that could happen “outside the scope of this analysis.”

“Our framing highlights other promising architectures for an online retail CBDC, whose analysis we leave as an area for further exploration,” reads the report.

When it comes to a digital Canadian dollar, the Bank of Canada last year found that Canadians are very wary of a government-backed digital currency, concluding that a “significant number” of citizens would resist the implementation of such a system.

Indeed, a 2023 study found that most Canadians, about 85 percent, do not want a digital dollar, as previously reported by LifeSiteNews.

The study found that a “significant number” of Canadians are suspicious of government overreach and would resist any measures by the government or central bank to create digital forms of official money.

The BOC has said that it would continue to look at other countries’ use and development of CBDCs and will work with other “central banks” to improve so-called cross border payments.

Last year, as reported by LifeSiteNews, the BOC has already said that plans to create a digital “dollar,” also known as a central bank digital currency (CBDC), have been shelved.

Digital currencies have been touted as the future by some government officials, but, as LifeSiteNews has reported before, many experts warn that such technology would restrict freedom and could be used as a “control tool” against citizens, similar to China’s pervasive social credit system.

The BOC last August admitted that the creation of a CBDC is not even necessary, as many people rely on cash to pay for things. The bank concluded that the introduction of a digital currency would only be feasible if consumers demanded its release.

Conservative Party leader Pierre Poilievre has promised, should he ever form the government, he would oppose the creation of a digital dollar.

Contrast this to Canada’s current Liberal Prime Minister Mark Carney. He has a history of supporting central bank digital currencies and in 2022 supported “choking off the money” donated to the Freedom Convoy protests against COVID mandates.

From LifeSiteNews

By

“central bank digital currency could hand incredible power to the Government and Bank of Canada to monitor financial transactions, punish whatever behaviours the government deems undesirable, and penalize those on the wrong side of government ambitions”

The Justice Centre for Constitutional Freedoms released a new report examining how the adoption of a central bank digital currency in Canada could undermine the rights and freedoms of Canadians, including their privacy, autonomy, security, equality, and access to economic participation.

Financial transactions are increasingly conducted digitally. In 2023, a mere 11 percent of transactions were conducted with cash, according to Payments Canada.

This trend is not limited to individual consumers. Government entities, including government departments, agencies, and Crown Corporations, have rapidly digitized access to, and delivery of, their goods and services over the past decade.

READ: Mark Carney has history of supporting CBDCs, endorsed Freedom Convoy crackdown

Against this backdrop, in 2017, the Bank of Canada (a Crown Corporation) began exploring the possibility of implementing its own government-issued and government-controlled cashless currency – a central bank digital currency (CBDC).

In a 2023 Bank of Canada survey on CBDCs, however, 82 percent of 89,423 respondents strongly disagreed that the Bank of Canada should be researching or building the capability to issue a CBDC. Despite these results, the Bank of Canada continues to research a CBDC for Canada.

The Justice Centre’s report critically evaluates the impact a CBDC could have on Canadians’ fundamental rights and freedoms. Absent robust legislative protections and oversight, a CBDC could allow the Government and Bank of Canada to monitor Canadians’ purchases, donations, investments and other financial transactions.

A CBDC has the potential to empower government to reward and punish the behaviours and lifestyle choices of individual Canadians, as Communist China does with its “social credit” system. Allowing the government to peer into and influence Canadians’ purchasing behaviours could have a profoundly damaging impact on their privacy and autonomy, cautions the report.

READ: Financial expert warns all-digital monetary system would enable ‘complete control’ of citizens

Canada is not the first jurisdiction to explore a CBDC. This report evaluates the Bank of Canada’s exploration within a global context, applying lessons learned from jurisdictions like Nigeria, the Caribbean, and others.

After analyzing negative outcomes of “going cashless” in jurisdictions such as Australia, Sweden, Finland, and Norway, this report advocates for the value of cash and the need for robust institutional and legislative protections for the use of cash.

Ben Klassen, Education Programs Coordinator at the Justice Centre and lead author of the report, stated, “Many Canadian politicians and policy designers would have us participate in a frantic (and global) race to digitize goods and services, including our dollar. The finish line, we are told, promises heightened profitability, convenience, and security. While the pursuit of innovation and efficiency can deliver worthwhile rewards, we must always remember the values of privacy, autonomy, security, equality, and access to economic participation. Adopting a central bank digital currency risks excluding the homeless, the elderly, the ‘internetless,’ the technologically illiterate, and the conscientious objector.”

“Most seriously, a central bank digital currency could hand incredible power to the Government and Bank of Canada to monitor financial transactions, punish whatever behaviours the government deems undesirable, and penalize those on the wrong side of government ambitions,” continued Mr. Klassen. “This issue should be framed as a contrast between a ‘digital dollar’ and a ‘human dollar’ – our currency cannot be designed without regard for the humans and human values that will be profoundly impacted by its design.”

READ: RFK Jr. warns Americans ‘will be slaves’ if central bank digital currency is established

This report was produced in collaboration with Sharon Polsky – President of AMINAcorp.ca, President of the Privacy & Access Council of Canada, and a Privacy by Design Ambassador with more than 30 years’ experience in advising governments and policy designers on privacy and access matters.

Reprinted with permission from the Justice Centre for Constitutional Freedoms.

So Alberta, what’s next?

Alberta Next Takes A Look At Alberta Provincial Police Force

The permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

President Xi Skips Key Summit, Adding Fuel to Ebbing Power Theories

It’s not enough to just make military commitments—we must also execute them

NATO commits to 5% defense floor after Trump pushes allies to step up

Federal government should finally cut Trudeau-era red tape

-

Alberta1 day ago

Alberta1 day agoAlberta judge sides with LGBT activists, allows ‘gender transitions’ for kids to continue

-

Health14 hours ago

Health14 hours agoRFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

-

Business3 hours ago

Business3 hours agoElon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

-

Business1 day ago

Business1 day agoCanada Caves: Carney ditches digital services tax after criticism from Trump

-

Crime1 day ago

Crime1 day agoSuspected ambush leaves two firefighters dead in Idaho

-

Alberta1 day ago

Alberta1 day agoAlberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

-

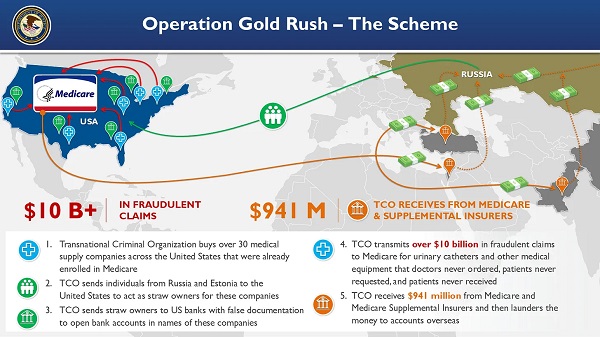

Crime14 hours ago

Crime14 hours agoNational Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Censorship Industrial Complex2 hours ago

Censorship Industrial Complex2 hours agoGlobal media alliance colluded with foreign nations to crush free speech in America: House report