Opinion

Canada’s Financial Freefall: When Rosy Rhetoric Meets Hard Reality

|

|

|

|

This article is from The Opposition With Dan Knight substack.

The Trudeau Government’s Economic Alchemy: Turning Gold Hopes Into Lead Numbers

Good morning, my fellow Canadians. It’s September 3, 2023, and if you’re expecting to wake up to a bright, financially secure Canada, well, I have some sobering news for you. The latest figures from Statistics Canada are in, and they confirm what many of us have suspected: the Canadian economy is not on the up-and-up. Despite the rosy pictures painted by Prime Minister Justin Trudeau and Finance Minster Chrystia Freeland, the real numbers don’t lie, and they point to an economic landscape in turmoil. Allow me to break it down for you.

The new Statistics Canada data is in, and it paints a rather bleak picture of the Canadian economy under the watchful eyes of the federal government and Justin Trudeau. Let’s delve into some numbers, shall we? A staggering $16.5 billion in debt was added by Canadian households in the first quarter of this year alone, with $11.2 billion being in mortgage debt. In an environment of 5% interest rates, a rate we haven’t seen for over a decade, this is a financial bomb waiting to explode.

And let’s not forget inflation. Since 2021, we’ve seen a cumulative inflation rate of around 16.5%. Now, remember, these aren’t just abstract numbers on a ledger somewhere; these are realities hitting your grocery bills, your gas prices, your rents, and slowly emptying your wallets. But it’s not just households feeling the pinch. The economy as a whole is stalling, with real GDP nearly unchanged in the second quarter of 2023, following a measly 0.6% rise in the first quarter.

Amidst all this, Justin Trudeau and the federal government seem content piling on debt like there’s no tomorrow. The Parliamentary Budget Officer’s March 2023 report shows Canada’s deficit is expected to rise to $43.1 billion in 2023-24, up from $36.5 billion in 2022-23. And let’s not forget that 1 out of every 5 dollars in this debt spree didn’t even exist pre-pandemic. Essentially, we’re spending money we don’t have, to solve problems we’re not solving, all while making new ones.

So, where has all this spending gone? Not into securing a robust future for Canadians, I can tell you that. Despite the monumental deficits and the reckless spending, housing investment fell 2.1% in the second quarter,marking its fifth consecutive quarterly decrease. Canadians are struggling to make ends meet, and the government’s financial imprudence is exacerbating, not alleviating, the situation.

But here’s a twist to the story: while investments in housing decline, Justin Trudeau decided it was prime time to open the floodgates of immigration. There’s an aspect of governance called planning, something that seems foreign to this administration. How does one justify allowing over a million immigrants into Canada without even hinting at a solution for housing them? The result is basic economics – demand outstrips supply, and prices soar.

Remember the days before Trudeau’s reign, when the average home in Canada cost around $400,000? Eight years under his watch and that figure has doubled. Trudeau’s policies seem like a cruel jest to young families, professionals, and, frankly, anyone aspiring to own a piece of the Canadian dream. It’s almost as if he expected the housing market to “balance itself”.

And before you think this is just a ‘rough patch,’ let me remind you that household spending is also slowing. So not only are Canadians going into debt, but they’re also cutting back on spending. They’re being hit from both sides, and there’s no end in sight. The government’s promises of prosperity seem increasingly hollow when we see that per capita household spending has declined in three of the last four quarters.

The Trudeau administration’s approach to governing appears to be in a parallel universe, one where debt is limitless, and financial responsibilities are for the next government or even the next generation to sort out. And don’t even get me started on the higher taxes lurking around the corner to pay off this bonanza of spending. This isn’t governance; it’s financial negligence.

When Canadians were told that this level of inflationary spending could turn our country into something akin to Venezuela, many scoffed at the idea. But let’s face it: the signs are becoming hard to ignore. The truth is, many Canadians have been led to believe they can have gold-plated social services without paying an ounce of gold in taxes. Prime Minister Justin Trudeau seemed more than happy to sell that narrative. He promised a utopia, a social safety net woven from dreams and aspirations. But what has that net caught? Rising costs, crippling debt, and a harder life for everyday Canadians.

Trudeau has turned out to be less a responsible steward of the economy and more of a Pied Piper, leading us all off a fiscal cliff while playing a cheerful tune. Or perhaps he’s more like the Cheshire Cat from “Alice in Wonderland,” grinning broadly as he disappears, leaving behind only his grin and a trail of false promises.

As we approach the pivotal year of 2025, don’t forget who sold you this bill of goods. Remember the skyrocketing costs of living, the unmanageable debt, and the empty words that were supposed to make everything better. I, for one, certainly won’t forget. And I suspect, come election time, neither will you.

Click here to see more from The Opposition with Dan Knight.

For the full experience, upgrade your subscription.

Peter Doocy asked directly, “What happened to the Epstein client list that the Attorney General said she had on her desk?” Here’s how Leavitt tried to explain it.

The Epstein client list was supposed to be SITTING on Pam Bondi’s desk for review.

But months later, the DOJ says no such list even exists.

Karoline Leavitt was just asked why there was such a reversal in so little time.

Her responses today are raising eyebrows.

On February 21st, Pam Bondi told the world the Epstein client list was “sitting on [her] desk right now to review,” explaining it was part of a directive ordered by President Trump.

Shortly afterward, she and Kash Patel pledged to end the Epstein cover-up, promising to fully disclose the Epstein files to the public, hold accountable any government officials who withheld key evidence, and investigate why critical documents had been hidden in the first place.

But ever since late February, it seems the cover-up wasn’t exposed but buried even deeper by those who promised transparency.

First, they handed out the so-called “Epstein files” to influencers like golden Willy Wanka tickets, only for everyone to discover that almost all of the contents inside were already public and contained no new revelations.

Fast-forward to May, and suddenly Kash Patel and Dan Bongino are declaring firmly that Epstein killed himself.

“I’ve seen the whole file. He killed himself,” Bongino stated bluntly to Fox News’s Maria Bartiromo.

Today, the Trump-appointed DOJ and FBI released a new report that’s turning heads and raising plenty of questions.

They concluded that Epstein had no clients, didn’t blackmail anyone, and definitely killed himself.

FBI Concludes Epstein Had No Clients, Didn’t Blackmail Anyone, and Definitely Killed Himself

This article originally appeared on Infowars and was republished with permission.

They also released surveillance footage and claimed it showed no one entered Epstein’s cell area, supporting the suicide ruling.

But people aren’t convinced. Some allege the video cuts off, with a minute of footage missing between 11:59 PM and midnight.

Monday, White House Press Secretary Karoline Leavitt responded to questions about the Epstein client list in light of these new DOJ and FBI statements.

A reporter asked, “Karoline, the DOJ and FBI have now concluded there was no Jeffrey Epstein client list. What do you tell MAGA supporters who say they want anyone involved in Epstein’s alleged crimes held accountable?”

Leavitt replied, “This administration wants anyone who has ever committed a crime to be accountable, and I would argue this administration has done more to lock up bad guys than certainly the previous administration.”

She continued, “The Trump administration is committed to truth and transparency. That’s why the Attorney General and the FBI Director pledged, at the president’s direction, to do an exhaustive review of all the files related to Jeffrey Epstein’s crimes and his death. They put out a memo in conclusion of that review.”

“There was material they did not release because frankly it was incredibly graphic and contained child pornography, which is not something that is appropriate for public consumption,” she added.

“But they committed to an exhaustive investigation. That’s what they did and they provided the results of that.”

“That’s transparency,” Leavitt said.

Leavitt was also pressed about Attorney General Pam Bondi’s comments in February when she claimed she had the Epstein list “on [her] desk.”

Peter Doocy asked, “Okay, so the FBI looks at the circumstances surrounding the death of Jeffrey Epstein. According to the report, this systematic review revealed no incriminating client list. So what happened to the Epstein client list that the Attorney General said she had on her desk?”

Leavitt responded, “I think if you go back and look at what the Attorney General said in that interview, which was on your network, on Fox News—”

Doocy pushed back, “I have the quote. John Roberts said: ‘DOJ may release the list of Jeffrey Epstein’s clients, will that really happen?’ And she said, ‘It’s sitting on my desk right now to review.’”

Leavitt explained, “Yes. She was saying the entirety of all of the paperwork, all of the paper in relation to Jeffrey Epstein’s crimes, that’s what the Attorney General was referring to. And I will let her speak for that.”

“But when it comes to the FBI and the Department of Justice, they are more than committed to ensuring that bad people are put behind bars.”

So, after months of patiently waiting, the American people get a nothing burger that simply repeats the same old claims we heard under Bill Barr.

Even worse, it’s purported that this is what “transparency” and “accountability” look like.

The story went from saying the Epstein client list was “on my desk” to “actually, there is no client list.”

And the newly released video footage raises questions and, in the age of AI, proves nothing.

If there’s really nothing to hide, why does it still feel like they’re hiding everything?

And most importantly—who’s still being protected?

Thanks for reading to the end. I hope you found this timeline of events and recap helpful.

Subscribe to The Vigilant Fox

This past week has seen (some) Canadians celebrating their heritage— now that Mike Myers has officially reinterpreted Canadian culture as a hockey sweater and Mr. Dressup. This quick-change was so popular that Canadian voters even forgot an entire decade of Justin Trudeau.

In the United States, the people who elected Donald Trump– and not Andrew Coyne– to run their nation celebrated Independence Day with stirring renditions off The Star Spangled Banner, although few could surpass the brilliant performance of the song by the late Whitney Houston at the 1991 Super Bowl.

The CDN equivalent is some flavour of the month changing the words to O Canada at the Grey Cup game. Canada’s national anthem has always been open to interpretation by people who may or may not have Canada in their hearts. At the 2023 NBA All Star Game Canadian chanteuse Jully Black became the latest singer to attempt a manicure to the English lyrics of O Canada, penned for the 1880 Saint-Jean-Baptiste Day ceremony ( Calixa Lavallée composed the music, after which words were written by the poet and judge Sir Adolphe-Basile Routhier. The English lyrics have “evolved” over the years, just like the dress code for the CDN PM..)

Black amended the first line from “our home and native land” to our home ON native land”. Because something-something. But this creative license is nothing new. Unlike Chris Stapleton, Marvin Gaye or Whitney Houston with the Star Spangled Banner, interpreters of O Canada have seen fit to amend the lyrics to their sensibilities. Roger Doucet, famed anthem singer of the Montreal Canadiens in the 1970-80s, tried to add the words “we stand on guard for truth and liberty” in place of the first “we stand on guard for thee”.

In 1990, having nothing better to do, Toronto City Council voted 12 to 7 in favour of recommending that the phrase “our home and native land” be changed to “our home and cherished land” and that “in all thy sons command” be partly reverted to “in all of us command”. (The latter was officially adapted.)

While those attempts had mixed outcomes it appears it’s just a matter of time till Ms. Black’s class-conscious culling of the words is accepted. Being generous we here at IDLM thought we’d short-circuit piecemeal attempts to create a throughly Woke version of the anthem that would last till the latest fad come along. Herewith our 2023 definitive O Canada that even— maybe only— Justin Trudeau could love:

“O Canada” (Ignores the French fact in our culture) Change to “Eau Canada”

“Our home on native land” (ignores indigenous land claims) Change to “Get off our land, settlers”

“True patriot love in all of us commands” (Only true patriot love? There were officially 78 kinds of relationships in Trudeaupia. And commanding love?) Change to “Love the one you’re with”.

“With glowing hearts we see thee rise” (rise suggests triumph of white triumphalist dogma) Change to “Non judgementally we oppose the crushing impacts of Euro-based autocracy”

“The true north strong and free” (How can anyone be strong or free when we support America’s killing fields?) Change to “Heteronormative thinking must be stamped out at our borders. If we even have borders anymore.”

“From far and wide” (Body shaming) Change to “Obesity is a disease that is not helped by putting it in the national anthem.”

“O Canada” (biased against A, B, AB blood types) change to “Science Must Be Believed”

“We stand on guard for thee” (Spreads hate against the non ableist community) Change to “Please remain seated.”

“God keep our land” (God? God? What is this, the Reformation) “Change to “It’s your thing”

”Glorious and free” (Glorious harkens to the bourgeois subjugation of Indigenous thought processes by white Christian priests) Change to “A genocidal state if there ever was one”.

“O Canada we stand on guard for thee/

O Canada we stand on guard for thee” The denial of trans rights is used twice here to emphasize the intolerable burdens faced by people of the LGBTQ2R community as they seek respect and compensation for the evils of the founding oppressors.) Change to “Eau Canada, after 6.5 hours of intensive lectures on the gender, race and dissociative application of class war on your citizens you may someday come to understand that this song is a manifestation of your bigotry and exploitation of minorities— and why rhyming lines like “thee and free” is the work of the devil or J.K. Rowling, whomever comes to mind first.”

There. That wasn’t so tough, was it? Flows trippingly off the tongue like Mark Carney refusing a special inquiry into China buying the electoral process. Or perhaps we should simply accept a literal translation of the original French lyrics:

“O Canada!

Land of our ancestors

Glorious deeds circle your brow

For your arm knows how to wield the sword

Your arm knows how to carry the cross;

Your history is an epic

Of brilliant deeds

And your valour steeped in faith

Will protect our homes and our rights.”

Yikes. That’s downright fascistic. But it’s Quebec, and we have to allow them their peccadilloes. So circle your brow with glorious deeds, grab a cross and a sword and valour steeped in faith. And remember we must be adaptable in the new era.

Unless it’s Alberta using the adapting to fuel its CO2-belching machines. In which case it’s man the battlements and follow Mike Myers into the fight.

Bruce Dowbiggin @dowbboy is the editor of Not The Public Broadcaster A two-time winner of the Gemini Award as Canada’s top television sports broadcaster, his new book Deal With It: The Trades That Stunned The NHL And Changed hockey is now available on Amazon. Inexact Science: The Six Most Compelling Draft Years In NHL History, his previous book with his son Evan, was voted the seventh-best professional hockey book of all time by bookauthority.org . His 2004 book Money Players was voted sixth best on the same list, and is available via brucedowbigginbooks.ca.

Elon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

RFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

CBS settles with Trump over doctored 60 Minutes Harris interview

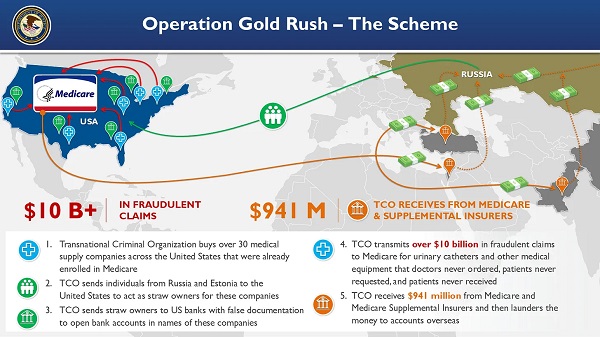

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

Alberta Provincial Police – New chief of Independent Agency Police Service

-

Carbon Tax2 days ago

Carbon Tax2 days agoCanada’s Carbon Tax Is A Disaster For Our Economy And Oil Industry

-

Disaster2 days ago

Disaster2 days agoTexas flood kills 43 including children at Christian camp

-

Alberta22 hours ago

Alberta22 hours agoAlberta Next: Immigration

-

Daily Caller2 days ago

Daily Caller2 days agoTrump’s One Big Beautiful Bill Resets The Energy Policy Playing Field

-

Business1 day ago

Business1 day agoThe Digital Services Tax Q&A: “It was going to be complicated and messy”

-

International1 day ago

International1 day agoElon Musk forms America Party after split with Trump

-

Crime10 hours ago

Crime10 hours agoNews Jeffrey Epstein did not have a client list, nor did he kill himself, Trump DOJ, FBI claim

-

COVID-198 hours ago

COVID-198 hours agoFDA requires new warning on mRNA COVID shots due to heart damage in young men