Business

Spending sprees by governments across Canada help fuel inflation and high interest rates

From the Fraser Institute

By Jake Fuss and Grady Munro

While the prime minister and many premiers justified their high spending levels during the pandemic as merely a temporary development, the federal government and seven provincial governments still plan to run budget deficits this year

Earlier this year, premiers in Ontario, British Columbia, and Newfoundland and Labrador wrote letters to Tiff Macklem, Governor of the Bank of Canada, cautioning against further interest rate hikes, citing the potential negative effects on residents including homeowners with mortgages. But instead of blaming the central bank, Canadian premiers—and the prime minister—should stop their spending sprees, which help fuel inflation and increase interest rates.

Indeed, when governments increase spending, particularly when financed by debt, they add more money to the economy and can help fuel inflation. And high rates of government spending put pressure on the Bank of Canada to maintain interest rates at current levels, or even hike the rate further, to counteract inflation. According to a recent report from Scotiabank, government spending has contributed significantly to higher interest rates in Canada, accounting for an estimated 42 per cent of the increase in the Bank of Canada’s rate since the first quarter of 2022.

Yet the spending sprees continue.

While the prime minister and many premiers justified their high spending levels during the pandemic as merely a temporary development, the federal government and seven provincial governments still plan to run budget deficits this year. Government spending across the country remains at elevated levels or, in some cases, even increased beyond pandemic levels.

Ontario is a prime example. Provincial program spending (total spending minus interest costs) will reach an estimated $193.0 billion in 2023/24—$24.0 billion more than at the peak of COVID. Debt interest costs have also grown due to debt accumulation and rising interest rates.

Despite a considerable increase in revenue over recent years, the Ford government had planned for a $1.3 billion deficit in its spring budget. By November, the government increased spending again and quadrupled the projected deficit to $5.6 billion.

Similarly, British Columbia outlined plans in February to increase program spending and run a $4.2 billion deficit while adding $13.1 billion in debt to the books this year. Just over a half-year later, the B.C. government increased spending again and the deficit was revised to $5.6 billion with debt rising by $14.0 billion instead of $13.1 billion.

Prime Minister Trudeau and his government followed a similar path. According to the recent federal fiscal update, between 2024/25 and 2027/28, the government has increased projected spending by $30.7 billion more than previously forecasted.

According to projections, only two provinces (Alberta and New Brunswick) will run budget surpluses this year, but in Alberta this is largely due to elevated resource revenues stemming from high commodity prices rather than any significant spending restraint. If resource revenues declined to historical average levels, the Smith government in Alberta would likely run deficits similar to other provinces.

Simply put, the excessive spending habits of many premiers and the prime minister are a big reason why interest rates have climbed and inflation remains sticky.

If Canadian politicians want to help tame inflation and bring down interest rates, they should look in the mirror for solutions and show leadership. Complaining about elevated interest rates helps no one, but ensuring fiscal policy is rowing in the same direction as monetary policy would be a good start.

Authors:

Business

Federal funds FROZEN after massive fraud uncovered: Trump cuts off Minnesota child care money

The Trump administration has cut off all federal child care payments to Minnesota, ordering a sweeping audit of the state’s day care system as investigators dig into what officials describe as one of the largest fraud schemes ever tied to social service programs.

“We have frozen all child care payments to the state of Minnesota,” Deputy Health and Human Services Secretary Jim O’Neill wrote Tuesday afternoon, saying the move comes after mounting evidence that taxpayer dollars were being siphoned to sham or non-operational day care centers. The freeze follows a viral investigative video that put a national spotlight on facilities across Minneapolis that were receiving large sums of public money despite appearing closed or barely functioning.

According to Alex Adams, assistant secretary at HHS’s Administration for Children and Families, Minnesota has already received roughly $185 million in federal child care funding this year alone. Those funds, the administration says, will remain locked down until the state can demonstrate that payments are being used lawfully. “Funds will be released only when states prove they are being spent legitimately,” Adams said.

We have frozen all child care payments to the state of Minnesota.

You have probably read the serious allegations that the state of Minnesota has funneled millions of taxpayer dollars to fraudulent daycares across Minnesota over the past decade.

Today we have taken three actions… pic.twitter.com/VYbyf3WGop

— Deputy Secretary Jim O'Neill (@HHS_Jim) December 30, 2025

O’Neill accused Minnesota officials of allowing abuse to fester for years, alleging the state has “funneled millions of taxpayer dollars to fraudulent daycares across Minnesota over the past decade.” To halt further losses, HHS outlined a series of immediate enforcement steps. Going forward, states seeking reimbursement through the Administration for Children and Families will be required to provide receipts or photographic proof documenting how funds are spent.

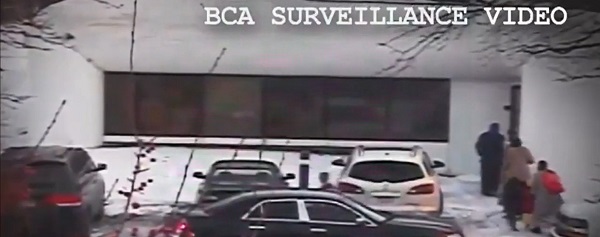

The department has also formally demanded that Gov. Tim Walz order a “comprehensive audit” of the day care centers flagged by investigators. O’Neill said the review must include attendance records, licensing documents, complaints, investigative files, and inspection reports. He pointed directly to a video published Friday by YouTuber Nick Shirley, who visited multiple Minneapolis-area centers listed as receiving millions in public funds but found locations that appeared closed or inactive.

In addition, HHS has launched a dedicated fraud hotline and email address at childcare.gov to encourage tips from parents, providers, and the public. “We have turned off the money spigot and we are finding the fraud,” O’Neill said, urging anyone with information to come forward.

Federal prosecutors say the scope of the alleged abuse is staggering. Authorities have already confirmed at least $1 billion in fraud tied to Minnesota child care programs, with 92 people charged so far. The U.S. Attorney’s Office has warned the total could ultimately reach as high as $9 billion as investigators continue combing through records.

The funding freeze marks one of the most aggressive crackdowns yet by the Trump administration on state-run social programs accused of lax oversight, sending a clear message that federal dollars will not flow until Minnesota can account for where the money went — and who was cashing in.

From the Frontier Centre for Public Policy

By Conrad Eder

Conrad Eder supports universal health care, but not Canada’s broken version. Despite massive spending, Canadians face brutal wait times. He argues it’s time to allow private options, as other countries do, without abandoning universality.

It’s not about money. It’s about the rules shaping how Canada’s health care system works

Canada’s health care system isn’t failing because it lacks funding or public support. It’s failing because governments have tied it to restrictive rules that block private medical options used in other developed countries to deliver timely care.

Canada spends close to $400 billion a year on health care, placing it among the highest-spending countries in the Organization for Economic Co-operation and Development (OECD). Yet the system continues to struggle with some of the longest waits for care, the fewest doctors per capita and among the lowest numbers of hospital beds in the OECD. This is despite decades of spending increases, including growth of 4.5 per cent in 2023 and 5.7 per cent in 2024, according to estimates from the Canadian Institute for Health Information.

Canadians are losing confidence that government spending is the solution. In fact, many don’t even think it’s making a difference.

And who could blame them? Median health care wait times reached 30 weeks in 2024, up from 27.7 weeks in 2023, which was up from 27.4 weeks in 2022, according to annual surveys by the Fraser Institute.

Nevertheless, politicians continue to tout our universal health care system as a source of national pride and, according to national surveys, 74 per cent of Canadians agree. Yet only 56 per cent are satisfied with it. This gap reveals that while Canadians value universal health care in principle, they are frustrated with it in practice.

But it isn’t universal health care that’s the problem; it’s Canada’s uniquely restrictive version of it. In most provinces, laws restrict physicians from working simultaneously in public and private systems and prohibit private insurance for medically necessary services covered by medicare, constraints that do not exist in most other universal health care systems.

The United Kingdom, France, Germany and the Netherlands all maintain universal health care systems. Like Canada, they guarantee comprehensive insurance coverage for essential health care services. Yet they achieve better access to care than Canada, with patients seeing doctors sooner and benefiting from shorter surgical wait times.

In Germany, there are both public and private hospitals. In France, universal insurance covers procedures whether patients receive them in public hospitals or private clinics. In the Netherlands, all health insurance is private, with companies competing for customers while coverage remains guaranteed. In the United Kingdom, doctors working in public hospitals are allowed to maintain private practices.

All of these countries preserved their commitment to universal health care while allowing private alternatives to expand choice, absorb demand and deliver better access to care for everyone.

Only 26 per cent of Canadians can get same-day or next-day appointments with their family doctor, compared to 54 per cent of Dutch and 47 per cent of English patients. When specialist care is needed, 61 per cent of Canadians wait more than a month, compared to 25 per cent of Germans. For elective surgery, 90 per cent of French patients undergo procedures within four months, compared to 62 per cent of Canadians.

If other nations can deliver timely access to care while preserving universal coverage, so can Canada. Two changes, inspired by our peers, would preserve universal coverage and improve access for all.

First, allow physicians to provide services to patients in both public and private settings. This flexibility incentivizes doctors to maximize the time they spend providing patient care, expanding service capacity and reducing wait times for all patients. Those in the public system benefit from increased physician availability, as private options absorb demand that would otherwise strain public resources.

Second, permit private insurance for medically necessary services. This would allow Canadians to obtain coverage for private medical services, giving patients an affordable way to access health care options that best suit their needs. Private insurance would enable Canadians to customize their health coverage, empowering patients and supporting a more responsive health care system.

These proposals may seem radical to Canadians. They are not. They are standard practice everywhere else. And across the OECD, they coexist with universal health care. They can do the same in Canada.

Alberta has taken an important first step by allowing some physicians to work simultaneously in public and private settings through its new dual-practice model. More Canadian provinces should follow Alberta’s lead and go one step further by removing legislative barriers that prohibit private health insurance for medically necessary services. Private insurance is the natural complement to dual practice, transforming private health care from an exclusive luxury into a viable option for Canadian families.

Canadians take pride in their health care system. That pride should inspire reform, not prevent it. Canada’s health care crisis is real. It’s a crisis of self-imposed constraints preventing our universal system from functioning at the level Canadians deserve.

Policymakers can, and should, preserve universal health care in this country. But maintaining it will require a willingness to learn from those who have built systems that deliver universality and timely access to care, something Canada’s current system does not.

Conrad Eder is a policy analyst at the Frontier Centre for Public Policy.

Remembering Afghanistan and the sacrifices of our military families

“Magnitude cannot be overstated”: Minnesota aid scam may reach $9 billion

Largest fraud in US history? Independent Journalist visits numerous daycare centres with no children, revealing massive scam

US Under Secretary of State Slams UK and EU Over Online Speech Regulation, Announces Release of Files on Past Censorship Efforts

US Halts Construction of Five Offshore Wind Projects Due To National Security

Sweden Fixed What Canada Won’t Even Name

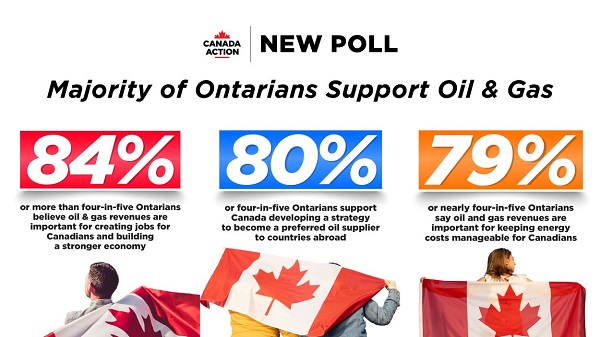

New Poll Shows Ontarians See Oil & Gas as Key to Jobs, Economy, and Trade

-

Alberta1 day ago

Alberta1 day agoThe Canadian Energy Centre’s biggest stories of 2025

-

Business1 day ago

Business1 day agoResurfaced Video Shows How Somali Scammers Used Day Care Centers To Scam State

-

Bruce Dowbiggin2 days ago

Bruce Dowbiggin2 days agoIn Contentious Canada Reality Is Still Six Degrees Of Hockey

-

Business13 hours ago

Business13 hours agoDark clouds loom over Canada’s economy in 2026

-

Business2 days ago

Business2 days agoDOOR TO DOOR: Feds descend on Minneapolis day cares tied to massive fraud

-

Addictions9 hours ago

Addictions9 hours agoCoffee, Nicotine, and the Politics of Acceptable Addiction

-

Business2 days ago

Business2 days agoCanada needs serious tax cuts in 2026

-

Business1 day ago

Business1 day agoOttawa Is Still Dodging The China Interference Threat