Business

Solar and wind power make electricity more expensive—that’s a fact

From the Fraser Institute

By Julio Mejía and Elmira Aliakbari

As a new year dawns and winter takes hold, it’s worth considering the cost of energy. After a meeting in Italy last spring, the G7 countries (including Canada) pledged to triple renewable energy sources (e.g. wind, solar) globally to ensure an “affordable” energy future. But while direct costs for wind and solar are dropping, they remain expensive due in part to the backup energy sources required when renewables are not available.

In short, an “affordable” energy future is incompatible with increased reliance on renewables. Here’s why.

Wind and solar energy are intermittent, meaning they aren’t consistently available, so we need an alternative power source when there’s no sunlight or wind given the current limited ability to store energy from solar and wind. So we must maintain enough energy capacity in a parallel system, typically powered by natural gas. Constructing and upkeeping a secondary energy source results in higher overall energy costs because two energy systems cost more than one. Therefore, when evaluating the costs of renewables, we must consider the costs of backup energy.

Often, when proponents claim that wind and solar sources are cheaper than fossil fuels, they ignore these costs. A recent study published in Energy, a peer-reviewed energy and engineering journal, found that—after accounting for backup, energy storage and associated indirect costs—solar power costs skyrocket from US$36 per megawatt hour (MWh) to as high as US$1,548 and wind generation costs increase from US$40 to up to US$504 per MWh.

Which is why when governments phase out fossil fuels to expand the role of renewable sources in the electricity grid, electricity become more expensive. In fact, a study by University of Chicago economists showed that between 1990 and 2015, U.S. states that mandated minimum renewable power sources experienced significant electricity price increases after accounting for backup infrastructure and other costs. Specifically, in those states electricity prices increased by an average of 11 per cent, costing consumers an additional $30 billion annually. The study also found that electricity prices grew more expensive over time, and by the twelfth year, electricity prices were 17 per cent higher (on average).

Europe is another case in point. Between 2006 and 2019, solar and wind sources went from representing around 5 per cent of Germany’s electricity generation to almost 30 per cent in 2019. During that same period, German households experienced an increase in electricity prices from 19.46 cents to 30.46 cents per kilowatt hour—a rise of more than 56 per cent. This surge in prices occurred before the war in Ukraine, which led to an unprecedented price spike in 2022.

For Canada, the outlook is also dire. In a recent report, TD Bank estimated that replacing existing gas generators with renewables (such as solar and wind) in Ontario could increase average electricity costs by 20 per cent by 2035 compared to 2021. In Alberta, electricity prices would increase by up to 66 per cent by 2035 compared to an scenario without changes. These increases are on top of the 15 to 20 per cent increase in average generation costs expected by 2035 under current government policies.

Clearly, when accounting for backup costs, renewable-powered electricity is more expensive than fossil fuels. Policymakers in Ottawa and across Canada must recognize that integrating renewables into electricity grids can lead to significant price increases for consumers, and they should be honest about that fact with Canadians in 2025 and beyond.

Julio Mejía

Policy Analyst

Elmira Aliakbari

![]()

People criticize capitalism. A recent Axios-Generation poll says, “College students prefer socialism to capitalism.”

Why?

Because they believe absurd myths. Like the claim that the Soviet Union “wasn’t real socialism.”

Socialism guru Noam Chomsky tells students that. He says the Soviet Union “was about as remote from socialism as you could imagine.”

Give me a break.

The Soviets made private business illegal.

If that’s not socialism, I’m not sure what is.

“Socialism means abolishing private property and … replacing it with some form of collective ownership,” explains economist Ben Powell. “The Soviet Union had an abundance of that.”

Socialism always fails. Look at Venezuela, the richest country in Latin America about 40 years ago. Now people there face food shortages, poverty, misery and election outcomes the regime ignores.

But Al Jazeera claims Venezuela’s failure has “little to do with socialism, and a lot to do with poor governance … economic policies have failed to adjust to reality.”

“That’s the nature of socialism!” exclaims Powell. “Economic policies fail to adjust to reality. Economic reality evolves every day. Millions of decentralized entrepreneurs and consumers make fine tuning adjustments.”

Political leaders can’t keep up with that.

Still, pundits and politicians tell people, socialism does work — in Scandinavia.

“Mad Money’s Jim Cramer calls Norway “as socialist as they come!”

This too is nonsense.

“Sweden isn’t socialist,” says Powell. “Volvo is a private company. Restaurants, hotels, they’re privately owned.”

Norway, Denmark and Sweden are all free market economies.

Denmark’s former prime minister was so annoyed with economically ignorant Americans like Bernie Sanders calling Scandanavia “socialist,” he came to America to tell Harvard students that his country “is far from a socialist planned economy. Denmark is a market economy.”

Powell says young people “hear the preaching of socialism, about equality, but they don’t look on what it actually delivers: poverty, starvation, early death.”

For thousands of years, the world had almost no wealth creation. Then, some countries tried capitalism. That changed everything.

“In the last 20 years, we’ve seen more humans escape extreme poverty than any other time in human history, and that’s because of markets,” says Powell.

Capitalism makes poor people richer.

Former Rep. Jamaal Bowman (D-N.Y.) calls capitalism “slavery by another name.”

Rep. Alexandria Ocasio-Cortez (D-N.Y.) claims, “No one ever makes a billion dollars. You take a billion dollars.”

That’s another myth.

People think there’s a fixed amount of money. So when someone gets rich, others lose.

But it’s not true. In a free market, the only way entrepreneurs can get rich is by creating new wealth.

Yes, Steve Jobs pocketed billions, but by creating Apple, he gave the rest of us even more. He invented technology that makes all of us better off.

“I hope that we get 100 new super billionaires,” says economist Dan Mitchell, “because that means 100 new people figured out ways to make the rest of our lives better off.”

Former Labor Secretary Robert Reich advocates the opposite: “Let’s abolish billionaires,” he says.

He misses the most important fact about capitalism: it’s voluntary.

“I’m not giving Jeff Bezos any money unless he’s selling me something that I value more than that money,” says Mitchell.

It’s why under capitalism, the poor and middle class get richer, too.

“The economic pie grows,” says Mitchell. “We are much richer than our grandparents.”

When the media say the “middle class is in decline,” they’re technically right, but they don’t understand why it’s shrinking.

“It’s shrinking because more and more people are moving into upper income quintiles,” says Mitchell. “The rich get richer in a capitalist society. But guess what? The rest of us get richer as well.”

I cover more myths about socialism and capitalism in my new video.

From the Fraser Institute

A report published by the Fraser Institute reaffirms just how much more economically free some states are compared with others. These are places where citizens are allowed to make more of their economic choices. Their taxes are lighter, and their regulatory burdens are easier. The benefits for workers, consumers and businesses have been clear for a long time.

There’s another group of states to watch: “movers” that have become much freer in recent decades. These are states that may not be the freest, but they have been cutting taxes and red tape enough to make a big difference.

How do they fare?

I recently explored this question using 22 years of data from the same Economic Freedom of North America index. The index uses 10 variables encompassing government spending, taxation and labour regulation to assess the degree of economic freedom in each of the 50 states.

Some states, such as New Hampshire, have long topped the list. It’s been in the top five for three decades. With little room to grow, the Granite State’s level of economic freedom hasn’t budged much lately. Others, such as Alaska, have significantly improved economic freedom over the last two decades. Because it started so low, it remains relatively unfree at 43rd out of 50.

Three states—North Carolina, North Dakota and Idaho—have managed to markedly increase and rank highly on economic freedom.

In 2000, North Carolina was the 19th most economically free state in the union. Though its labour market was relatively unhindered by the state’s government, its top marginal income tax rate was America’s ninth-highest, and it spent more money than most states.

From 2013 to 2022, North Carolina reduced its top marginal income tax rate from 7.75 per cent to 4.99 per cent, reduced government employment and allowed the minimum wage to fall relative to per-capita income. By 2022, it had the second-freest labour market in the country and was ninth in overall economic freedom.

North Dakota took a similar path, reducing its 5.54 per cent top income tax rate to 2.9 per cent, scaling back government employment, and lowering its minimum wage to better reflect local incomes. It went from the 27th most economically free state in the union in 2000 to the 10th freest by 2022.

Idaho saw the most significant improvement. The Gem State has steadily improved spending, taxing and labour market freedom, allowing it to rise from the 28th most economically free state in 2000 to the eighth freest in 2022.

We can contrast these three states with a group that has achieved equal and opposite distinction: California, Delaware, New Jersey and Maryland have managed to decrease economic freedom and end up among the least free overall.

What was the result?

The economies of the three liberating states have enjoyed almost twice as much economic growth. Controlling for inflation, North Carolina, North Dakota and Idaho grew an average of 41 per cent since 2010. The four repressors grew by just 24 per cent.

Among liberators, statewide personal income grew 47 per cent from 2010 to 2022. Among repressors, it grew just 26 per cent.

In fact, when it comes to income growth per person, increases in economic freedom seem to matter even more than a state’s overall, long-term level of freedom. Meanwhile, when it comes to population growth, placing highly over longer periods of time matters more.

The liberators are not unique. There’s now a large body of international evidence documenting the freedom-prosperity connection. At the state level, high and growing levels of economic freedom go hand-in-hand with higher levels of income, entrepreneurship, in-migration and income mobility. In economically free states, incomes tend to grow faster at the top and bottom of the income ladder.

These states suffer less poverty, homelessness and food insecurity and may even have marginally happier, more philanthropic and more tolerant populations.

In short, liberation works. Repression doesn’t.

Geopolitics no longer drives oil prices the way it used to

There’s No Bias at CBC News, You Say? Well, OK…

Carney Floor Crossing Raises Counterintelligence Questions aimed at China, Former Senior Mountie Argues

2025: The Year The Narrative Changed

Australian PM booed at Bondi vigil as crowd screams “shame!”

FDA warns ‘breast binder’ manufacturers to stop marketing to gender-confused girls

Argentina’s Milei delivers results free-market critics said wouldn’t work

-

armed forces1 day ago

armed forces1 day agoRemembering Afghanistan and the sacrifices of our military families

-

Fraser Institute1 day ago

Fraser Institute1 day agoHow to talk about housing at the holiday dinner table

-

Frontier Centre for Public Policy1 day ago

Frontier Centre for Public Policy1 day agoTent Cities Were Rare Five Years Ago. Now They’re Everywhere

-

Opinion1 day ago

Opinion1 day agoPope Leo XIV’s Christmas night homily

-

Fraser Institute15 hours ago

Fraser Institute15 hours agoCarney government sowing seeds for corruption in Ottawa

-

Alberta15 hours ago

Alberta15 hours agoAlberta Next Panel calls for less Ottawa—and it could pay off

-

Energy6 hours ago

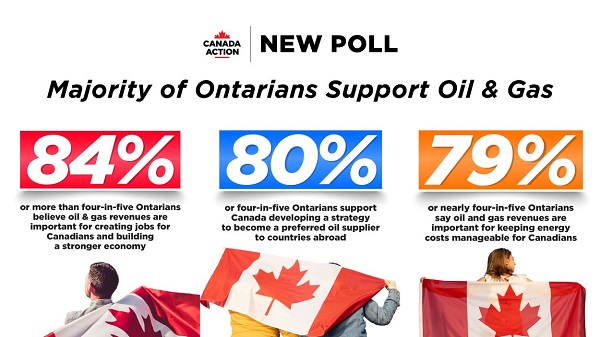

Energy6 hours agoNew Poll Shows Ontarians See Oil & Gas as Key to Jobs, Economy, and Trade

-

Energy15 hours ago

Energy15 hours agoWhile Western Nations Cling to Energy Transition, Pragmatic Nations Produce Energy and Wealth