Business

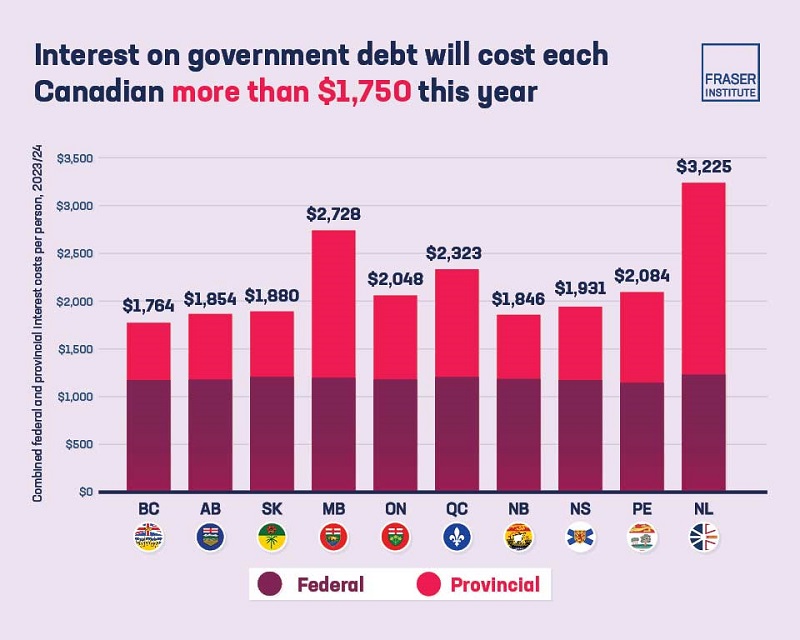

Canadians in every province will pay more than $1,750 per person in 2023-24 on government interest costs amounting to $81.8 billion

From the Fraser Institute

By Jake Fuss and Grady Munro

Canadians in every province will pay more than $1,750 per person in 2023/24 on government interest costs, finds a new study published by the Fraser Institute, an independent, non-partisan Canadian public policy think-tank.

“Interest must be paid on government debt, and the more money governments spend on interest payments the less money is available for the programs and services that matter to Canadians,” said Jake Fuss, director of fiscal studies at the Fraser Institute and author of Federal and Provincial Debt Interest Costs for Canadians, 2024 edition.

The study finds that taxpayers across Canada will pay a total of $81.8 billion on interest payments for the federal and provincial debts this year alone. The federal government will spend $46.5 billion on debt servicing charges in 2023/24, which is more than the government expects to spend on childcare benefits ($31.2 billion) and almost as much as the Canada Health Transfer ($49.4 billion).

Nationally, Newfoundland and Labrador’s combined federal and provincial interest costs is the highest in the country at $3,225 per person. Manitoba is the next highest at $2,728 per person.

Meanwhile, total expenditures on interest costs for Albertans ($8.6 billion) and Ontarians ($31.5 billion) are nearly equivalent to expected spending on K-12 education in their respective provinces this year.

“Even before the COVID-19 pandemic and recession, governments across Canada and in Ottawa were racking up large debts, and this debt imposes real costs on Canadian taxpayers in the form of interest payments,” said Fuss. “Interest payments across the country are substantial, and that takes money away from other important priorities.”

- In recent years, deficit spending and growing government debt have become a trend for many Canadian governments. Like households, governments are required to pay interest on their debt.

- In aggregate, the provinces and federal government are expected to spend $81.8 billion on interest payments in 2023/24.

- Residents in Newfoundland & Labrador face by far the highest combined federal-provincial interest payments per person ($3,225). Manitoba is the next highest at $2,728 per person.

- The federal government will spend $46.5 billion on debt servicing charges in 2023/24, which is nearly what the government expects to spend on the Canada Health Transfer ($49.4 billion), and significantly more than it expects to spend on childcare benefits ($31.2 billion).

- Combined federal-provincial interest costs in Ontario ($31.5 billion), Quebec ($20.3 billion), and Alberta ($8.6 billion) are nearly as much, or more than, what these provinces will spend on K-12 education in 2023/24.

- Meanwhile, combined federal-provincial interest costs for British Columbians ($9.6 billion) are higher than what the province expects to spend on its social services this year.

Authors:

More from this study

The Fraser Institute is an independent Canadian public policy research and educational organization with offices in Vancouver, Calgary, Toronto, and Montreal and ties to a global network of think-tanks in 87 countries. Its mission is to improve the quality of life for Canadians, their families and future generations by studying, measuring and broadly communicating the effects of government policies, entrepreneurship and choice on their well-being. To protect the Institute’s independence, it does not accept grants from governments or contracts for research. Visit www.fraserinstitute.org

![]()

From the Daily Caller News Foundation

During the latest marathon cabinet meeting on Dec. 2, Energy Secretary Chris Wright made news when he told President Donald Trump that “The biggest determinant of the price of energy is politicians, political leaders, and polices — that’s what drives energy prices.”

He’s right about that, and it is why the back-and-forth struggle over federal energy and climate policy plays such a key role in America’s economy and society. Just 10 months into this second Trump presidency, the administration’s policies are already having a profound impact, both at home and abroad.

While the rapid expansion of AI datacenters over the past year is currently being blamed by many for driving up electric costs, power bills were skyrocketing long before that big tech boom began, driven in large part by the policies of the Obama and Biden administration designed to regulate and subsidize an energy transition into reality. As I’ve pointed out here in the past, driving up the costs of all forms of energy to encourage conservation is a central objective of the climate alarm-driven transition, and that part of the green agenda has been highly effective.

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

Please consider making a small donation of any amount here.

Thank you!

President Trump, Wright, and other key appointees like Interior Secretary Doug Burgum and EPA Administrator Lee Zeldin have moved aggressively throughout 2025 to repeal much of that onerous regulatory agenda. The GOP congressional majorities succeeded in phasing out Biden’s costly green energy subsidies as part of the One Big Beautiful Bill Act, which Trump signed into law on July 4. As the federal regulatory structure eases and subsidy costs diminish, it is reasonable to expect a gradual easing of electricity and other energy prices.

This year’s fading out of public fear over climate change and its attendant fright narrative spells bad news for the climate alarm movement. The resulting cracks in the green facade have manifested rapidly in recent weeks.

Climate-focused conflict groups that rely on public fears to drive donations have fallen on hard times. According to a report in the New York Times, the Sierra Club has lost 60 percent of the membership it reported in 2019 and the group’s management team has fallen into infighting over elements of the group’s agenda. Greenpeace is struggling just to stay afloat after losing a huge court judgment for defaming pipeline company Energy Transfer during its efforts to stop the building of the Dakota Access Pipeline.

350.org, an advocacy group founded by Bill McKibben, shut down its U.S. operations in November amid funding woes that had forced planned 25 percent budget cuts for 2025 and 2026. Employees at EDF voted to form their own union after the group went through several rounds of budget cuts and layoffs in recent months.

The fading of climate fears in turn caused the ESG management and investing fad to also fall out of favor, leading to a flood of companies backtracking on green investments and climate commitments. The Net Zero Banking Alliance disbanded after most of America’s big banks – Goldman Sachs, J.P. Morgan Chase, Citigroup, Wells Fargo and others – chose to drop out of its membership.

The EV industry is also struggling. As the Trump White House moves to repeal Biden-era auto mileage requirements, Ford Motor Company is preparing to shut down production of its vaunted F-150 Lightning electric pickup, and Stellantis cancelled plans to roll out a full-size EV truck of its own. Overall EV sales in the U.S. collapsed in October and November following the repeal of the $7,500 per car IRA subsidy effective Sept 30.

The administration’s policy actions have already ended any new leasing for costly and unneeded offshore wind projects in federal waters and have forced the suspension or abandonment of several projects that were already moving ahead. Capital has continued to flow into the solar industry, but even that industry’s ability to expand seems likely to fade once the federal subsidies are fully repealed at the end of 2027.

Truly, public policy matters where energy is concerned. It drives corporate strategies, capital investments, resource development and movement, and ultimately influences the cost of energy in all its forms and products. The speed at which Trump and his key appointees have driven this principle home since Jan. 20 has been truly stunning.

David Blackmon is an energy writer and consultant based in Texas. He spent 40 years in the oil and gas business, where he specialized in public policy and communications.

From the Canadian Energy Centre

Bigger project maintains decades-long marine safety record

The Trans Mountain system continues its decades-long record of zero marine spills, even as oil tanker traffic has surged more than 800 per cent since the pipeline’s expansion in May 2024.

The number of tankers calling at Trans Mountain’s Westridge Marine Terminal in the Port of Vancouver in one month now rivals the number that used to go through in one year.

A global trend toward safer tanker operations

Trans Mountain’s safe operations are part of a worldwide trend. Global oil tanker traffic is up, yet spills are down, according to the International Tanker Owners Pollution Federation, a London, UK-based nonprofit that provides data and response support.

Graph courtesy International Tanker Owners Pollution Federation

Transport Canada reports a 95 per cent drop in ship-source oil spills and spill volumes since the 1970s, driven by stronger ship design, improved response and better regulations.

“Tankers are now designed much more safely. They are double-hulled and compartmentalized to mitigate spills,” said Mike Lowry, spokesperson for the Western Canada Marine Response Corporation (WCMRC).

WCMRC: Ready to protect the West Coast

One of WCMRC’s new response vessels arrives in Barkley Sound. Photo courtesy Western Canada Marine Response Corporation

From eight marine bases including Vancouver and Prince Rupert, WCMRC stands at the ready to protect all 27,000 kilometres of Canada’s western coastline.

Lowry sees the corporation as similar to firefighters — training to respond to an event they hope they never have to see.

In September, it conducted a large-scale training exercise for a worst-case spill scenario. This included the KJ Gardner — Canada’s largest spill response vessel and a part of WCMRC’s fleet since 2024.

“It’s part of the work we do to make sure everybody is trained and prepared to use our assets just in case,” Lowry said.

Expanding capacity for Trans Mountain

The K.J. Gardner is the largest-ever spill response vessel in Canada. Photo courtesy Western Canada Marine Response Corporation

WCMRC’s fleet and capabilities were doubled with a $170-million expansion to support the Trans Mountain project.

Between 2012 and 2024, the company grew from 13 people and $12 million in assets to more than 200 people and $213 million in assets.

“About 80 per cent of our employees are mariners who work as deckhands, captains and marine engineers on our vessels,” Lowry said.

“Most of the incidents we respond to are small marine diesel spills — the last one was a fuel leak from a forest logging vessel near Nanaimo — so we have deployed our fleet in other ways.”

Tanker safety starts with strong rules and local expertise

Tanker loading at the Westridge Marine Terminal in the Port of Vancouver. Photo courtesy Trans Mountain Corporation

Speaking on the ARC Energy Ideas podcast, Trans Mountain CEO Mark Maki said tanker safety starts with strong regulations, including the use of local pilots to guide vessels into the harbour.

“On the Mississippi River, you have Mississippi River pilots because they know how the river behaves. Same thing would apply here in Vancouver Harbour. Tides are strong, so people who are familiar with the harbor and have years and decades of experience are making sure the ships go in and out safely,” Maki said.

“A high standard is applied to any ship that calls, and our facility has to meet very strict requirements. And we have rejected ships, just said, ‘Nope, that one doesn’t fit the bill.’ A ship calling on our facilities is very, very carefully looked at.”

![]()

Working with communities to protect sensitive areas

Beyond escorting ships and preparing for spills, WCMRC partners with coastal communities to map sensitive areas that need rapid protection including salmon streams, clam beds and culturally important sites like burial grounds.

“We want to empower communities and nations to be more prepared and involved,” Lowry said.

“They can help us identify and protect the areas that they value or view as sensitive by working with our mapping people to identify those areas in advance. If we know where those are ahead of time, we can develop a protection strategy for them.”

Net Zero goal is a fundamental flaw in the Ottawa-Alberta MOU

Canadians love Nordic-style social programs as long as someone else pays for them

Trump vows to pause migration after D.C. shooting

Alleged Liberal vote-buying scandal lays bare election vulnerabilities Canada refuses to fix

‘No Critical Thinking’: Parents Sound Alarm As Tech Begins To ‘Replace The Teacher’

Eco-radical Canadian Cabinet minister resigns after oil deal approved

Manitoba Is Doubling Down On A Failed Drug Policy

-

Business2 days ago

Business2 days agoCarney’s Toronto cabinet meetings cost $530,000

-

Artificial Intelligence2 days ago

Artificial Intelligence2 days agoAI is accelerating the porn crisis as kids create, consume explicit deepfake images of classmates

-

Bruce Dowbiggin2 days ago

Bruce Dowbiggin2 days agoIntegration Or Indignation: Whose Strategy Worked Best Against Trump?

-

Health2 days ago

Health2 days ago23,000+ Canadians died waiting for health care in one year as Liberals pushed euthanasia

-

MAiD2 days ago

MAiD2 days ago101-year-old woman chooses assisted suicide — press treats her death as a social good

-

Health2 days ago

Health2 days agoNews RFK Jr.’s vaccine committee to vote on ending Hepatitis B shot recommendation for newborns

-

COVID-1923 hours ago

COVID-1923 hours agoCanadian legislator introduces bill to establish ‘Freedom Convoy Recognition Day’ as a holiday

-

espionage2 days ago

espionage2 days agoDigital messages reportedly allege Chinese police targeted dissident who died suspiciously near Vancouver