Business

Canada can – and should – crack down on trade-based money laundering

From the Macdonald Laurier Institute

By Jamie Ferrill for Inside Policy

Neglecting to take decisive action enables organized criminal networks whose activities cause significant harm on our streets and those of our international partners.

Financial crime bears considerable political and economic risk. For the incoming Trump administration, the threat that transnational organized crime and the illicit financial flows pose to global financial stability is a top priority. The threat of tariffs by the Trump administration makes the costs to Canada in enabling global financial crime all too apparent. In addition to the cost of tariffs themselves, the associated reputational risk and loss of confidence in Canada’s financial system has implications for investments, credit, supply chains, and bilateral co-operation and agreements.

Canada’s proximity to major international markets, stable economy, high standard of living, and strong institutions and frameworks make it an attractive place to do business: for both legitimate and criminal enterprises.

Trade is a key contributing sector for Canada’s economic security. It represents two-thirds of Canada’s GDP, and exports alone support nearly 3.3 million Canadian jobs. Trade is also highly vulnerable to criminal exploitation. Ineffective oversight, regulatory complexity, and lagging technology adoption, coupled with a lack of export controls, make it possible to move vast proceeds of crimes, such as those from drug trafficking, human trafficking, corruption, and tax evasion through the global trade system.

These vulnerabilities are well-known by transnational organized crime groups. They are able to effectively move billions of dollars of dirty money through the global trade system every year, a method commonly referred to as Trade-Based Money Laundering (TBML).

While any statistics must be interpreted with caution, evidence shows that TBML is a prevalent method of money laundering.

What is it?

There are several types of Trade-Based Financial Crimes such as terrorism financing through trade, sanctions evasion, and simply trade fraud. However, the TBML definition is necessarily specific. Essentially here, TBML is a money laundering method: the processing of criminal proceeds to disguise their illegal origin. TBML involves the movement of value through the global trade system to obfuscate the illicit origin. This is usually done through document fraud: undervaluing, overvaluing, phantom shipping, or multiple invoicing. Different techniques employ different aspects of the supply chain. And TBML may be just one method used within larger money laundering operations.

By way of example, US authorities allege that two Chinese nationals living in Chicago laundered tens of millions of dollars for the Sinaloa and Jalisco Cartels. Drugs were smuggled into the United States and sold throughout the country. The proceeds from these sales were collected by the Chinese nationals. Those proceeds were used to purchase bulk electronics in the United States, which were then shipped – with a falsified value – to co-conspirators in China, who sold them locally. The legitimacy provided by the electronics sales and the trade transaction provide cover to “clean” proceeds from precursor crime.

Either the importer and/or the exporter of the goods can shift value. Chances here are the electronics shipped were undervalued: on leaving the country, they are declared at a (much) lower value than they are actually worth. The importer in China pays the undervalued invoice, then sells the goods for what they are worth. The profit from those electronics now appears clean, since it was used for a “legitimate” sale. The ensuing value gap can be transferred informally or stored as illicit wealth. The value has now shifted, without fiat currency leaving the country of origin.

But the cycle does not stop there. The value and money itself continue to traverse around the world, through various intermediaries such as financial institutions or cryptocurrency exchanges. It then goes right back into the system and enables the very crimes and organized crime groups that generated it in the first place. It is, in short, the business model of organized crime.

The Canadian problem

Ultimately, the proceeds of crime that have been legitimised through TBML (and other money laundering methods) supports the criminal enterprises that generated the value in the first place. In the example, these are prolific cartels who have been behind the fentanyl crisis, migrant trafficking and abuse, corruption, and widespread violence that destabilizes communities and undermines governments across North America and beyond.

With new actors, drug routes, and ways of doing business, the cartels are very much active in Canada. The Sinaloa cartel in particular has established a significant presence in Canada where it controls the cocaine market, manufactures and distributes fentanyl, and is embedded in local criminal networks. This increases Canada’s role as a strategic location for drug trafficking and a base to export abroad, notably to Europe, the US, and Australia.

Hells Angels, Red Scorpions, ’Ndrangheta, and other organized crime groups are also exploiting Canada’s strategic location using their transnational links. These groups are active in criminal activities that generate proceeds of crime, which they launder through Canadian institutions. From drug trafficking to extortion to human and sex trafficking, the foundation of organized crime relies on generating and maximizing profits. The proceeds generally need to be laundered; otherwise, there are direct lines back to the criminal organizations. They are, without a doubt, exploiting the trade sector; the very sector that provides so much economic security for Canada.

Canada’s regulation, reporting, and prosecution record for money laundering is notoriously weak. Its record for regulation, reporting, and prosecution for trade-based financial crimes, namely here TBML, is even weaker.

As financial institutions and other regulated entities face increased scrutiny following the TD Bank scandal and the Cullen Commission’s inquiry into money laundering in BC, more criminal activity is likely to be displaced into the trade sector and the institutions it comprises.

TBML is difficult for financial institutions to detect, especially given that 80 per cent of trade is done through open accounts. It exploits established trade structures that are meant to protect the system –like documentation and invoicing processes – by manipulating transactions outside traditional payment systems, which requires more sophisticated anti-money laundering strategies to address these hidden vulnerabilities.

Addressing the problem

Trade is a gaping vulnerability. Yet, it attracts minimal attention in countering transnational financial crime. Containing the fentanyl crisis for one requires a collaborative effort to bolster supply chains and the trade sector against financial crime. This means global cooperation, technological advances (such as blockchain technology), appropriate resourcing, more scrutiny on high-risk countries and shippers, and regulatory innovation.

But political will is in short supply. The federal government’s Budget 2024 and the resulting proposed Regulations Amending Certain Regulations Made Under the Proceeds of Crime (Money Laundering) and Terrorism Financing Act will grant CBSA new authorities to counter TBML, but limited resources to make good on them. And CBSA cannot do it alone.

Transnational organized crime and the illicit financial flows that support it poses a threat to global financial stability. The enabling of financial crime hurts Canada’s reputation abroad. With a new political regime emerging in the US, Canada cannot afford to be seen as a weak link. Loss of confidence in a country and its financial system has implications for investments, credit, supply chains, and bilateral cooperation and agreements.

By neglecting to take decisive action, we inadvertently enable organized criminal networks whose activities cause significant harm on our streets and those of our international partners. With profits as their primary driver, it is imperative that we scrutinize financial pathways to disrupt these illicit operations effectively.

Organized crime groups are not bound by privacy laws, bureaucracy, political agendas, and government budgets. They are continually evolving and staying many steps ahead of what Canada is equipped to control: technologically, geographically, strategically, logistically, and tactically. Without appropriate regulations, technological advances, and resources in place, we will continue to be a laggard in countering financial crime.

More systematic change is needed across regulatory frameworks, law enforcement coordination and resourcing, and international partnerships to strengthen oversight, close loopholes, and enhance detection and disruption. It would be a low-cost signal to the Trump administration that Canada is committed to upping its game.

Jamie Ferrill is senior lecturer in Financial Crime at Charles Sturt University and co-editor of Dirty Money: Financial Crime in Canada.

From the Fraser Institute

According to a recent study, living standards in Canada have declined over the past five years. And the country’s economic growth has been “ugly.” Crucially, all 10 provinces are experiencing this economic stagnation—there are no exceptions to Canada’s “ugly” growth record. In 2026, reversing this trend should be the top priority for the Carney government and provincial governments across the country.

Indeed, demographic and economic data across the country tell a remarkably similar story over the past five years. While there has been some overall economic growth in almost every province, in many cases provincial populations, fuelled by record-high levels of immigration, have grown almost as quickly. Although the total amount of economic production and income has increased from coast to coast, there are more people to divide that income between. Therefore, after we account for inflation and population growth, the data show Canadians are not better off than they were before.

Let’s dive into the numbers (adjusted for inflation) for each province. In British Columbia, the economy has grown by 13.7 per cent over the past five years but the population has grown by 11.0 per cent, which means the vast majority of the increase in the size of the economy is likely due to population growth—not improvements in productivity or living standards. In fact, per-person GDP, a key indicator of living standards, averaged only 0.5 per cent per year over the last five years, which is a miserable result by historic standards.

A similar story holds in other provinces. Prince Edward Island, Nova Scotia, Quebec and Saskatchewan all experienced some economic growth over the past five years but their populations grew at almost exactly the same rate. As a result, living standards have barely budged. In the remaining provinces (Newfoundland and Labrador, New Brunswick, Ontario, Manitoba and Alberta), population growth has outstripped economic growth, which means that even though the economy grew, living standards actually declined.

This coast-to-coast stagnation of living standards is unique in Canadian history. Historically, there’s usually variation in economic performance across the country—when one region struggles, better performance elsewhere helps drive national economic growth. For example, in the early 2010s while the Ontario and Quebec economies recovered slowly from the 2008/09 recession, Alberta and other resource-rich provinces experienced much stronger growth. Over the past five years, however, there has not been a “good news” story anywhere in the country when it comes to per-person economic growth and living standards.

In reality, Canada’s recent record-high levels of immigration and population growth have helped mask the country’s economic weakness. With more people to buy and sell goods and services, the overall economy is growing but living standards have barely budged. To craft policies to help raise living standards for Canadian families, policymakers in Ottawa and every provincial capital should remove regulatory barriers, reduce taxes and responsibly manage government finances. This is the great policy challenge for governments across the country in 2026 and beyond.

Ben Eisen

Senior Fellow, Fraser Institute

Jake Fuss

Director, Fiscal Studies, Fraser Institute

A Minneapolis day care run by Somali immigrants is claiming that a mysterious break-in wiped out its most sensitive records, even as police say officers were never told that anything was actually stolen — a discrepancy that’s drawing sharp attention amid Minnesota’s spiraling child care fraud scandal.

According to the center’s manager, Nasrulah Mohamed, someone forced their way into Nakomis Day Care Center earlier this week by entering through a rear kitchen area, damaging a wall and accessing the office. Mohamed told reporters the intruder made off with “important documentation,” including children’s enrollment records, employee files, and checkbooks tied to the facility’s operations.

But a preliminary report from the Minneapolis Police Department tells a different story. Police say no loss was reported to officers at the time of the call. While the department confirmed the center later contacted police with additional information, an updated report was not immediately available.

Video released by the day care purporting to show damage from the incident depicts a hole punched through drywall inside what appears to be a utility closet, with stacks of cinder blocks visible just behind the wall — imagery that has only fueled skepticism as investigators continue to unravel what authorities have described as one of the largest fraud schemes ever tied to Minnesota’s human services programs.

Mohamed blamed the alleged break-in on fallout from a viral investigation by YouTuber Nick Shirley, who recently toured nearly a dozen Minnesota day care sites while questioning whether they were legitimately operating. Shirley’s video has racked up more than 110 million views. Mohamed insisted the coverage unfairly targeted Somali operators and said his center has since received what he described as hateful and threatening messages.

A manager at the Nokomis Daycare Center in Minneapolis detailed "extensive vandalism" at the facility during a Wednesday news conference.

Manager Nasrulah Mohamed reported that the suspect stole important employee and client documents, an incident he attributed to YouTuber Nick… pic.twitter.com/71nNTSXdTT

— FOX 9 (@FOX9) December 31, 2025

“This is devastating news, and we don’t know why this is targeting our Somali community,” Mohamed said, calling Shirley’s reporting false. Nakomis Day Care Center was not among the facilities featured in the video.

The break-in claim surfaced as law enforcement and federal officials continue to expose a massive fraud network centered in Minneapolis, involving food assistance, housing, and child care payments. Authorities say at least $1 billion has already been identified as fraudulent, with federal prosecutors warning the total could climb as high as $9 billion. Ninety-two people have been charged so far, 80 of them Somali immigrants.

Late Tuesday, the U.S. Department of Health and Human Services announced it was freezing all federal child care payments to Minnesota unless the state can prove the funds are being used lawfully. The payments totaled roughly $185 million in 2025 alone.

Minnesota Gov. Tim Walz, under intensifying scrutiny for allowing fraud to metastasize for years, responded by attacking the Trump administration rather than addressing the substance of the findings. “This is Trump’s long game,” Walz wrote on X Tuesday night, claiming the administration was politicizing fraud enforcement to defund programs — despite federal officials pointing to documented abuse and ongoing criminal cases.

Meanwhile, questions continue to swirl around facilities already flagged by investigators. Reporters visiting several sites highlighted in Shirley’s video found at least one — Quality “Learing” Center — operating with children inside despite state officials previously saying it had been shut down. The Minnesota Department of Children, Youth, and Families later issued a confusing clarification, saying the center initially reported it would close but later claimed it would remain open.

As Minnesota scrambles to respond to the funding freeze and mounting arrests, the conflicting accounts surrounding the Nakomis Day Care incident underscore a broader problem confronting state leaders: a system so riddled with gaps and contradictions that even basic facts — like whether records were actually stolen — are now in dispute, while taxpayers are left holding the bill.

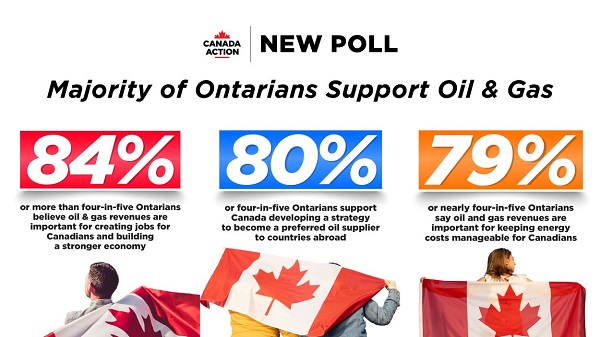

New Poll Shows Ontarians See Oil & Gas as Key to Jobs, Economy, and Trade

Largest fraud in US history? Independent Journalist visits numerous daycare centres with no children, revealing massive scam

“Magnitude cannot be overstated”: Minnesota aid scam may reach $9 billion

US Under Secretary of State Slams UK and EU Over Online Speech Regulation, Announces Release of Files on Past Censorship Efforts

Sweden Fixed What Canada Won’t Even Name

Socialism vs. Capitalism

Canada’s debate on energy levelled up in 2025

-

Business2 days ago

Business2 days agoDark clouds loom over Canada’s economy in 2026

-

Business2 days ago

Business2 days agoThe Real Reason Canada’s Health Care System Is Failing

-

Business2 days ago

Business2 days agoFederal funds FROZEN after massive fraud uncovered: Trump cuts off Minnesota child care money

-

Addictions2 days ago

Addictions2 days agoCoffee, Nicotine, and the Politics of Acceptable Addiction

-

Opinion2 days ago

Opinion2 days agoGlobally, 2025 had one of the lowest annual death rates from extreme weather in history

-

International23 hours ago

International23 hours agoTrump confirms first American land strike against Venezuelan narco networks

-

Business22 hours ago

How convenient: Minnesota day care reports break-in, records gone

-

Business22 hours ago

The great policy challenge for governments in Canada in 2026