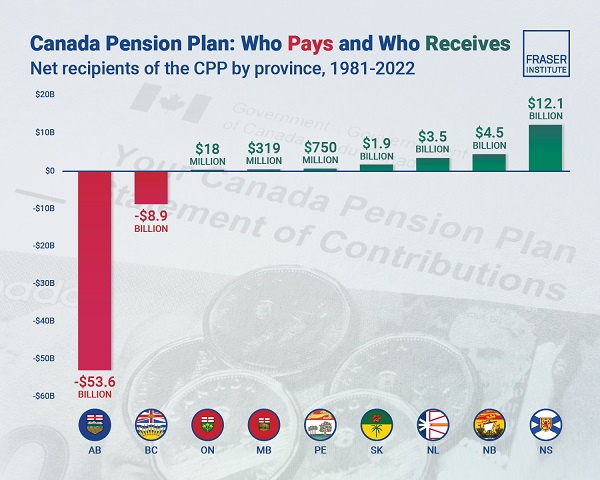

Alberta

Albertans have contributed $53.6 billion to the retirement of Canadians in other provinces

From the Fraser Institute

By Tegan Hill and Nathaniel Li

Albertans contributed $53.6 billion more to CPP then retirees in Alberta received from it from 1981 to 2022

Albertans’ net contribution to the Canada Pension Plan —meaning the amount Albertans paid into the program over and above what retirees in Alberta

received in CPP payments—was more than six times as much as any other province at $53.6 billion from 1981 to 2022, finds a new report published today by the Fraser Institute, an independent, non-partisan Canadian public policy think-tank.

“Albertan workers have been helping to fund the retirement of Canadians from coast to coast for decades, and Canadians ought to know that without Alberta, the Canada Pension Plan would look much different,” said Tegan Hill, director of Alberta policy at the Fraser Institute and co-author of Understanding Alberta’s Role in National Programs, Including the Canada Pension Plan.

From 1981 to 2022, Alberta workers contributed 14.4 per cent (on average) of the total CPP premiums paid—Canada’s compulsory, government- operated retirement pension plan—while retirees in the province received only 10.0 per cent of the payments. Alberta’s net contribution over that period was $53.6 billion.

Crucially, only residents in two provinces—Alberta and British Columbia—paid more into the CPP than retirees in those provinces received in benefits, and Alberta’s contribution was six times greater than BC’s.

The reason Albertans have paid such an outsized contribution to federal and national programs, including the CPP, in recent years is because of the province’s relatively high rates of employment, higher average incomes, and younger population.

As such, if Alberta withdrew from the CPP, Alberta workers could expect to receive the same retirement benefits but at a lower cost (i.e. lower payroll tax) than other Canadians, while the payroll tax would likely have to increase for the rest of the country (excluding Quebec) to maintain the same benefits.

“Given current demographic projections, immigration patterns, and Alberta’s long history of leading the provinces in economic growth, Albertan workers will likely continue to pay more into it than Albertan retirees get back from it,” Hill said.

Understanding Alberta’s Role in National Programs, Including the Canada Pension Plan

- Understanding Alberta’s role in national income transfers and other important programs is crucial to informing the broader debate around Alberta’s possible withdrawal from the Canada Pension Plan (CPP).

- Due to Alberta’s relatively high rates of employment, higher average incomes, and younger population, Albertans contribute significantly more to federal revenues than they receive back in federal spending.

- From 1981 to 2022, Alberta workers contributed 14.4 percent (on average) of the total CPP premiums paid while retirees in the province received only 10.0 percent of the payments. Albertans net contribution was $53.6 billion over the period—approximately six times greater than British Columbia’s net contribution (the only other net contributor).

- Given current demographic projections, immigration patterns, and Alberta’s long history of leading the provinces in economic growth and income levels, Alberta’s central role in funding national programs is unlikely to change in the foreseeable future.

- Due to Albertans’ disproportionate net contribution to the CPP, the current base CPP contribution rate would likely have to increase to remain sustainable if Alberta withdrew from the plan. Similarly, Alberta’s stand-alone rate would be lower than the current CPP rate.

Tegan Hill

Director, Alberta Policy, Fraser Institute

Nathaniel Li

Senior Economist, Fraser Institute

When Democratic Tools Become Weapons

A Canadian politician once kept his legislative seat while serving time in prison.

Gilles Grégoire, a founding figure in Quebec’s nationalist movement, was convicted in 1983 of multiple counts of sexual assault against minors, mostly girls between the ages of 10 and 14. He inhabited a cell yet remained a member of the National Assembly. A representative of free citizens could no longer walk among them.

Grégoire became the kind of figure who seems made for a recall law. His presence in office after conviction insulted the very notion of a democratic mandate. Yet Quebec lacked recall legislation, and the Assembly chose not to intervene. The episode lingers as a reminder that even robust democracies sometimes fail to protect themselves from rare, glaring contradictions.

Such cases hold powerful sway over the political imagination. They tempt reformers to believe that recall is the cure for democratic injustice, giving it exceptional weight it does not deserve. A constitution shaped by anomalies becomes a constitution shaped by distortion.

We are grateful that you’re enjoying Haultain Research.

For the full experience, and to help us bring you more quality research and commentary, please upgrade your subscription.

Alberta’s own history proves the point, though the lesson has been forgotten. William Aberhart’s rise in 1935 owed more to spiritual magnetism and Depression-era desperation than to prudent reform. He promised Social Credit prosperity through monthly dividends to all citizens. The electorate believed that a new economic order would arrive at a cheerful pace. It did not. Within eighteen months of taking office, Aberhart found himself the target of what he himself had created. His government had passed recall legislation in its first session, fulfilling a campaign promise to democratize Alberta’s government. When the promised dividends failed to materialize, his own constituents in Okotoks-High River began gathering signatures for his removal. The charge was not misconduct but failure to deliver miracles.

Faced with this threat, Aberhart’s government retroactively repealed the recall legislation rather than allow him to be forced from his seat. He thus became the first Canadian politician to institute recall and to be threatened with it. History recorded the episode as a cautionary tale rather than a triumph of democratic vigilance. It showed how easily recall could slip from a tool for integrity to a weapon for frustration, revealing a truth that democratic societies often forget: mechanisms designed for exceptional cases seldom remain limited to them.

Those two stories frame Alberta’s problem today. The province revived recall legislation under Premier Jason Kenney in 2021, with the law taking effect later that year. The measure returned with assurances that high thresholds would prevent misuse. Its defenders claimed recall would restrain arrogance and encourage accountability, offering ordinary Albertans a way to hold politicians accountable between elections. Then, facing discontent within his own party over COVID mandates, Kenney himself became the subject of a different form of recall, a leadership review that undermined his power. Premier Danielle Smith, who succeeded him, amended the recall legislation in July 2025 to make it easier to use. She lowered the signature threshold and extended the collection period, changes that would soon work against her own government.

The result has been quite different from what either leader intended. On October 23, 2025, Alberta approved its first recall petition of the modern era, targeting Education Minister Demetrios Nicolaides in Calgary-Bow. The applicant, Jennifer Yeremiy of a group called AB Resistance, told reporters that their goal was “to put forward enough recalls to trigger an early election.” This was not a response to corruption or criminality. It was an explicit strategy to overturn the results of the 2023 provincial election.

The floodgates opened from there. As of December 10, 2025, twenty-one MLAs face active recall petitions. The list now includes Premier Smith herself, as well as multiple cabinet ministers, backbenchers, and even one NDP opposition member. None confronts allegations of criminality. None confronts evidence of corruption. None resembles Gilles Grégoire. Their adversaries object to education funding decisions, the government’s use of the notwithstanding clause during a teachers’ strike, and various claims of insufficient constituent engagement. These are matters of policy disagreement, not grounds for judicial removal from office.

The principled case for recall legislation deserves some consideration. A democratic society must guard against officeholders whose conduct becomes so egregious that the public cannot wait for the next scheduled election. A mechanism for such removal, carefully designed and narrowly applied, reflects respect for citizenship and the dignity of democratic representation. The theory imagines a vigilant electorate using a sharp tool with care, meeting the rare case with a rare response.

Reality seldom matches this ideal. British Columbia has maintained recall legislation since 1995—thirty years during which not a single MLA has been successfully recalled, despite no shortage of controversial politicians and unpopular decisions. When recall petitions have been attempted there, they have almost exclusively targeted MLAs from close ridings over policy disputes rather than serious misconduct. The pattern is remarkably consistent. Recall becomes a tool for the sore losers of close elections, not a mechanism for removing the genuinely unfit.

This should not surprise us. Most political conflicts involve competing policy visions rather than breaches of trust. Legislators are elected precisely to judge the merits of those visions over a defined term. Elections confer authority because they settle disputes for a time, allowing governments to govern and oppositions to organize for the next contest. A recall mechanism that permits policy quarrels to trigger removal undermines the very purpose of elections. It invites factions to overturn results they dislike through extraordinary means, weakening the equilibrium that representative government tries to protect.

The Aberhart episode illustrates this tendency with clarity. His opponents did not claim he had abused office or engaged in corruption. They claimed he had failed to conjure prosperity, which was entirely true; his promise of monthly dividends proved impossible to deliver. Their frustration stemmed from disappointment rather than betrayal, from unmet expectations rather than broken trust. Yet they seized on the recall mechanism to express that disappointment, nearly removing him on that basis alone. The effort had nothing to do with the integrity of public office and everything to do with the volatility of public expectation during desperate times.

The contemporary Alberta law requires signatures from sixty percent of voters who participated in the last election, collected within 90 days. This appears to be a significant threshold designed to prevent frivolous attempts. The appearance misleads in several ways. First, the threshold is lower than it sounds because it requires sixty percent of actual voters rather than eligible voters—a crucial distinction that substantially reduces the number needed. Second, even petitions that fall short of this threshold can inflict severe political damage. The mere existence of an active recall petition marks an MLA with the taint of public disapproval, regardless of whether the petition succeeds.

The scale and coordination of current efforts reveal something more troubling than isolated expressions of constituent dissatisfaction. A website called Operation Total Recall provides organizational infrastructure for a systematic campaign targeting all 44 MLAs who voted to use the notwithstanding clause during the teachers’ strike. This is not spontaneous grassroots democracy. It is coordinated political warfare using recall as a weapon to overturn electoral outcomes. The effort aims not at removing individual members for cause, but at destabilizing an elected government through mass petitions. Analysis of the 2023 election results shows that five UCP MLAs won by fewer than 1,000 votes, with roughly a dozen more winning by fewer than 2,000. Multiple successful recalls could topple a government with only an 11-seat majority, precisely the outcome the organizers openly seek.

Each successful petition would trigger not just a referendum but also, if that referendum passes, a by-election costing taxpayers between $500,000 and $1 million. This is public money spent not to address disqualifying conduct but to re-litigate policy disagreements that voters already decided in 2023. The financial cost alone should give pause. But the deeper costs run to the foundations of representative government itself.

Prudence counsels caution here. Stable institutions exist precisely to restrain public passions rather than reflect them in every heated moment. Legislators must make decisions that sometimes contradict immediate popular sentiment, particularly when facing complex policy files or managing competing interests across diverse constituencies. A system that keeps them in constant survival mode, forever fighting off recall petitions over unpopular but necessary decisions, cannot foster the kind of judgment that good governance requires. Hayek warned that societies often overestimate their ability to redesign the political order according to the impulses of the moment, mistaking the intensity of feeling for the wisdom of action. Recall legislation embodies exactly this temptation, pretending to offer precise accountability while producing disorder and instability.

The concerns of those organizing these recall campaigns may well be sincere. Many genuinely believe that government policies on education funding or the use of constitutional override powers represent serious failures deserving extraordinary remedy. But sincerity of belief does not make the remedy appropriate. These matters played out during the 2023 election campaign. Voters heard the arguments on both sides. They weighed the competing visions. They made their choices. Those choices produced a government with a mandate to govern according to its platform, which included the education policies and approach to constitutional questions now under attack through recall petitions.

A representative who steals public funds or breaks criminal law betrays the trust voters placed in him. Recall aimed at such behaviour may have genuine merit, providing a necessary safeguard against serious malfeasance. But a representative who supports an unpopular policy does not betray his office—he exercises the judgment he was elected to exercise. That is the political job. Voters who disagree may vote him out at the end of his term. They ought not demand his eviction for legislative disagreement over education funding levels or the appropriate use of constitutional tools in labour disputes.

The shift that recall produces goes beyond individual cases. It fundamentally alters the character of political engagement, moving energy away from long-term relationship building and toward short-term confrontation. Petition campaigns demand signatures rather than solutions. They mobilize resentment rather than reflection. They organize anger rather than deliberation. The timing of the first modern recall petition makes this dynamic clear—it launched during a province-wide teachers’ strike, piggybacking on existing mobilization and emotion. But teachers’ strikes happen. Contract negotiations sometimes get contentious. Should every education minister facing difficult bargaining face recall? Should every healthcare minister dealing with doctors’ disputes become a petition target? This path leads to governance by perpetual crisis, where every unpopular but necessary decision triggers a removal campaign.

The effect on the dignity and effectiveness of public work deserves particular attention. Legislators must confront complex files that rarely offer clearly correct answers. They must choose among imperfect options while balancing competing demands from local constituents and provincial interests. Recall turns these unavoidable difficulties into personal liabilities. Taking a principled but unpopular stand risks triggering a petition. The pressure to remain popular at all times can overwhelm the responsibility to remain principled, inverting the proper relationship between representative and constituency.

If Albertans are genuinely dissatisfied with their government’s direction, a perfectly functional mechanism exists to express that dissatisfaction: the next general election, scheduled for October 2027. That is less than two years away—hardly an eternity in democratic terms. In the meantime, voters retain numerous other tools for making their voices heard. They may contact their MLAs directly, organize politically through parties and interest groups, attend town halls and constituency meetings, and build support for the opposition. These traditional channels require patience and persuasion. They require building actual majority support rather than mobilizing intense minorities. Recall petitions short-circuit this democratic process, allowing well-organized groups to force expensive special votes over disputes that were already litigated during the last election. The NDP opposition, which came close but ultimately fell short in 2023, appears in a hurry to open a back door to reverse its electoral fortune through extraordinary means.

The case of Gilles Grégoire illuminates a genuine weakness in democratic systems—the inability to remove someone whose continued presence in office becomes morally intolerable. This reveals a fundamental flaw. But the solution lies in targeted remedies: clear rules for automatic expulsion upon conviction for serious offences, for instance, rather than a broad recall system that allows every policy grievance to become a removal campaign. Such targeted measures would correct specific defects without inviting the broader turmoil that comprehensive recall legislation produces.

Alberta’s present situation echoes the Aberhart lesson with remarkable fidelity. Recall laws seldom remain tied to their original purpose. They drift toward unintended uses, shifting from instruments of moral accountability to weapons of political agitation. They reward passion rather than judgment at precisely the time when there is already far too much passion and not nearly enough good political judgment. They trade stability for drama and substitute the illusion of democratic empowerment for the reality of weakened institutions that guard freedom.

When Jason Kenney introduced recall legislation in 2021, Alberta had twenty-six years of British Columbia evidence showing how these laws function in practice. That evidence pointed clearly in one direction. Yet the UCP proceeded anyway, and in July 2025, the Smith government made recalls even easier, lowering thresholds and extending signature periods precisely when the government enjoyed a comfortable majority. Now, multiple petitions target UCP cabinet ministers and backbenchers while organizers openly seek to force an early election. The NDP leader’s response captured the irony perfectly: “Hoisted on your own petard.”

A healthy political community requires transparent elections that produce precise results, firm mandates that allow governments to govern, and representatives who can exercise judgment with appropriate stability between electoral contests. It requires citizens who understand that disagreement over policy, much less tit for tat, does not warrant removal. It requires carefully designed safeguards against genuine abuse of office rather than mechanisms that allow temporary frustration to masquerade as a permanent principle. Recall legislation promises a swift cure for democratic ailments while delivering turbulence and rewarding radical impatience.

Democracy depends on accepting election results even when we disagree with them. It depends on waiting for our turn to make our case to voters at the next scheduled opportunity. The recall weapon undermines these basic norms in the service of immediate partisan advantage, encouraging precisely the kind of political mischief that corrodes public trust. This is not democratic vitality expressing itself through new channels. It is democratic exhaustion, the permanent campaign that prevents anyone from governing.

Alberta stands at a point where history speaks with unusual clarity. The Grégoire case shows us the moral outlier who truly deserved immediate removal from office. The Aberhart episode shows us the grave danger of using recall for anything less serious. The voters of this province should draw the correct lesson from both stories. They should protect democracy by resisting the recall illusion—not by eliminating all accountability mechanisms, but by insisting that extraordinary remedies be reserved for truly remarkable circumstances rather than routine policy disputes. That distinction makes all the difference between a legitimate tool and a partisan weapon.

We are grateful that you’re enjoying Haultain Research.

For the full experience, and to help us bring you more quality research and commentary, please upgrade your subscription.

From the Fraser Institute

By Tegan Hill and Austin Thompson

According to Calgarians for Thoughtful Growth (CFTG)—an organization advocating against “blanket rezoning”— housing would be more affordable if the mayor and council restricted what homes can be built in Calgary and where. But that gets the economics backwards.

Blanket rezoning—a 2024 policy that allowed homebuilders to construct duplexes, townhomes and fourplexes in most neighbourhoods—allowed more homebuilding, giving Calgarians more choice, and put downward pressure on prices. Mayor Farkas and several councillors campaigned on repealing blanket rezoning and on December 15 council will debate a motion that could start that process. As Calgarians debate the city’s housing rules, residents should understand the trade-offs involved.

When CFTG claims that blanket rezoning does “nothing” for affordability, it ignores a large body of economic research showing the opposite.

New homes are only built when they can be sold to willing homebuyers for a profit. Restrictions that limit the range of styles and locations for new homes, or that lock denser housing behind a long, costly and uncertain municipal approval process, inevitably eliminate many of these opportunities. That means fewer new homes are built, which worsens housing scarcity and pushes up prices. This intuitive story is backed up by study after study. An analysis by Canada’s federal housing agency put it simply: “higher residential land use regulation seems to be associated with lower housing affordability.”

CFTG also claims that blanket rezoning merely encourages “speculation” (i.e. buying to sell in the short-term for profit) by investors. Any profitable housing market may invite some speculative activity. But homebuilders and investors can only survive financially if they make homes that families are willing to buy or rent. The many Calgary families who bought or rented a new home enabled by blanket rezoning did so because they felt it was their best available option given its price, amenities and location—not because they were pawns in some speculative game. Calgarians benefit when they are free to choose the type of home and neighbourhood that best suits their family, rather than being constrained by the political whims of city hall.

And CFTG’s claim that blanket rezoning harms municipal finances also warrants scrutiny. More specifically, CFTG suggests that developers do not pay for infrastructure upgrades in established neighbourhoods, but this is simply incorrect. The City of Calgary charges an “Established Area Levy” to cover the cost of water and wastewater upgrades spurred by redevelopment projects—raising $16.5 million in 2024 alone. Builders in the downtown area must pay the “Centre City Levy,” which funds several local services (and generated $2.5 million in 2024).

It’s true that municipal fees on homes in new communities are generally higher, but that reflects the reality that new communities require far more new pipes, roads and facilities than established neighbourhoods.

Redeveloping established areas of the city means more residents can make use of streets, transit and other city services already in place, which is often the most cost-effective way for a city to grow. The City of Calgary’s own analysis finds that redevelopment in established neighbourhoods saves billions of taxpayer dollars on capital and operating costs for city services compared to an alternative scenario where homebuilding is concentrated in new suburban communities.

An honest debate about blanket rezoning ought to acknowledge the advantages this system has in promoting housing choice, housing affordability and the sustainability of municipal finances.

Clearly, many Calgarians felt blanket rezoning was undesirable when they voted for mayoral and council candidates who promised to change Calgary’s zoning rules. However, Calgarians also voted for a mayor who promised that more homes would be built faster, and at affordable prices—something that will be harder to achieve if city hall imposes tighter restrictions on where and what types of homes can be built. This unavoidable tension should be at the heart of the debate.

CFTG is promoting a comforting fairy tale where Calgary can tighten restrictions on homebuilding without limiting supply or driving up prices. In reality, no zoning regime delivers everything at once—greater neighbourhood control inevitably comes at the expense of housing choice and affordability. Calgarians—including the mayor and council—need a clear understanding of the trade-offs.

Tegan Hill

Director, Alberta Policy, Fraser Institute

Austin Thompson

Senior Policy Analyst, Fraser Institute

Why Does Canada “Lead” the World in Funding Racist Indoctrination?

US Condemns EU Censorship Pressure, Defends X

Will this deal actually build a pipeline in Canada?

The West Needs Bogeymen (Especially Russia)

Loblaws Owes Canadians Up to $500 Million in “Secret” Bread Cash

They know they are lying, we know they are lying and they know we know but the lies continue

The day the ‘King of rock ‘n’ roll saved the Arizona memorial

-

Alberta1 day ago

The Recall Trap: 21 Alberta MLA’s face recall petitions

-

illegal immigration1 day ago

illegal immigration1 day agoUS Notes 2.5 million illegals out and counting

-

International1 day ago

International1 day agoTyler Robinson shows no remorse in first court appearance for Kirk assassination

-

2025 Federal Election2 days ago

2025 Federal Election2 days agoToo Close for Comfort: Carney Floor Crosser Comes From a Riding Tainted by PRC Interference

-

Business2 days ago

Business2 days agoHigh-speed rail between Toronto and Quebec City a costly boondoggle for Canadian taxpayers

-

Business2 days ago

Business2 days agoThe world is no longer buying a transition to “something else” without defining what that is

-

Energy1 day ago

Energy1 day agoCanada’s future prosperity runs through the northwest coast

-

Daily Caller18 hours ago

Daily Caller18 hours ago‘There Will Be Very Serious Retaliation’: Two American Servicemen, Interpreter Killed In Syrian Attack