Business

28 energy leaders call for eliminating ALL energy subsidies—even ones they benefit from

Energy Talking Points by Alex Epstein

Alex Epstein

Alex Epstein

This is the kind of integrity we need from industry—and from Congress.

Dear Chairman Smith and Chairman Crapo:

We, the undersigned American energy producers and investors, write to voice our principled support for full repeal of the Inflation Reduction Act’s (IRA) energy subsidies, including subsidies that would appear to be to our firms’ and industry’s benefit. This is the only moral and practical path forward if we are to truly unleash American energy.

In recent weeks, Congress has been embroiled in battles over which, if any, of the IRA energy subsidies to cut. Lobbyists representing every corner of the energy landscape, including trade groups that many of us are part of, are jockeying to preserve their own piece of the pie, claiming that it is uniquely valuable.

We have oil lobbyists fighting to keep carbon capture and hydrogen subsidies, solar and wind lobbyists fighting to keep solar and wind subsidies, biofuel lobbyists fighting to keep biofuel subsidies, and EV lobbyists fighting to keep EV subsidies.

If this continues, we will likely preserve most if not all of the subsidies, which, deep down, everyone knows are not good for America.

The fundamental truth about subsidies is very simple. For any product, including energy, a subsidy is just a way of taking money from more efficient producers—and from taxpayers—and giving it to less efficient producers. The result is always less efficient production and therefore higher costs or lower quality for Americans.

The most egregious example of subsidies’ destructiveness is the IRA’s solar and wind subsidies, which pay electric utilities to invest much more money in solar and wind than they otherwise would, and thus much less in coal and gas than they otherwise would. Ultimately this means higher electricity prices and certainly less electricity reliability for Americans.

The IRA subsidies’ devastating harm to American energy is more than enough to compel us, as energy producers, to oppose them.

But their harm goes far beyond energy, as they will dramatically increase our debt and ultimately undermine every aspect of our economy.

A central Congressional priority is to curb the national debt during the upcoming budget reconciliation exercise. But according to credible estimates, the IRA will cost over $1 trillion over the next decade and trillions more after that. Worse, the IRA subsidies are expected to misallocate, into uncompetitive business and jobs, $3 trillion of investment by 2032 and $11 trillion by 2050. That’s a disaster for our economy, and for real job opportunities.

Clearly, the right thing to do is to eliminate all these subsidies. When lobbyists say that these subsidies are essential for America, what they’re really saying is that their backers have made investments in projects that have no near term cost-effectiveness and that are totally dependent on indefinite subsidies to sustain themselves.

Most people know the truth, but are afraid to say it due to institutional pressures. Too many Congressmen are afraid of alienating trade groups. Too many trade groups are afraid of alienating their large and vocal members who have made investments hoping for indefinite subsidies. All the while, too few are talking about freedom.

That’s why we invite our colleagues to do the right thing: level with the American people, say that we made a mistake, and that those who built subsidy-dependent businesses took on the kind of risk that we do not want to reward.

Keeping the IRA subsidies—despite all the evidence that they benefit only special interests at the expense of America—risks making our nation ever more like Europe, where industries do not succeed by providing the best value to consumers, but by providing the best favors to politicians. That’s not the America we want to work in.

Sincerely,

Bud Brigham, Founder, Atlas Energy Services and Brigham Exploration

David Albin, Managing Partner, Spectra Holdings

Adam Anderson, CEO, Innovex International

Thurmon Andress, Chairman and CEO, Andress Oil

Don Bennett, Managing Partner, Bennett Ventures LP

Greg Bird, CEO and President, Jetta Operating Company

David de Roode, Partner, Lockton

Andy Eidson, CEO, Alpha Metallurgical Resources

Matt Gallagher, President and CEO, Greenlake Energy

Mike Howard, CEO, Howard Energy

Justin Thompson, CEO, Iron Senergy

Ed Kovalik, CEO, Prairie Operating Company

Thomas E. Knauff, Executive Chairman, EDP

Lance Langford, CEO, Langford Energy Partners

Mickey McKee, CEO, Kodiak Gas Services

Mike O’Shaughnessy, CEO, Lario Oil and Gas Company

D. Martin Phillips, Founder, EnCap Investments LP

Karl Pfluger, midstream executive

David Rees-Jones, President, Chief Energy

Rob Roosa, CEO, Brigham Royalties

Bobby Shackouls, Former CEO, Burlington Resources

Ross Stevens, Founder and CEO, Stone Ridge Holdings Group

Kyle Stallings, CEO, Desert Royalty Company

Justin Thompson, CEO, Iron Senergy

Mike Wallace, Partner, Wallace Family Partnership

Ladd Wilks, CEO, ProFrac

Denzil West, CEO, Admiral Permian Operating

Bill Zartler, Founder and CEO, Solaris Oilfield Infrastructure

Additional signatories (email [email protected] to add yours):

Jimmy Brock, Executive Chairman, Core Natural Resources

Ted Williams, President and CEO, Rockport Energy Solutions LLC

To make sure as many politicians as possible see this letter, help us by sharing on Twitter/X and tagging your Congressmen! Congress is currently undecided about what to do about the IRA subsidies, so now is the moment to make your voice heard.

“Energy Talking Points by Alex Epstein” is my free Substack newsletter designed to give as many people as possible

access to concise, powerful, well-referenced talking points on the latest energy, environmental,

and climate issues from a pro-human, pro-energy perspective.

Share Energy Talking Points by Alex Epstein

![]()

From the Daily Caller News Foundation

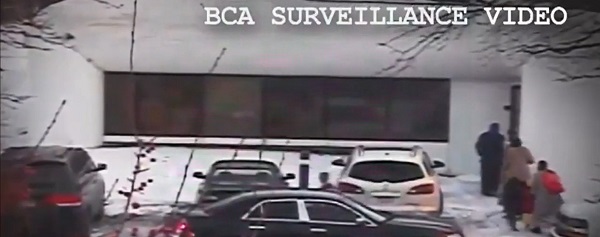

A resurfaced 2018 video from a Minneapolis-area TV station shows how Somali scammers allegedly bilked Minnesota out of millions of dollars for services that they never provided.

Independent journalist Nick Shirley touched off a storm on social media Friday after he posted a photo of one day-care center, which displayed a banner calling it “The Greater Learing Center” on X, along with a 42-minute video that went viral showing him visiting that and other day-care centers. The surveillance video, which aired on Fox 9 in 2018 after being taken in 2015, showed parents taking kids into the center, then leaving with them minutes later, according to Fox News.

“They were billing too much, they went up to high,” Hennepin County attorney Mike Freeman told Fox 9 in 2018. “It’s hard to imagine they were serving that many people. Frankly if you’re going to cheat, cheat little, because if you cheat big, you’re going to get caught.”

Dear Readers:

As a nonprofit, we are dependent on the generosity of our readers.

Please consider making a small donation of any amount here.

Thank you!

Democratic Gov. Tim Walz of Minnesota was accused of engaging in “systemic” retaliation against whistleblowers in a Nov. 30 statement by state employees. Assistant United States Attorney Joe Thompson announced on Dec. 18 that the amount of suspected fraud in Minnesota’s Medicaid program had reached over $9 billion.

After Shirley’s video went viral, FBI Director Kash Patel announced the agency was already sending additional resources in a Sunday post on X, citing the case surrounding Feeding Our Future, which at one point accused the Minnesota government of racism during litigation over the suspension of funds after earlier allegations of fraud.

KSTP reported that the Quality Learning Center, one of the centers visited by Shirley, had 95 citations for violations from one Minnesota agency between 2019 to 2023.

President Donald Trump announced in a Nov. 21 post on Truth Social that he would end “Temporary Protected Status” for Somalis in the state in response to allegations of welfare fraud and said that the influx of refugees had “destroyed our country.”

Business

Disclosures reveal Minnesota politician’s husband’s companies surged thousands-fold amid Somali fraud crisis

Rep. Ilhan Omar’s latest financial disclosures reveal seemingly sudden wealth accumulation inside her household, even as Minnesota grapples with revelations of massive fraud that may have siphoned more than $9 billion from government programs. The numbers, drawn from publicly filed congressional reports, show two companies tied to Omar’s husband, Tim Mynett, surging in value at a pace that raises more questions than answers.

According to the filings, Rose Lake Capital LLC — a business advisory firm Mynett co-founded in 2022 — jumped from an assessed range of $1 to $1,000 in 2023 to between $5 million and $25 million in 2024. Even using the most conservative assumptions allowed under Congress’ broad valuation ranges, the company’s value would have increased thousands of times in a single year. The firm advertises itself as a facilitator of “deal-making, mergers and acquisitions, banking, politics and diplomacy.”

Archived versions of Rose Lake’s website once showcased an eye-catching lineup of political heavyweights: former Ambassador to Bahrain Adam Ereli, former Sen. Max Baucus, and prominent Democratic National Committee alumni William Derrough and Alex Hoffman. But as scrutiny surrounding Omar intensifies — particularly over whether her political network intersected with sprawling fraud schemes exposed in Minnesota — the company has quietly scrubbed its online footprint. Names and biographies of team members have vanished, and the firm has not clarified whether these figures remain involved. Omar’s office offered no comment when asked to explain the company’s sudden growth or the removal of its personnel listings.

Mynett, Omar’s third husband, has long been a controversial presence in her political orbit, but the dramatic swell in his business holdings comes at a moment when trust in Minnesota’s oversight systems is already badly shaken. Federal and state investigators now estimate that fraud involving pandemic-era and nonprofit programs may exceed $9 billion, a staggering figure for a state often held up as a model of progressive governance. For many residents, the revelation that Omar’s household wealth soared during the same period only deepens skepticism about who benefited from Minnesota’s expansive social-spending apparatus.

The financial story doesn’t stop with Rose Lake. A second Mynett-linked entity, ESTCRU LLC — a boutique winery registered in Santa Rosa, California — reported an assessed value of $1 million to $5 million in 2024. Just a year earlier, Omar disclosed its worth at $15,000 to $50,000. Despite the dramatic valuation spike, ESTCRU’s online storefront does not appear to function, its last social media activity dates back to early 2023, and the phone number listed on its website is no longer in service. As with Rose Lake, Omar’s office declined to comment on the winery’s sudden rise in reported value.

The House clerk has yet to release 2025 disclosures, leaving unanswered how these companies are performing today — and how such explosive growth materialized in the first place.

Ottawa-Alberta agreement may produce oligopoly in the oilsands

The Top News Stories That Shaped Canadian Energy in 2025 and Will Continue to Shape Canadian Energy in 2026

‘The electric story is over’

Calgary’s new city council votes to ban foreign flags at government buildings

Western Canada’s supply chain for Santa Claus

Communist China arrests hundreds of Christians just days before Christmas

Georgia county admits illegally certifying 315k ballots in 2020 presidential election

-

Business2 days ago

Business2 days agoLand use will be British Columbia’s biggest issue in 2026

-

Digital ID1 day ago

Digital ID1 day agoThe Global Push for Government Mandated Digital IDs And Why You Should Worry

-

Business1 day ago

Business1 day agoFeds pull the plug on small business grants to Minnesota after massive fraud reports

-

Business15 hours ago

Business15 hours agoDOOR TO DOOR: Feds descend on Minneapolis day cares tied to massive fraud

-

Bruce Dowbiggin14 hours ago

Bruce Dowbiggin14 hours agoIn Contentious Canada Reality Is Still Six Degrees Of Hockey

-

Business14 hours ago

Business14 hours agoCanada needs serious tax cuts in 2026

-

Energy2 days ago

Energy2 days agoWhy Japan wants Western Canadian LNG

-

Business3 hours ago

Business3 hours agoOttawa Is Still Dodging The China Interference Threat