Economy

Key energy agencies diverge as demand and oil prices climb

DUBAI, United Arab Emirates (AP) — Leaders of the world’s most consequential energy bodies gathered for a forum Wednesday to discuss the uncertain future of oil as demand rebounds and prices climb, all while a growing roster of nations pledge to transition to cleaner forms of energy.

The forum, which included speakers from the Organization of Petroleum Exporting Countries, the International Energy Agency and the International Energy Forum, presented varying forecasts for oil demand and discussed energy security and market stability.

Yet from the outset, the wider debate on how the world should best transition away from so-called dirty fuels and other sources of carbon emissions that pollute the air played out as speakers gave their remarks.

Major oil-producing nations, like Saudi Arabia and the United Arab Emirates, have long argued that a rapid energy transition away from the fossil fuels that they continue to rely on for revenue will impact global economic growth and hurt the world’s poorest. Those backing a fast-tracked transition insist new investments in energy must go toward expanding existing wind and solar solutions and in funding innovative solutions if the world is to avoid catastrophic global warming levels. On both sides, however, there is agreement that the world is far from reaching sustainable targets as demand for energy grows.

“We are not on track. So how should policy makers respond to this dilemma? The reality is that 80% of the world’s energy needs continue to be met by fossil fuels,” said Joseph McMonigle, secretary general of the Saudi-based International Energy Forum that hosted the symposium. The IEF is the largest organization of energy ministers, with 71 member states, including the United States.

McMonigle said global energy demand has “roared back” to pre-pandemic levels, but that investments in oil and gas are not back to where they were before the COVID-19 crisis.

“Disinvestment in energy supply will not deliver a just and orderly transition and cannot be a response to the climate crisis,” he said, arguing that countries should invest in both greener forms of energy as well as fossil fuels.

The IEF has called for oil and gas investment to reach $525 billion through 2030 to ensure “market balance” despite a slowdown projected in how much demand for oil will grow. The group notes that investment in the oil and gas sector in 2021 stood at $341 billion. Without more financing, the IEF says demand could outstrip future supply within the next five to six years. They say it could also result in switching to more polluting energy sources such as wood and coal.

Others disagree. The International Energy Agency’s executive director has said the world does not need more investments in new oil, gas and coal projects.

From Paris, the IEA’s Fatih Birol did not directly address the comments made by McMonigle, but he echoed the sentiment that the energy transition must happen in an “orderly manner” so that climate targets are met and oil producing economies are seen as part of the solution.

To meet these targets, the world must reduce its consumption of fossil fuels, Birol said, before later adding: “We cannot drop oil and gas tomorrow.”

“The world will need oil and gas for several years to come. However, if we want to reach our climate targets we would need less oil and less coal and less gas than we use today in an unabated format.”

The IEA says that for the world to reach net-zero emissions by 2050, annual clean energy investment worldwide will need to more than triple by 2030 to around $4 trillion. It has also called out the energy sector as the source of around 75% of greenhouse gas emissions, a main driver in climate change.

The IEA estimates that world oil demand is set to expand by 3.2 million barrels per day this year, reaching 100.6 million barrels per day as restrictions to contain the spread of the coronavirus ease. Benchmark crude prices rose by more than 15% in January to cross the $90 per barrel threshold for the first time in more than seven years.

The rebound in demand for oil, combined with a shortfall in energy investments, rising prices and market uncertainty has led to varying energy outlook scenarios. The diverging outlooks by OPEC, the IEF, IEA and others have an impact on how governments choose to formulate their energy policies and decide on production levels as they commit to net-zero pledges.

___

Follow Aya Batrawy on Twitter at www.twitter.com/ayaelb

___

Follow AP’s climate coverage at http://apnews.com/hub/climate

Aya Batrawy, The Associated Press

Alberta

COWBOY UP! Pierre Poilievre Promises to Fight for Oil and Gas, a Stronger Military and the Interests of Western Canada

Fr0m Energy Now

As Calgarians take a break from the incessant news of tariff threat deadlines and global economic challenges to celebrate the annual Stampede, Conservative party leader Pierre Poilievre gave them even more to celebrate.

Poilievre returned to Calgary, his hometown, to outline his plan to amplify the legitimate demands of Western Canada and not only fight for oil and gas, but also fight for the interests of farmers, for low taxes, for decentralization, a stronger military and a smaller federal government.

Speaking at the annual Conservative party BBQ at Heritage Park in Calgary (a place Poilievre often visited on school trips growing up), he was reminded of the challenges his family experienced during the years when Trudeau senior was Prime Minister and the disastrous effect of his economic policies.

“I was born in ’79,” Poilievre said. “and only a few years later, Pierre Elliott Trudeau would attack our province with the National Energy Program. There are still a few that remember it. At the same time, he hammered the entire country with money printing deficits that gave us the worst inflation and interest rates in our history. Our family actually lost our home, and we had to scrimp and save and get help from extended family in order to get our little place in Shaughnessy, which my mother still lives in.”

This very personal story resonated with many in the crowd who are now experiencing an affordability crisis that leaves families struggling and young adults unable to afford their first house or condo. Poilievre said that the experience was a powerful motivator for his entry into politics. He wasted no time in proposing a solution – build alliances with other provinces with mutual interests, and he emphasized the importance of advocating for provincial needs.

“Let’s build an alliance with British Columbians who want to ship liquefied natural gas out of the Pacific Coast to Asia, and with Saskatchewanians, Newfoundlanders and Labradorians who want to develop their oil and gas and aren’t interested in having anyone in Ottawa cap how much they can produce. Let’s build alliances with Manitobans who want to ship oil in the port of Churchill… with Quebec and other provinces that want to decentralize our country and get Ottawa out of our business so that provinces and people can make their own decisions.”

Poilievre heavily criticized the federal government’s spending and policies of the last decade, including the increase in government costs, and he highlighted the negative impact of those policies on economic stability and warned of the dangers of high inflation and debt. He advocated strongly for a free-market economy, advocating for less government intervention, where businesses compete to impress customers rather than impress politicians. He also addressed the decade-long practice of blocking and then subsidizing certain industries. Poilievre referred to a famous quote from Ronald Reagan as the modus operandi of the current federal regime.

“The Government’s view of the economy could be summed up in a few short phrases. If anything moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.”

The practice of blocking and then subsidizing is merely a ploy to grab power, according to Poilievre, making industry far too reliant on government control.

“By blocking you from doing something and then making you ask the government to help you do it, it makes you reliant. It puts them at the center of all power, and that is their mission…a full government takeover of our economy. There’s a core difference between an economy controlled by the government and one controlled by the free market. Businesses have to clamour to please politicians and bureaucrats. In a free market (which we favour), businesses clamour to impress customers. The idea is to put people in charge of their economic lives by letting them have free exchange of work for wages, product for payment and investment for interest.”

Poilievre also said he plans to oppose any ban on gas-powered vehicles, saying, “You should be in the driver’s seat and have the freedom to decide.” This is in reference to the Trudeau-era plan to ban the sale of gas-powered cars by 2035, which the Carney government has said they have no intention to change, even though automakers are indicating that the targets cannot be met. He also intends to oppose the Industrial Carbon tax, Bill C-69 the Impact Assessment Act, Bill C-48 the Oil tanker ban, the proposed emissions cap which will cap energy production, as well as the single-use plastics ban and Bill C-11, also known as the Online Streaming Act and the proposed “Online Harms Act,” also known as Bill C-63. Poilievre closed with rallying thoughts that had a distinctive Western flavour.

“Fighting for these values is never easy. Change, as we’ve seen, is not easy. Nothing worth doing is easy… Making Alberta was hard. Making Canada, the country we love, was even harder. But we don’t back down, and we don’t run away. When things get hard, we dust ourselves off, we get back in the saddle, and we gallop forward to the fight.”

Cowboy up, Mr. Poilievre.

Maureen McCall is an energy professional who writes on issues affecting the energy industry.

Alberta

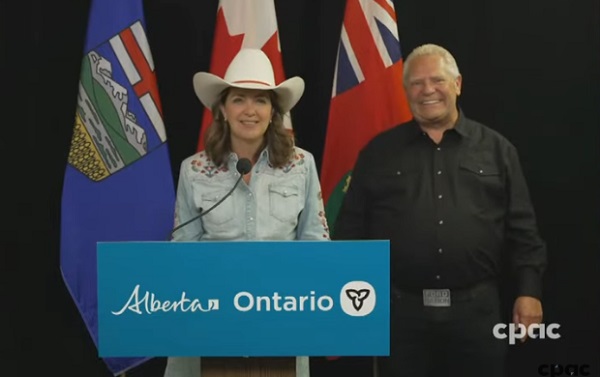

Alberta and Ontario sign agreements to drive oil and gas pipelines, energy corridors, and repeal investment blocking federal policies

Alberta-Ontario MOUs fuel more pipelines and trade

Alberta Premier Danielle Smith and Ontario Premier Doug Ford have signed two memorandums of understanding (MOUs) during Premier Ford’s visit to the Calgary Stampede, outlining their commitment to strengthen interprovincial trade, drive major infrastructure development, and grow Canada’s global competitiveness by building new pipelines, rail lines and other energy and trade infrastructure.

The two provinces agree on the need for the federal government to address the underlying conditions that have harmed the energy industry in Canada. This includes significantly amending or repealing the Impact Assessment Act, as well as repealing the Oil Tanker Moratorium Act, Clean Electricity Regulations, the Oil and Gas Sector Greenhouse Gas Emissions Cap, and all other federal initiatives that discriminately impact the energy sector, as well as sectors such as mining and manufacturing. Taking action will ensure Alberta and Ontario can attract the investment and project partners needed to get shovels in the ground, grow industries and create jobs.

The first MOU focuses on developing strategic trade corridors and energy infrastructure to connect Alberta and Ontario’s oil, gas and critical minerals to global markets. This includes support for new oil and gas pipeline projects, enhanced rail and port infrastructure at sites in James Bay and southern Ontario, as well as end-to-end supply chain development for refining and processing of Alberta’s energy exports. The two provinces will also collaborate on nuclear energy development to help meet growing electricity demands while ensuring reliable and affordable power.

The second MOU outlines Alberta’s commitment to explore prioritizing made-in-Canada vehicle purchases for its government fleet. It also includes a joint commitment to reduce barriers and improve the interprovincial trade of liquor products.

“Alberta and Ontario are joining forces to get shovels in the ground and resources to market. These MOUs are about building pipelines and boosting trade that connects Canadian energy and products to the world, while advocating for the right conditions to get it done. Government must get out of the way, partner with industry and support the projects this country needs to grow. I look forward to working with Premier Doug Ford to unleash the full potential of our economy and build the future that people across Alberta and across the country have been waiting far too long for.”

“In the face of President Trump’s tariffs and ongoing economic uncertainty, Canadians need to work together to build the infrastructure that will diversify our trading partners and end our dependence on the United States. By building pipelines, rail lines and the energy and trade infrastructure that connects our country, we will build a more competitive, more resilient and more self-reliant economy and country. Together, we are building the infrastructure we need to protect Canada, our workers, businesses and communities. Let’s build Canada.”

These agreements build on Alberta and Ontario’s shared commitment to free enterprise, economic growth and nation-building. The provinces will continue engaging with Indigenous partners, industry and other governments to move key projects forward.

“Never before has it been more important for Canada to unite on developing energy infrastructure. Alberta’s oil, natural gas, and know-how will allow Canada to be an energy superpower and that will make all Canadians more prosperous. To do so, we need to continue these important energy infrastructure discussions and have more agreements like this one with Ontario.”

“These MOUs with Ontario build on the work Alberta has already done with Saskatchewan, Manitoba, Northwest Territories and the Port of Prince Rupert. We’re proving that by working together, we can get pipelines built, open new rail and port routes, and break down the barriers that hold back opportunities in Canada.”

“Canada’s economy has an opportunity to become stronger thanks to leadership and steps taken by provincial governments like Alberta and Ontario. Removing interprovincial trade barriers, increasing labour mobility and attracting investment are absolutely crucial to Canada’s future economic prosperity.”

Together, Alberta and Ontario are demonstrating the shared benefits and opportunities that result from collaborative partnerships, and what it takes to keep Canada competitive in a changing world.

Quick facts

- Steering committees with Alberta and Ontario government officials will be struck to facilitate work and cooperation under the agreements.

- Alberta and Ontario will work collaboratively to launch a preliminary joint feasibility study in 2025 to help move private sector led investments in rail, pipeline(s) and port(s) projects forward.

- These latest agreements follow an earlier MOU Premiers Danielle Smith and Doug Ford signed on June 1, 2025, to open up trade between the provinces and advance shared priorities within the Canadian federation.

Related information

Court compels RCMP and TD Bank to hand over records related to freezing of peaceful protestor’s bank accounts

B.C. Residents File Competition Bureau Complaint Against David Suzuki Foundation for Use of False Imagery in Anti-Energy Campaigns

Alberta uncorks new rules for liquor and cannabis

Trump transportation secretary tells governors to remove ‘rainbow crosswalks’

-

Alberta13 hours ago

COWBOY UP! Pierre Poilievre Promises to Fight for Oil and Gas, a Stronger Military and the Interests of Western Canada

-

Alberta1 day ago

Alberta1 day agoAlberta Next: Immigration

-

Alberta13 hours ago

Alberta and Ontario sign agreements to drive oil and gas pipelines, energy corridors, and repeal investment blocking federal policies

-

Business2 days ago

Business2 days agoThe Digital Services Tax Q&A: “It was going to be complicated and messy”

-

International2 days ago

International2 days agoElon Musk forms America Party after split with Trump

-

COVID-1916 hours ago

COVID-1916 hours agoFDA requires new warning on mRNA COVID shots due to heart damage in young men

-

Crime13 hours ago

Crime13 hours agoEyebrows Raise as Karoline Leavitt Answers Tough Questions About Epstein

-

Alberta Sports Hall of Fame and Museum1 day ago

Alberta Sports Hall of Fame and Museum1 day agoAlberta Sports Hall of Fame 2025 Inductee Profiles – Para Nordic Skiing – Brian and Robin McKeever