Alberta

Canadians not feeling great about personal finances… Even worse in Alberta

From MNP Canada

According to the latest MNP Consumer Debt Index being released today, Albertans are finding themselves with a lot less wiggle room in household budgets each month. The amount of money left over after paying all their bills and debt obligations has reached its lowest level since tracking began. Even though the Bank of Canada is expected to keep interest rates stable this week, six in ten in the province say they are more concerned about their ability to repay their debts than they used to be.

MNP Consumer Debt Index Update: Albertans finding themselves with a lot less money each month, six in ten concerned their ability to repay their debts

Stable interest rates are a cold comfort to those already having a difficult time making ends meet

Even though the Bank of Canada has stated that it will keep interest rates stable until next year, six in ten (58%) Albertans say they are more concerned about their ability to repay their debts than they used to be. The concern could be the result of steeply declining wiggle room in household budgets. After paying all their current bills and debt obligations, Albertans say they are, on average, left with $459 at the end of the month, a drop of $209 since June and the lowest level since tracking began in February 2016. Half (49%, +5 pts) say they are left with less than $200 including three in ten (34%) who say they already don’t make enough money to cover all their bills and debt obligations each month (+9 pts).

The findings are part of the latest MNP Consumer Debt Index conducted quarterly by Ipsos. Now in its tenth wave, the Index tracks Canadians’ attitudes about their consumer debt and their perception of their ability to meet their monthly payment obligations.

Average Finances Left at Month-End

Image Caption: Albertans were asked: Thinking about the amount of after-tax income you make each month compared to the amount of your bills and debt obligations each month, how much is left over? In other words, how much wiggle room do you have before you wouldn’t be able to pay all your bills and debt payments each month?

“There has been a marked decline in the amount of wiggle room that households have in Alberta. says Donna Carson, a Licensed Insolvency Trustee with MNP LTD, the country’s largest personal insolvency practice. “Family budgets are being strained by everyday expenses which means many aren’t putting anything away for rainy day savings and that puts them at risk. It is most often unexpected expenses that force people to take on more debt they can’t afford and that begins a cycle of increasing servicing costs, and eventual default.”

It’s no surprise that with less in the bank at month-end, Albertans’ ability to cope with unexpected expenses has been shaken. Seven in ten (70%) are not confident in their ability to cope with life-changing events – such as a divorce, unexpected auto repairs, loss of employment or the death of a family member – without increasing their debt.

“A job loss or an unexpected expense are most devastating for people who already have a large amount of debt. Our research continues to show just how vulnerable Alberta households are to inevitable life events like a car repair,” says Carson who recommends having at least three to six months of expenses saved in case of emergencies.

Albertans may have fewer dollars left at month-end to buffer them from sudden expenses but, somewhat surprisingly, they are growing generally far more positive about their personal financial situations than those in other provinces. According to the index, one quarter (25%) say that their debt situation is better than it was a year ago (+6 pts) and one in three (32%) say that it is better than five years ago (+7 pts). In addition to being optimistic about the present, there has been a significant increase in the proportion who feel more positive about the future. Four in ten (44%) expect that their debt situation a year from now will be better, a jump of 19 points. Six in ten (58%) believe that it will be better five years from now (+13 pts).

“The current holding pattern on interest rates and increasing economic optimism in the province could be giving Albertans a sense of relief about their finances. Still, the fact remains that many Albertans are deeply indebted and most don’t have a clear path to repayment,” says Carson pointing to evidence from the research showing that many may intend to take on more credit to make ends meet over the next year.

Just about half (48%) of Albertans say they don’t think that they will be able to cover all their living and family expenses for the next 12 months without going further into debt, a one-point decrease since June. Furthermore, just under half (49%) are confident they won’t have any debt in retirement, a one-point increase.

“Some may have resigned themselves to being in debt for life. Interest rates may remain stable but there are many already struggling to make ends meet at the current rate,” says Carson.

A large portion of Albertans (53%) are concerned about how rising interest rates will impact their financial situation, up one point since June. Fifty-two per cent agree that if interest rates go up much more, they are afraid they will be in financial trouble (-4 pts). Finally, a third (35%) are still concerned that rising interest rates could move them towards bankruptcy (-7 pts).

“The single biggest mistake people make is taking on more debt to try and deal with debt. Even if you are swimming in credit card debt, with a line of credit, a mortgage, a car loan or all of the above, you can get help to design a debt relief strategy,” says Carson.

MNP LTD offers free consultations with Licensed Insolvency Trustees to help individuals understand their debt relief options. Licensed Insolvency Trustees are the only government-regulated debt professionals who offer a full range of debt relief options and can guarantee legal protection from creditors through consumer proposals and bankruptcies.

About the MNP Consumer Debt Index

The MNP Consumer Debt Index measures Canadians’ attitudes toward their consumer debt and gauges their ability to pay their bills, endure unexpected expenses, and absorb interest-rate fluctuations without approaching insolvency. Conducted by Ipsos and updated quarterly, the Index is an industry-leading barometer of financial pressure or relief among Canadians. Visit www.MNPdebt.ca/CDI to learn more.

The latest data, representing the tenth wave of the MNP Consumer Debt Index, was compiled by Ipsos on behalf of MNP LTD between September 4 and September 9, 2019. For this survey, a sample of 2,002 Canadians aged 18 years and over was interviewed. The precision of online polls is measured using a credibility interval. In this case, the results are accurate to within +2.5 percentage points, 19 times out of 20, of what the results would have been had all Canadian adults been polled. The credibility interval will be wider among subsets of the population. All sample surveys and polls may be subject to other sources of error, including, but not limited to coverage error, and measurement error.

From the Fraser Institute

By Tegan Hill

If the Smith government reversed the 2015 personal income tax rate increases and instituted a flat 8 per cent tax rate, it would help restore Alberta’s position as one of the lowest tax jurisdictions in North America

Over the past decade, Alberta has gone from one of the most competitive tax jurisdictions in North America to one of the least competitive. And while the Smith government has promised to create a new 8 per cent tax bracket on personal income below $60,000, it simply isn’t enough to restore Alberta’s tax competitiveness. Instead, the government should institute a flat 8 per cent personal and business income tax rate.

Back in 2014, Alberta had a single 10 per cent personal and business income tax rate. As a result, it had the lowest top combined (federal and provincial/state) personal income tax rate and business income tax rate in North America. This was a powerful advantage that made Alberta an attractive place to start a business, work and invest.

In 2015, however, the provincial NDP government replaced the single personal income tax rate of 10 percent with a five-bracket system including a top rate of 15 per cent, so today Alberta has the 10th-highest personal income tax rate in North America. The government also increased Alberta’s 10 per cent business income tax rate to 12 per cent (although in 2019 the Kenney government began reducing the rate to today’s 8 per cent).

If the Smith government reversed the 2015 personal income tax rate increases and instituted a flat 8 per cent tax rate, it would help restore Alberta’s position as one of the lowest tax jurisdictions in North America, all while saving Alberta taxpayers $1,573 (on average) annually.

And a truly integrated flat tax system would not only apply a uniform tax 8 per cent rate to all sources of income (including personal and business), it would eliminate tax credits, deductions and exemptions, which reduce the cost of investments in certain areas, increasing the relative cost of investment in others. As a result, resources may go to areas where they are not most productive, leading to a less efficient allocation of resources than if these tax incentives did not exist.

Put differently, tax incentives can artificially change the relative attractiveness of goods and services leading to sub-optimal allocation. A flat tax system would not only improve tax efficiency by reducing these tax-based economic distortions, it would also reduce administration costs (expenses incurred by governments due to tax collection and enforcement regulations) and compliance costs (expenses incurred by individuals and businesses to comply with tax regulations).

Finally, a flat tax system would also help avoid negative incentives that come with a progressive marginal tax system. Currently, Albertans are taxed at higher rates as their income increases, which can discourage additional work, savings and investment. A flat tax system would maintain “progressivity” as the proportion of taxes paid would still increase with income, but minimize the disincentive to work more and earn more (increasing savings and investment) because Albertans would face the same tax rate regardless of how their income increases. In sum, flat tax systems encourage stronger economic growth, higher tax revenues and a more robust economy.

To stimulate strong economic growth and leave more money in the pockets of Albertans, the Smith government should go beyond its current commitment to create a new tax bracket on income under $60,000 and institute a flat 8 per cent personal and business income tax rate.

Author:

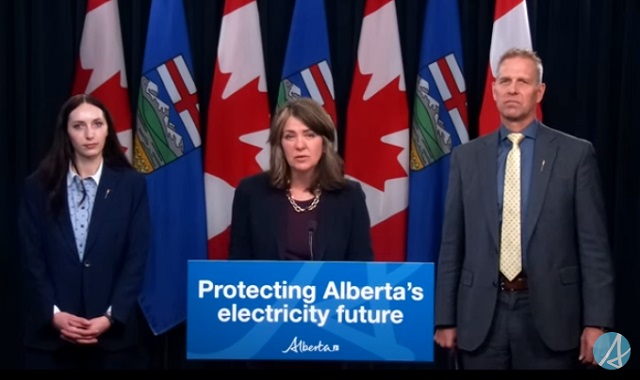

Making utility bills more affordableAlberta’s government is taking action to protect Alberta’s ratepayers by introducing legislation to lower and stabilize local access fees. Affordability is a top priority for Alberta’s government, with the cost of utilities being a large focus. By introducing legislation to help reduce the cost of utility bills, the government is continuing to follow through on its commitment to make life more affordable for Albertans. This is in addition to the new short-term measures to prevent spikes in electricity prices and will help ensure long-term affordability for Albertans’ basic household expenses.

Local access fees are functioning as a regressive municipal tax that consumers pay on their utility bills. It is unacceptable for municipalities to be raking in hundreds of millions in surplus revenue off the backs of Alberta’s ratepayers and cause their utility bills to be unpredictable costs by tying their fees to a variable rate. Calgarians paid $240 in local access fees on average in 2023, compared to the $75 on average in Edmonton, thanks to Calgary’s formula relying on a variable rate. This led to $186 million more in fees being collected by the City of Calgary than expected.

To protect Alberta’s ratepayers, the Government of Alberta is introducing the Utilities Affordability Statutes Amendment Act, 2024. If passed, this legislation would promote long-term affordability and predictability for utility bills by prohibiting the use of variable rates when calculating municipalities’ local access fees. Variable rates are highly volatile, which results in wildly fluctuating electricity bills. When municipalities use this rate to calculate their local access fees, it results in higher bills for Albertans and less certainty in families’ budgets. These proposed changes would standardize how municipal fees are calculated across the province, and align with most municipalities’ current formulas.

If passed, the Utilities Affordability Statutes Amendment Act, 2024 would prevent municipalities from attempting to take advantage of Alberta’s ratepayers in the future. It would amend sections of the Electric Utilities Act and Gas Utilities Act to ensure that the Alberta Utilities Commission has stronger regulatory oversight on how these municipal fees are calculated and applied, ensuring Alberta ratepayer’s best interests are protected.

If passed, this legislation would also amend sections of the Alberta Utilities Commission Act, the Electric Utilities Act, Government Organizations Act and the Regulated Rate Option Stability Act to replace the terms “Regulated Rate Option”, “RRO”, and “Regulated Rate Provider” with “Rate of Last Resort” and “Rate of Last Resort Provider” as applicable. Quick facts

Related information |

Deborah Birx Gets Her Close-Up

CDC Quietly Admits to Covid Policy Failures

Japanese study shows disturbing increase in cancer related deaths during the Covid pandemic

Biden’s Kill Switch: The Growing Threat of Government Control of Your Car

-

Brownstone Institute2 days ago

Deborah Birx Gets Her Close-Up

-

Alberta2 days ago

Alberta2 days agoCoutts Three verdict: A warning to protestors who act as liaison with police

-

Alberta2 days ago

Alberta2 days agoAlberta moves to protect Edmonton park from Trudeau government’s ‘diversity’ plan

-

Energy2 days ago

Energy2 days agoCanada Has All the Elements to be a Winner in Global Energy — Now Let’s Do It

-

Business2 days ago

Business2 days agoMaxime Bernier warns Canadians of Trudeau’s plan to implement WEF global tax regime

-

espionage2 days ago

espionage2 days agoCanada’s intelligence chief says he personally warned Trudeau about China’s election meddling

-

Freedom Convoy2 days ago

Freedom Convoy2 days agoOttawa spent “excessive” $2.2 million fighting Emergencies Act challenge

-

Brownstone Institute2 days ago

Brownstone Institute2 days agoA Coup Without Firing a Shot