Canadian Energy Centre

The importance of Canadian crude oil to refineries in the U.S.

From the Canadian Energy Centre

By Ven VenkatachalamOil from Canada supplies more than 23% of U.S. refinery feedstock, helping bolster North American energy security

Introduction

The refining industry¹ in the United States is one of the world’s largest, with capacity to process 18 million barrels of oil per day. Canada plays a crucial role by supplying more than one-fifth of the crude oil refined in the U.S.

The U.S.–Canada cross-border crude oil trade is essential to North American energy security. Canadian crude oil exports and the U.S. refinery industry are highly integrated. In recent years, Canada’s crude oil sector has been making a growing contribution to the operations of U.S. oil refineries.

U.S. refineries are converting Canadian crude oil, including heavy oil,² into products that North Americans use daily, such as transportation fuels (gasoline and diesel), chemicals, and plastics. Although the U.S. has increased its production of oil in recent years, U.S. refineries still rely on Canadian heavy crude oil to meet their feedstock (i.e., the raw materials and intermediate materials processed at refineries to produce finished petroleum products, otherwise known as refinery inputs) specifications.

In this CEC Fact Sheet, we examine several economic indicators that illustrate the importance of Canadian crude oil, particularly heavy crude, to U.S. refineries. This fact sheet also analyzes the refining industry’s direct and indirect economic impacts on the U.S. economy.

1. NAICS Code 324110 (Petroleum Refineries): This industry comprises

establishments primarily engaged in refining crude petroleum into refined petroleum.

2. A majority of the crude oil imported by the U.S. from Canada is heavy crude (between 15-25 API gravity). API gravity is a commonly used index for measuring the density of crude oil or refined products. Crude oil typically has an API between 15 and 45 degrees. The higher the API, the lighter the crude; the lower the API, the heavier the crude.

Imports of Canadian crude oil to refineries in the United States

The physical characteristics of crude oil determine how it is processed in refineries. Generally, heavy crude oil offers higher yields of low-value products (coke and asphalt) and lower yields of high-value products (gasoline). Heavy crude oil requires more complicated processing than lighter crude if it is to produce high-value products.

Overall, Canadian crude oil imports to U.S. refineries for processing have risen from over 1.3 million barrels per day in 2000 to just under 3.8 million barrels per day in 2022, an increase of 181 per cent (see Figure 1). The per cent of Canadian crude in U.S. refinery feedstock has steadily risen from nearly 9 per cent in 2000 to over 23 per cent by the end of 2022.

Source: U.S. Energy Information Administration (2024a, 2024b, 2024c)

The U.S. refining industry

Since the first U.S. refinery began operating in 1861, the refining industry has been one of the largest manufacturing sectors in the United States. There are currently 129 petroleum refineries across the five U.S. PADDS³ (125 operating refineries and five refineries that are idle but not permanently shut down) (see Table 1).

3. The United States is divided into five Petroleum Administration for Defense Districts (PADDs) for the allocation of fuels derived from petroleum products, including gasoline and diesel fuel. The geographic breakdown of PADDs enables U.S. policymakers to better analyze petroleum supplies in the country

Source: U.S. Energy Information Administration (2023)

Total refining capacity in the United States has risen from 16.2 million barrels of crude processed in 2000 to nearly 17.8 million barrels per day in 2022, an increase of over 8 per cent (see Figure 2). The refining utilization⁴ has also recovered, growing from 79 per cent during COVID-19 to a high of 91 per cent in 2022.

Source: U.S. Energy Information Administration (2024b)

The impact of the U.S. refining industry on the American economy

The estimated direct and indirect economic impacts of the U.S. refining industry in 2024 include 1.6 million direct and indirect jobs, $206 billion in labour income, $577 billion in direct and indirect value-added, and $1.6 trillion in what is known as “outputs,” i.e., the value of goods and services produced by the industry (see Table 2).⁵

4. Capacity measures how much crude oil refineries are able to process. Utilization measures how much is actually being processed (as a percentage of maximum capacity). 5. These projected amounts are in nominal U.S. dollars

Source: Author’s calculations using the IMPLAN modelling system. Details may not add up to totals due to rounding

Projected spending by the U.S. refining industry, 2024-2030

Figure 3 illustrates the industry’s projected annual spending between 2024 and 2030. Industry spending is expected to be US$58 billion in 2024, rising to US$62 billion by 2030. This includes operating expenditures (OPEX) and capital expenditures (CAPEX). Cumulatively, between 2024 and 2030, the industry is projected to spend over US$428 billion.⁶

6. These projected amounts are in nominal U.S. dollars and are calculated using the Rystad Energy UCube.

Source: Derived from Rystad Energy (2024), Service Market Solution

Conclusion

American refineries are critical to the country’s strategic interest. U.S. refineries are projected to spend more than $428 billion in the next seven years on operating and capital expenditures. The industries support millions of jobs. Canadian crude is an important part of the equation. It supplies more than 23 per cent of U.S. refinery feedstock.

Not only are Canadian crude oil supplies critical for the U.S. refining industry, but they are key to North American energy security. Limiting access to Canadian crude oil for U.S. refineries would require increased U.S. imports from less-free countries, which in turn would risk North American energy security.

References

Rystad Energy (2024), Service Market Solution <http://tinyurl.com/28fmv6a6>; U.S. Energy Information Administration (Undated), Oil and Petroleum Products Explained: Refining Crude Oil <http://tinyurl.com/3b2uwrxh>; U.S. Energy Information Administration (2023), Refinery Capacity Report <http://tinyurl.com/2s4ybz9z>; U.S. Energy Information Administration (2024a), Petroleum and Other Liquids: PADD District Imports by Country of Origin <http://tinyurl.com/58mzvtts>; U.S. Energy Information Administration (2024b), Petroleum and Other Liquids: Refinery Utilization and Capacity <http://tinyurl.com/3wx957k4>; U.S. Energy Information Administration (2024c), Petroleum and Other Liquids: U.S. Imports by Country of Origin <http://tinyurl.com/bdcsbwhn>; U.S. Environmental Protection Agency (Undated), Appendix A — Overview of Petroleum Refining, Proposed Clean Fuels Refinery DEIS <http://tinyurl.com/dveyzc8k>.

Alberta

The permanent CO2 storage site at the end of the Alberta Carbon Trunk Line is just getting started

Wells at the Clive carbon capture, utilization and storage project near Red Deer, Alta. Photo courtesy Enhance Energy

From the Canadian Energy Centre

Inside Clive, a model for reducing emissions while adding value in Alberta

It’s a bright spring day on a stretch of rolling farmland just northeast of Red Deer. It’s quiet, but for the wind rushing through the grass and the soft crunch of gravel underfoot.

The unassuming wellheads spaced widely across the landscape give little hint of the significance of what is happening underground.

In just five years, this site has locked away more than 6.5 million tonnes of CO₂ — equivalent to the annual emissions of about 1.5 million cars — stored nearly four CN Towers deep beneath the surface.

The CO₂ injection has not only reduced emissions but also breathed life into an oilfield that was heading for abandonment, generating jobs, economic activity and government revenue that would have otherwise been lost.

This is Clive, the endpoint of one of Canada’s largest carbon capture, utilization and storage (CCUS) projects. And it’s just getting started.

Rooted in Alberta’s first oil boom

Clive’s history ties to Alberta’s first oil boom, with the field discovered in 1952 along the same geological trend as the legendary 1947 Leduc No. 1 gusher near Edmonton.

“The Clive field was discovered in the 1950s as really a follow-up to Leduc No. 1. This is, call it, Leduc No. 4,” said Chris Kupchenko, president of Enhance Energy, which now operates the Clive field.

Over the last 70 years Clive has produced about 70 million barrels of the site’s 130 million barrels of original oil in place, leaving enough energy behind to fuel six million gasoline-powered vehicles for one year.

“By the late 1990s and early 2000s, production had gone almost to zero,” said Candice Paton, Enhance’s vice-president of corporate affairs.

“There was resource left in the reservoir, but it would have been uneconomic to recover it.”

Facilities at the Clive project. Photo courtesy Enhance Energy

Gearing up for CO2

Calgary-based Enhance bought Clive in 2013 and kept it running despite high operating costs because of a major CO2 opportunity the company was developing on the horizon.

In 2008, Enhance and North West Redwater Partnership had launched development of the Alberta Carbon Trunk Line (ACTL), one of the world’s largest CO2 transportation systems.

Wolf Midstream joined the project in 2018 as the pipeline’s owner and operator.

Completed in 2020, the groundbreaking $1.2 billion project — supported by the governments of Canada and Alberta — connects carbon captured at industrial sites near Edmonton to the Clive facility.

“With CO2 we’re able to revitalize some of these fields, continue to produce some of the resource that was left behind and permanently store CO2 emissions,” Paton said.

Map of the Alberta Carbon Trunk Line courtesy of Wolf Midstream

An oversized pipeline on purpose

Each year, about 1.6 million tonnes of CO2 captured at the NWR Sturgeon Refinery and Nutrien Redwater fertilizer facility near Fort Saskatchewan travels down the trunk line to Clive.

In a unique twist, that is only about 10 per cent of the pipeline’s available space. The project partners intentionally built it with room to grow.

“We have a lot of excess capacity. The vision behind the pipe was, let’s remove barriers for the future,” Kupchenko said.

The Alberta government-supported goal was to expand CCS in the province, said James Fann, CEO of the Regina-based International CCS Knowledge Centre.

“They did it on purpose. The size of the infrastructure project creates the opportunity for other emitters to build capture projects along the way,” he said.

CO2 captured at the Sturgeon Refinery near Edmonton is transported by the Alberta Carbon Trunk Line to the Clive project. Photo courtesy North West Redwater Partnership

Extending the value of aging assets

Building more CCUS projects like Clive that incorporate enhanced oil recovery (EOR) is a model for extending the economic value of aging oil and gas fields in Alberta, Kupchenko said.

“EOR can be thought of as redeveloping real estate,” he said.

“Take an inner-city lot with a 700-square-foot house on it. The bad thing is there’s a 100-year-old house that has to be torn down. But the great thing is there’s a road to it. There’s power to it, there’s a sewer connection, there’s water, there’s all the things.

“That’s what this is. We’re redeveloping a field that was discovered 70 years ago and has at least 30 more years of life.”

The 180 existing wellbores are also all assets, Kupchenko said.

“They may not all be producing oil or injecting CO2, but every one of them is used. They are our eyes into the reservoir.”

CO2 injection well at the Clive carbon capture, utilization and storage project. Photo for the Canadian Energy Centre

Alberta’s ‘beautiful’ CCUS geology

The existing wells are an important part of measurement, monitoring and verification (MMV) at Clive.

The Alberta Energy Regulator requires CCUS projects to implement a comprehensive MMV program to assess storage performance and demonstrate the long-term safety and security of CO₂.

Katherine Romanak, a subsurface CCUS specialist at the University of Texas at Austin, said that her nearly 20 years of global research indicate the process is safe.

“There’s never been a leak of CO2 from a storage site,” she said.

Alberta’s geology is particularly suitable for CCUS, with permanent storage potential estimated at more than 100 billion tonnes.

“The geology is beautiful,” Romanak said.

“It’s the thickest reservoir rocks you’ve ever seen. It’s really good injectivity, porosity and permeability, and the confining layers are crazy thick.”

Suitability of global regions for CO2 storage. Courtesy Global CCS Institute

CO2-EOR gaining prominence

The extra capacity on the ACTL pipeline offers a key opportunity to capitalize on storage potential while addressing aging oil and gas fields, according to the Alberta government’s Mature Asset Strategy, released earlier this year.

The report says expanding CCUS to EOR could attract investment, cut emissions and encourage producers to reinvest in existing properties — instead of abandoning them.

However, this opportunity is limited by federal policy.

Ottawa’s CCUS Investment Tax Credit, which became available in June 2024, does not apply to EOR projects.

“Often people will equate EOR with a project that doesn’t store CO2 permanently,” Kupchenko said.

“We like to always make sure that people understand that every ton of CO2 that enters this project is permanently sequestered. And we take great effort into storing that CO2.”

The International Energy Forum — representing energy ministers from nearly 70 countries including Canada, the U.S., China, India, Norway, and Saudi Arabia — says CO₂-based EOR is gaining prominence as a carbon sequestration tool.

The technology can “transform a traditional oil recovery method into a key pillar of energy security and climate strategy,” according to a June 2025 IEF report.

Drone view of the Clive project. Photo courtesy Enhance Energy

Tapping into more opportunity

In Central Alberta, Enhance Energy is advancing a new permanent CO2 storage project called Origins that is designed to revitalize additional aging oil and gas fields while reducing emissions, using the ACTL pipeline.

“Origins is a hub that’s going to enable larger scale EOR development,” Kupchenko said.

“There’s at least 10 times more oil in place in this area.”

Meanwhile, Wolf Midstream is extending the pipeline further into the Edmonton region to transport more CO2 captured from additional industrial facilities.

Canadian Energy Centre

Cross-Canada economic benefits of the proposed Northern Gateway Pipeline project

From the Canadian Energy Centre

Billions in government revenue and thousands of jobs across provinces

Announced in 2006, the Northern Gateway project would have built twin pipelines between Bruderheim, Alta. and a marine terminal at Kitimat, B.C.

One pipeline would export 525,000 barrels per day of heavy oil from Alberta to tidewater markets. The other would import 193,000 barrels per day of condensate to Alberta to dilute heavy oil for pipeline transportation.

The project would have generated significant economic benefits across Canada.

The following projections are drawn from the report Public Interest Benefits of the Northern Gateway Project (Wright Mansell Research Ltd., July 2012), which was submitted as reply evidence during the regulatory process.

Financial figures have been adjusted to 2025 dollars using the Bank of Canada’s Inflation Calculator, with $1.00 in 2012 equivalent to $1.34 in 2025.

Total Government Revenue by Region

Between 2019 and 2048, a period encompassing both construction and operations, the Northern Gateway project was projected to generate the following total government revenues by region (direct, indirect and induced):

British Columbia

- Provincial government revenue: $11.5 billion

- Federal government revenue: $8.9 billion

- Total: $20.4 billion

Alberta

- Provincial government revenue: $49.4 billion

- Federal government revenue: $41.5 billion

- Total: $90.9 billion

Ontario

- Provincial government revenue: $1.7 billion

- Federal government revenue: $2.7 billion

- Total: $4.4 billion

Quebec

- Provincial government revenue: $746 million

- Federal government revenue: $541 million

- Total: $1.29 billion

Saskatchewan

- Provincial government revenue: $6.9 billion

- Federal government revenue: $4.4 billion

- Total: $11.3 billion

Other

- Provincial government revenue: $1.9 billion

- Federal government revenue: $1.4 billion

- Total: $3.3 billion

Canada

- Provincial government revenue: $72.1 billion

- Federal government revenue: $59.4 billion

- Total: $131.7 billion

Annual Government Revenue by Region

Over the period 2019 and 2048, the Northern Gateway project was projected to generate the following annual government revenues by region (direct, indirect and induced):

British Columbia

- Provincial government revenue: $340 million

- Federal government revenue: $261 million

- Total: $601 million per year

Alberta

- Provincial government revenue: $1.5 billion

- Federal government revenue: $1.2 billion

- Total: $2.7 billion per year

Ontario

- Provincial government revenue: $51 million

- Federal government revenue: $79 million

- Total: $130 million per year

Quebec

- Provincial government revenue: $21 million

- Federal government revenue: $16 million

- Total: $37 million per year

Saskatchewan

- Provincial government revenue: $204 million

- Federal government revenue: $129 million

- Total: $333 million per year

Other

- Provincial government revenue: $58 million

- Federal government revenue: $40 million

- Total: $98 million per year

Canada

- Provincial government revenue: $2.1 billion

- Federal government revenue: $1.7 billion

- Total: $3.8 billion per year

Employment by Region

Over the period 2019 to 2048, the Northern Gateway Pipeline was projected to generate the following direct, indirect and induced full-time equivalent (FTE) jobs by region:

British Columbia

- Annual average: 7,736

- Total over the period: 224,344

Alberta

- Annual average: 11,798

- Total over the period: 342,142

Ontario

- Annual average: 3,061

- Total over the period: 88,769

Quebec

- Annual average: 1,003

- Total over the period: 29,087

Saskatchewan

- Annual average: 2,127

- Total over the period: 61,683

Other

- Annual average: 953

- Total over the period: 27,637

Canada

- Annual average: 26,678

- Total over the period: 773,662

The Quiet Invasion: How Transnational Crime and Chinese State Actors Infiltrated Vancouver and Eroded Canada’s Sovereignty

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

World Economic Forum Aims to Repair Relations with Schwab

-

Business7 hours ago

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

-

Alberta1 day ago

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

-

Crime19 hours ago

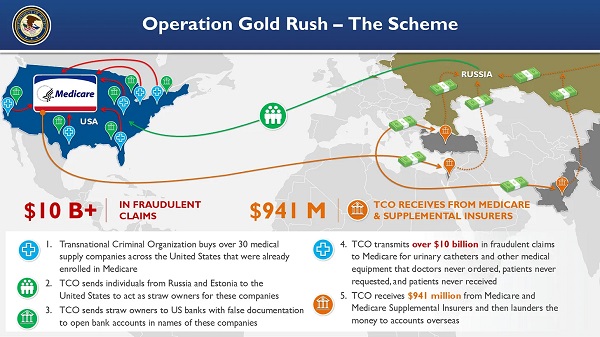

Crime19 hours agoNational Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Crime1 day ago

Crime1 day agoSuspected ambush leaves two firefighters dead in Idaho

-

Health19 hours ago

Health19 hours agoRFK Jr. Unloads Disturbing Vaccine Secrets on Tucker—And Surprises Everyone on Trump

-

Alberta1 day ago

Alberta1 day agoWhy the West’s separatists could be just as big a threat as Quebec’s

-

Business1 day ago

Business1 day agoCanada Caves: Carney ditches digital services tax after criticism from Trump

-

Bruce Dowbiggin1 day ago

Bruce Dowbiggin1 day agoThe Game That Let Canadians Forgive The Liberals — Again