Business

The CRTC said it would leave podcasts alone. Turns out that was a myth

From the MacDonald-Laurier Institute

This article originally appeared in the Hub.

By Peter Menzies, October 4, 2023

It’s clear the regulator is about to draw podcasts into its warm embrace.

The CRTC has backtracked on its promise to leave podcasts alone.

On May 12, the federal regulator stated in its “Myths and Facts” release that concerns it would regulate content such as podcasts were a “myth” and the “fact” of the matter was that “a person who creates audio or video content or creates a podcast, is not a broadcaster under” the Online Streaming Act (Bill C-11).

That “fact” didn’t live long. It expired September 29 when, in its first decisions since being granted authority over the internet, the CRTC changed lanes.

While it was careful to state that podcasters themselves don’t have to register with the Commission, the web-based platforms that make podcasts available must do so. Indeed, podcasters may not be broadcasters, but very much as predicted by the legislation’s critics, the CRTC has found ways to bring them into scope anyway.

It decided that podcasts constitute “programs under the Broadcasting Act, given that they are comprised of sounds intended to inform, enlighten or entertain.”

The regulator’s decision further explains that while podcasters may not be broadcasters, the transmission of podcasts over the internet most definitely “constitutes broadcasting” which makes those entities that platform podcasts into cable companies.

So while the CRTC concedes that while “the Broadcasting Act does not give the Commission a mandate to regulate creators of programs” it nevertheless makes clear that its powers do cover “those services that are involved in the broadcasting of programs, which are referred to as broadcasting undertakings.”

Is your head spinning yet?

The legal contortions continue throughout the decision, but the clear takeaway, the bottom line, is that, while it keeps insisting it doesn’t intend to regulate the content of podcasts, it is very concerned about the content of podcasts and if it can’t legally regulate them, it’ll make sure someone else does it for them.

Paragraph 223 of its decision makes it clear the CRTC is about to draw podcasts into its warm embrace.

Without information about online undertakings that transmit or retransmit podcasts, it would be more difficult for the Commission to ensure the achievement of the objectives of … the Broadcasting Act, which relate to, among other things, providing a reasonable opportunity for the public to be exposed to the expression of differing views on matters of public concern, and (that) the programming provided by the Canadian broadcasting system should be varied and comprehensive, providing a balance of information, enlightenment and entertainment for people of all ages, interests and tastes.

In other words, what the CRTC denounced as “myth” in the spring has become a “fact” in the fall. It has kicked open the door to the regulation of online content, if not directly then by proxy through the platforms that deliver the work of podcasters to their audiences.

It is a bureaucratic master stroke.

Here’s what will follow.

The list of intervenors presenting at the CRTC’s public hearing coming up in late November indicates the panel of commissioners will hear from a number of groups that will explain the extent to which they are under-represented and funded. So, a possible outcome of this will be that services that carry podcasts will have to fund podcasters who, on their own, haven’t been able to find an audience.

Just as likely is that platforms will be regulated to ensure podcasts designated by the CRTC are given priority visibility/discoverability online over undesignated podcasts through the manipulation of algorithms. These are likely to be podcasts by Indigenous, BIPOC and LGBTQ2S creators.

As erstwhile CRTC Chair Ian Scott told the Senate committee studying Bill C-11 in 2022:

Instead of saying, and the Act precludes this, we will make changes to your algorithms as many European countries are contemplating doing, instead, we will say this is the outcome we want. We want Canadians to find Canadian music. How best to do it? How will you do it? I don’t want to manipulate your algorithm. I want you to manipulate it to produce a particular outcome. And then we will have hearings to decide what are the best ways and explore it.

This was reinforced in an exchange Scott had with Senator Pamela Wallin, who suggested proponents of the bill were parsing their words and that:

You won’t manipulate the algorithms; you will make the platforms do it. That is regulation by another name. You’re regulating either directly and explicitly or indirectly, but you are regulating content.

To which Mr. Scott replied: “you’re right.”

The CRTC has now confirmed what it denied mere months ago when it was parroting then-Heritage Minister Pablo Rodriguez’s talking points.

It will make sure podcasts and any other internet content it can capture is regulated.

Peter Menzies is a Senior Fellow with the Macdonald-Laurier Institute, a former newspaper executive, and past vice chair of the CRTC.

Racket News

Racket News

By Eric Salzman

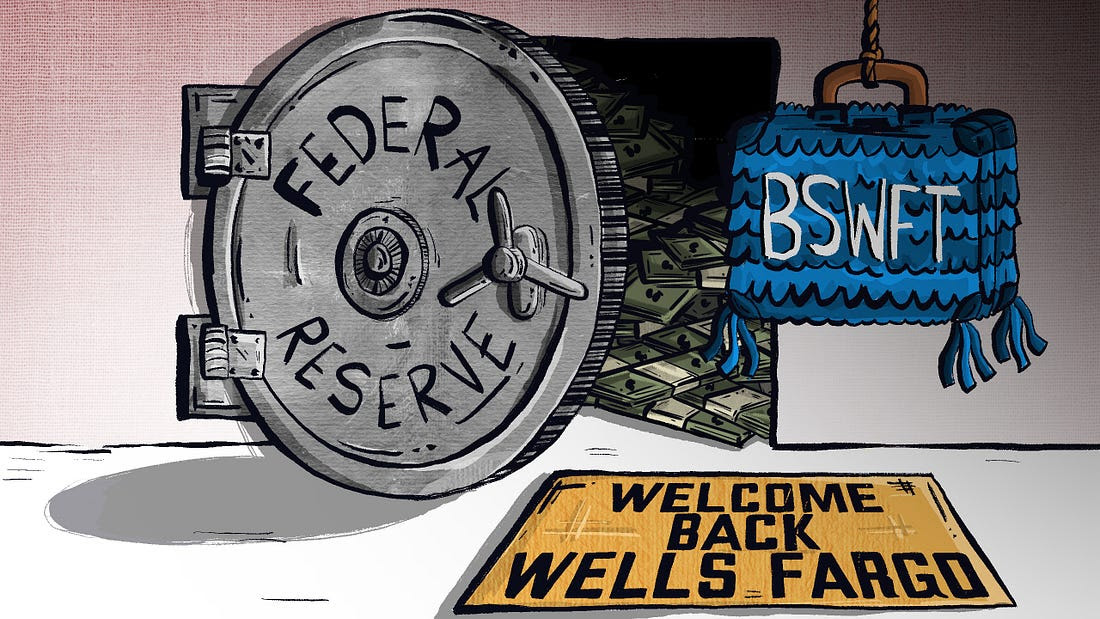

The heavyweight champion of financial crime gets seemingly its millionth chance to show it’s reformed

The past two decades have been tough ones for Wells Fargo and the many victims of its sprawling crime wave. While the banking industry is full of scammers, Wells took turning time honored street-hustles into multi-billion dollar white-collar hustles to a new level.

The Federal Reserve announced last month that Wells Fargo is no longer subject to the asset growth restriction the Fed finally enforced in 2018 after multiple scandals. This was a major enforcement action that prohibited Wells from growing existing loan portfolios, purchasing other bank branches or entering into any new activities that would result in their asset base growing.

Upon hearing the news that Wells was being released from the Fed’s penalty box, my mind turned to this pivotal moment in the classic movie “Slapshot.”

Here are some of Wells Fargo’s lowlights both before and after the Fed’s enforcement action:

- December 2022: Wells Fargo paid more than $2 billion to consumers and $1.7 billion in civil penalties after the Consumer Financial Protection Bureau (CFPB) found mismanagement — including illegal fees and interest charges — in several of its biggest product lines, such as auto loans, mortgages, and deposit accounts.

- September 2021: Wells Fargo paid $72.6 million to the Justice Department for overcharging foreign exchange customers from 2010-2017.

- February 2020: Wells Fargo paid $3 billion to settle criminal and civil investigations by the Justice Department and SEC into its aggressive sales practices between 2002 and 2016. About $500 million was eventually distributed to investors.

- January 2020: The Office of the Comptroller of the Currency (OCC) banned two senior executives, former CEO John Stumpf and ex-Head of Community Bank Carrie Tolstedt, from the banking industry. Stumpf and Tolstedt also incurred civil penalties of $17.5 million and $17 million.

- August 2018: The Justice Department levied a $2.09 billion fine on Wells Fargo for its actions during the subprime mortgage crisis, particularly its mortgage lending practices between 2005 and 2007.

- April 2018: Federal regulators at the CFPB and OCC examined Wells’ auto loan insurance and mortgage lending practices and ordered the bank to pay $1 billion in damages.

- February 2018: The aforementioned Fed enforcement action. In addition to the asset growth restriction, Wells was ordered to replace three directors.

- October 2017: Wells Fargo admitted wrongdoing after 110,000 clients were fined for missing a mortgage payment deadline — delays for which the bank was ultimately deemed at fault.

- July 2017: As many as 570,000 Wells Fargo customers were wrongly charged for auto insurance on car loans after the bank failed to verify whether those customers already had existing insurance. As a result, up to 20,000 customers may have defaulted on car loans.

- September 2016: Wells Fargo acknowledged its employees had created 1.5 million deposit accounts and 565,000 credit card accounts between 2002 and 2016 that “may not have been authorized by consumers,” according to CFPB. As a result, the lender was forced to pay $185 million in damages to the CFPB, OCC, and City and County of Los Angeles.

Additionally, somehow in 2023 Wells even managed to drop $1 billion in a civil settlement with shareholders for overstating their progress in complying with their 2018 agreement with the Fed to clean themselves up!

I imagine if Wells were in any other business, it wouldn’t be allowed to continue. But Wells is part of the “Too Big to Fail” club. Taking away its federal banking charter would be too disruptive for the financial markets, so instead they got what ended up being a seven-year growth ban. Not exactly rough justice.

While not the biggest settlement, my favorite Wells scam was the 2021 settlement of the seven-year pilfering operation, ripping off corporate customers’ foreign exchange transactions.

Like many banks, Wells Fargo offers its corporate clients with global operations foreign exchange (FX) services. For example, if a company is based in the U.S. but has extensive dealings in Canada, it may receive payments in Canadian dollars (CAD) that need to be exchanged for U.S. dollars (USD) and vice versa. Wells, like many banks, has foreign exchange specialists who do these conversions. Ideally, the banks optimize their clients’ revenue and decrease risk, in return for a markup fee, or “spread.”

There’s a lot of trust involved with this activity as the corporate customers generally have little idea where FX is trading minute by minute, nor do they know what time of day the actual orders for FX transactions — commonly called “BSwifts” — come in. For an unscrupulous bank, it’s a license to steal, which is exactly what Wells did.

According to the complaint, Wells regularly marked up transactions at higher spreads than what was agreed upon. This was just one of the variety of naughty schemes Wells used to clobber their customers. My two favorites were “The Big Figure Trick” and the “BSwift Pinata.”

The Big Figure Trick

Let’s say a client needs to sell USD for CAD, and that the $1 USD is worth $1.32 CAD. In banking parlance, the 32 cents is called the “Big Figure.” Wells would buy the CAD at $1.32 for $1 USD and then transpose the actual exchange rate on the customer statement from $1.32 to $1.23. If the customer didn’t notice, Wells would pocket the difference. On a transaction where the client is buying 5 million CAD with USD, the ill-gotten gain for Wells would be about $277,000 USD!

Conversely, if the customer did notice the difference, Wells would just blame it on the grunts in its operational back office, saying they accidentally transposed the number and “correct” the transaction. From the complaint, here is some give and take between two Wells FX specialists:

“You can play the transposition error game if you get called out.” Another FX sales specialist noted to a colleague about a previous transaction that a customer “didn’t flinch at the big fig the other day. Want to take a bit more?”

The BSwift Piñata

The way this hustle would work is, let’s say the Wells corporate customer was receiving payment from one of their Canadian clients. The Canadian client’s bank would send a BSwift message to Wells. The Wells client was in the dark about the U.S. dollar-Canadian dollar exchange rate because it had no idea what time of day the message arrived. Wells took advantage of that by purchasing U.S. dollars for Canadian dollars first. For simplicity, think of the U.S. dollar-Canadian dollar exchange rate as a widget that Wells bought for $1. If the widget increased in value, say to $1.10 during the day, Wells would sell the widget they purchased for $1 to the client for $1.10 and pocket 10 cents. If the price of the widget Wells bought for $1 fell to 95 cents, Wells would just give up their $1 purchase to the client, plus whatever markup they agreed to.

Heads, Wells wins. Tails, client loses.

The complaint notes that a Wells FX specialist wrote that he:

“Bumped spreads up a pinch,” that “these clients who are in the mode of just processing wires will most likely not notice this slight change in pricing” and that it “could have a very quick positive impact on revenue without a lot of risk.”

Talk about a boiler room operation. Personally, I think calling what you are doing to a client a “piñata” should have easily put Wells in the Fed’s penalty box another 5 years at least!

Wells has been released from the Fed’s 2018 enforcement order. I would like to think they have learned their lesson and are reformed, but I would lay good odds against it. A leopard can’t change its spots.

Racket News is a reader-supported publication.

Consider becoming a free or paid subscriber.

Alberta

Pierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

From Pierre Poilievre

The Quiet Invasion: How Transnational Crime and Chinese State Actors Infiltrated Vancouver and Eroded Canada’s Sovereignty

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

-

Business2 days ago

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

-

Business19 hours ago

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

-

Censorship Industrial Complex2 days ago

Censorship Industrial Complex2 days agoGlobal media alliance colluded with foreign nations to crush free speech in America: House report

-

Alberta14 hours ago

Alberta14 hours agoAlberta Provincial Police – New chief of Independent Agency Police Service

-

Opinion10 hours ago

Opinion10 hours agoBlind to the Left: Canada’s Counter-Extremism Failure Leaves Neo-Marxist and Islamist Threats Unchecked

-

Alberta18 hours ago

Pierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

-

Business2 days ago

Business2 days agoElon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

-

COVID-1912 hours ago

COVID-1912 hours agoTop COVID doctor given one of Canada’s highest honors