Business

Spending sprees by governments across Canada help fuel inflation and high interest rates

From the Fraser Institute

By Jake Fuss and Grady Munro

While the prime minister and many premiers justified their high spending levels during the pandemic as merely a temporary development, the federal government and seven provincial governments still plan to run budget deficits this year

Earlier this year, premiers in Ontario, British Columbia, and Newfoundland and Labrador wrote letters to Tiff Macklem, Governor of the Bank of Canada, cautioning against further interest rate hikes, citing the potential negative effects on residents including homeowners with mortgages. But instead of blaming the central bank, Canadian premiers—and the prime minister—should stop their spending sprees, which help fuel inflation and increase interest rates.

Indeed, when governments increase spending, particularly when financed by debt, they add more money to the economy and can help fuel inflation. And high rates of government spending put pressure on the Bank of Canada to maintain interest rates at current levels, or even hike the rate further, to counteract inflation. According to a recent report from Scotiabank, government spending has contributed significantly to higher interest rates in Canada, accounting for an estimated 42 per cent of the increase in the Bank of Canada’s rate since the first quarter of 2022.

Yet the spending sprees continue.

While the prime minister and many premiers justified their high spending levels during the pandemic as merely a temporary development, the federal government and seven provincial governments still plan to run budget deficits this year. Government spending across the country remains at elevated levels or, in some cases, even increased beyond pandemic levels.

Ontario is a prime example. Provincial program spending (total spending minus interest costs) will reach an estimated $193.0 billion in 2023/24—$24.0 billion more than at the peak of COVID. Debt interest costs have also grown due to debt accumulation and rising interest rates.

Despite a considerable increase in revenue over recent years, the Ford government had planned for a $1.3 billion deficit in its spring budget. By November, the government increased spending again and quadrupled the projected deficit to $5.6 billion.

Similarly, British Columbia outlined plans in February to increase program spending and run a $4.2 billion deficit while adding $13.1 billion in debt to the books this year. Just over a half-year later, the B.C. government increased spending again and the deficit was revised to $5.6 billion with debt rising by $14.0 billion instead of $13.1 billion.

Prime Minister Trudeau and his government followed a similar path. According to the recent federal fiscal update, between 2024/25 and 2027/28, the government has increased projected spending by $30.7 billion more than previously forecasted.

According to projections, only two provinces (Alberta and New Brunswick) will run budget surpluses this year, but in Alberta this is largely due to elevated resource revenues stemming from high commodity prices rather than any significant spending restraint. If resource revenues declined to historical average levels, the Smith government in Alberta would likely run deficits similar to other provinces.

Simply put, the excessive spending habits of many premiers and the prime minister are a big reason why interest rates have climbed and inflation remains sticky.

If Canadian politicians want to help tame inflation and bring down interest rates, they should look in the mirror for solutions and show leadership. Complaining about elevated interest rates helps no one, but ensuring fiscal policy is rowing in the same direction as monetary policy would be a good start.

Authors:

This article supplied by Troy Media.

![]() By Lee Harding

By Lee Harding

Ottawa is targeting the charitable tax status of faith-based groups. The fallout could hit every Canadian community

The possibility that Canadian religious organizations will lose their charitable status has never been more real.

On Jan. 6, Parliament’s Standing Committee on Finance recommended numerous changes, including Recommendation 430: “Amend the Income Tax Act to define a charity, which would remove the privileged status of ‘advancement of religion’ as a

charitable purpose, meaning faith-based organizations could lose access to tax benefits.”

The B.C. Humanist Association, a secular advocacy group, has long advocated for removing religion as a stand-alone charitable purpose. That idea is reflected in Recommendation 430. Before adopting such a proposal, the finance committee should have reviewed a study published last November by Cardus, a Canadian think tank focused on faith, civil society and public policy.

The Cardus study examined 64 Christian congregations in various provinces to assess the socio-economic value of their impact. It suggested that congregations make an $18.2-billion socioeconomic contribution to Canadian society, well in excess of tax exemptions and rebates equal to $1.7 billion. The net positive result of $16.5 billion—a “halo effect”—is more than 10

times the value of the tax exemptions.

The implications are clear: society will be worse off if the loss of religious charitable status leads to a drop of more than 10 per cent in donations to affected charities. Why risk it?

When congregations unravel, society follows in ways that go beyond mere economics. As Cardus explains, churches often provide space, often at no cost or below-market rates, for cultural and artistic events, recreation and sports, education, social services and other community activities. They also deliver addiction recovery, counselling and mental-health support, child care, refugee sponsorship and settlement services for newcomers, education and food banks.

Whether institutionally or personally, helping people is often an integral extension of religious belief. A 2012 Statistics Canada study found that the 14 per cent of Canadians who attend church weekly offer 29 per cent of the nation’s volunteer hours and provide 45 per cent of all charitable donations.

No party has explicitly endorsed removing charitable status for religion. But the Bloc Québécois, NDP and Liberals dominated the committee recommendation to remove religion as a charitable purpose. The Conservative Party, which held a minority on the committee, was alone in opposing it outright.

Randy Crosson, executive director of Freedoms Advocate, is organizing a national pushback. In a speech given Oct. 1 to the Regina Civic Awareness and Action Network, he said the recommendation was a “shot across the bow” to gauge public reaction.

“This isn’t just about donors losing tax receipts. It’s about churches losing buildings, staff losing jobs, and ministries being forced to shut down due to reduced donations. This is a direct threat to the future of faith in Canada, and it’s happening fast,” Crosson explained in an online video.

Crosson said religion enjoys less participation and more opposition than in previous decades. Church attendance has slumped since the pandemic, and some Canadians continue to criticize churches for their historical involvement in residential schools.

The Quebec government has also pursued a strongly secular approach to public policy. In 2019, Quebec’s Bill 21 used the notwithstanding clause of the Constitution to ban public servants from wearing religious symbols, such as hijabs, turbans or crucifixes. In August, Quebec’s secularism minister, Jean François Roberge, said that the “proliferation of street prayer is a serious and sensitive issue” and promised to bring legislation to ban it.

That’s why Crosson is urging religious leaders to launch a three-part campaign.

“First, an open letter drafted with legal and faith leaders to show government and the media the real value of the church in Canadian society. Second, mass signatures. We need churches, leaders and individuals to sign the letter,” Crosson says in a video appeal. “And third, a national documentary based on the open letter. This will be released publicly and spread through churches, media and social platforms.”

The Frontier Centre for Public Policy has also come out publicly against the proposed change. A report by Senior Fellow Pierre Gilbert entitled Revoking the Charitable Status for the Advancement of Religion: A Critical Assessment makes a case for the status quo, pointing to benefits such as those mentioned above.

For now, at least, the idea is on hold. A published email response by Liberal MP Karina Gould, the chair of the House of Commons’ Standing Committee on Finance, said the charitable status of faith-driven non-profits will not be revoked in the Nov. 4 budget.

That’s good news. Faith is a big motivator of charity, and it’s hard to see how a less charitable society is a better one. If governments want to balance the books, they should rein in spending, not put faith-based charities at risk.

Lee Harding is a research fellow for the Frontier Centre for Public Policy.

Troy Media empowers Canadian community news outlets by providing independent, insightful analysis and commentary. Our mission is to support local media in helping Canadians stay informed and engaged by delivering reliable content that strengthens community connections and deepens understanding across the country

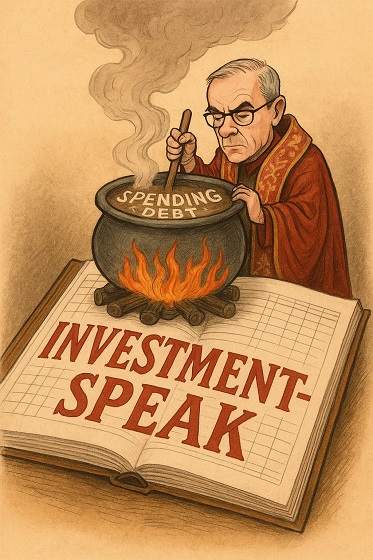

The trick lies in the word “investment.” By separating “operational spending” from “capital investment,” Ottawa can now reclassify expenditures, moving them from one column to another without changing the underlying reality. A deficit remains a deficit.

Next week, Ottawa will table its first budget in nearly two years. The government has already told us what to expect. In October, the Department of Finance announced a new “Capital Budgeting Framework” that would allow Canada to “spend less so it can invest more.” The phrasing sounds prudent. It is not. It is a linguistic sleight of hand designed to obscure what the government is actually doing: spending more while pretending to exercise restraint.

The older meanings of the two words reveal the moral inversion. To spend, from the Latin dispendere, meant to weigh out and let go. It implied the careful release of what one possessed, whether money, time, or energy. In Old English and Middle English, to “spend” one’s life or strength was to pour it out, knowingly and finitely. There was gravity to the act; what was spent was gone. To invest, by contrast, came from the Latin investīre: to clothe or cover. Before it became a financial term, it referred to the ceremonial act of placing robes upon a monarch or knight, endowing them with office or honour. In its financial sense, to invest was to “clothe money” in a venture, expecting return. The first word carried finality; the second, expectancy. Spending ended a possession; investing disguised it in the promise of future gain.

From these roots, the moral difference is clear. Spending belongs to the household, measured, finite, and real. Investing belongs to the court, symbolic, ceremonial, and often self-flattering. When a government calls its spending “investment,” it does not change the transaction; it changes the costume.

The gradual adoption of this vocabulary by governments is an old habit dressed as innovation. For two decades, Ottawa has been learning to speak the language of investment as disguise. Budgets that once tabulated “program spending” now announce “investments in Canadians.” Under the Trudeau governments, tax credits and subsidies were cast as “investments in innovation.” The Canada Infrastructure Bank was sold as “leveraging private investment” rather than public debt. Even emergency COVID programs were justified as “investing in recovery.” The word became a universal solvent, dissolving distinctions between cost, borrowing, and speculation.

This year’s government has merely made the trend official. In October, the Department of Finance released Modernizing Canada’s Budgeting Approach, explaining that the new Capital Budgeting Framework would “distinguish day-to-day operational spending from capital investment.” The document asserts that this will “guide decisions and help prioritize. The trick lies in the word “investment.” By separating “operational spending” from “capital investment,” Ottawa can now reclassify expenditures, moving them from one column to another without changing the underlying reality. A deficit remains a deficit. Borrowed money is still borrowed. But call it investment, and suddenly it carries the glow of foresight and responsibility. The government plans to balance its operating budget while continuing to borrow for capital projects. The ledger will grow, but the language will comfort.

This is not merely bad accounting. It is a deliberate corruption of language in service of political evasion. And it reveals something deeper about how modern governments govern: not through honest argument but through the manipulation of words.

Ottawa has been perfecting this costume for two decades. Budgets that once listed “program spending” now announce “investments in Canadians.” Tax credits became “investments in innovation.” The Canada Infrastructure Bank was sold as “leveraging private investment,” not public debt. COVID emergency programs were justified as “investing in recovery.” The word became a universal solvent, dissolving the distinction between cost, borrowing, and speculation.

This year’s framework makes the habit official. The October document from Finance Canada promises that the new approach will “guide decisions and help prioritize investments that generate long-term benefits for Canadians, such as major projects, housing, clean energy, and infrastructure.” The tone is managerial and assured. The assumption goes unexamined: that one can divide the public purse into virtuous investment and wasteful spending, and that the government possesses the wisdom to know the difference.

Haultain Research is a reader-supported publication.

To receive new posts and support our work, consider becoming a donor or a paid subscriber.

The Prime Minister echoed the line in his own announcement: “Budget 2025 will set out our plan to spend less so we can invest more in Canada’s long-term growth.” Read carefully, the statement reveals its own dishonesty. To “spend less” no longer means reducing outlays. It means shifting expenditures into a different category where they escape the stigma of cost. The government intends to continue borrowing, but it will refer to that borrowing by a supposedly more respectable name.

The definition of capital investment is conveniently broad. It includes tax credits, corporate subsidies, and nearly any policy “that contributes to capital formation.” The Fraser Institute and others have warned that this expansiveness allows Ottawa to reclassify politically favored programs as investment, inflating the appearance of fiscal discipline while reducing transparency. A deficit becomes a “generational investment.” A subsidy becomes a “partnership.” Waste is rebranded as “capacity-building.” The language does the work that policy cannot.

Recent history exposes the fraud. Consider the electric vehicle battery subsidies, heralded as “historic investments” in the green economy. Tens of billions were promised. Projects have stalled, been postponed, or quietly abandoned. The so-called green slush fund, officially presented as an investment vehicle for sustainable innovation, turned out to be a network of cronyism and waste. These, too, were dressed as investments. When their failures emerged, the language remained untouched, as though incompetence and corruption could not breach the sanctity of the term.

The alchemy works because language shapes perception faster than arithmetic. “Investment” suggests prudence and reward. “Spending” suggests indulgence and loss. Citizens hear that the government is “investing in Canadians” and imagine return, not depletion. The moral weight of the word does the political work. Accountability fades behind aspiration.

There is a deeper danger here. Words like spend and cost belong to the vocabulary of limits. They remind us that government operates with other people’s money. Invest, as politicians now use it, belongs to the vocabulary of boundless promise. It implies benevolence without constraint, as though the state were a benefactor rather than a borrower. When the government claims to “invest in Canadians,” it implies ownership of the very people whose money it spends. The inversion of subject and object is telling. It reveals the paternalism at the heart of modern technocracy.

George Orwell wrote that political language “is designed to make lies sound truthful and murder respectable.” He understood that the corruption of speech precedes the corruption of thought. When a government renames its spending as investment, it is not simply misdescribing an accounting category. It is reshaping the citizen’s perception of what government may do. If all spending is investment, then any limit on it seems stingy, even immoral. The citizen becomes debtor to a future defined by the state.

The deceit is subtle. No one disputes that bridges or power grids can be sound investments. The deceit lies in the implication that all government activity now yields return, that every expense is productive, every grant visionary. By this logic, no spending is considered waste and no deficit is deemed reckless, as long as it is labelled as an investment. The language abolishes the distinction between consumption and creation, between present sacrifice and future gain. In doing so, it abolishes prudence itself.

Prudence, in the older sense, is not caution for its own sake. It is moral realism: the recognition that resources are finite and choices have costs. The new investment rhetoric invites the opposite illusion. Money, once moralized as investment, appears to carry no weight of trade-off. Ottawa can clothe profligacy in the robes of responsibility. The government that promises to “spend less and invest more” is like a man claiming to drink less whiskey by pouring it into crystal.

The cost of this linguistic vanity is not only fiscal. It corrodes public trust. Citizens sense the dissonance. Deficits widen, taxes climb, promises multiply. When language becomes a substitute for honesty, cynicism follows. A people that cannot trust its government’s words cannot trust its numbers.

The remedy is simple, though seldom easy: call things by their names. Spending is spending, whether on roads, welfare, or research. Some are wise, some are foolish. But none becomes virtuous by relabeling. The duty of government is not to invent euphemisms but to justify expenditures plainly and bear the consequences. That is what accountability means.

Roger Scruton observed that conservatism, properly understood, is “the politics of the tried and tested against the politics of experiment.” In fiscal speech, that means preferring accuracy to allure. A government confident in its stewardship would not fear plain-spoken spending. Only one uneasy with its own excess needs the comfort of investment.

Ottawa’s linguistic reform is therefore not a matter of diction. It is an attempt to alter reality through language, to convert liability into virtue by decree. The danger is that citizens, lulled by investment-speak, will cease to notice the arithmetic beneath. The numbers will grow; the language will glow. By the time the robe is lifted, the treasury will be bare.

That is not a forecast. It is a warning. When governments clothe waste in the garments of investment, they are not modernizing accounting. They are modernizing deceit.

We are grateful that you’re reading an article from Haultain Research.

For the full experience, and to help us bring you more quality research and commentary,

CAPP calls on federal government to reset energy policy before it’s too late

Premier Smith sending teachers back to school and setting up classroom complexity task force

RCMP Bust Industrial-Scale Superlab Outside Toronto

Carney speech highlights how easily newsrooms are played by politicians announcing the same things over and over again

-

National19 hours ago

National19 hours agoCanadian MPs order ethics investigation into Mark Carney’s corporate interests

-

Business2 days ago

Business2 days agoCanada has given $109 million to Communist China for ‘sustainable development’ since 2015

-

Banks24 hours ago

Banks24 hours agoBank of Canada Cuts Rates to 2.25%, Warns of Structural Economic Damage

-

Opinion2 days ago

Opinion2 days agoBritish Columbians protest Trump while Eby brings their province to its knees

-

Business1 day ago

Business1 day agoFord’s Liquor War Trades Economic Freedom For Political Theatre

-

International2 days ago

International2 days agoStrongest hurricane in 174 years makes landfall in Jamaica

-

Alberta14 hours ago

Alberta14 hours agoNobel Prize nods to Alberta innovation in carbon capture

-

Business1 day ago

Business1 day agoBill Gates walks away from the climate cult