Banks

International Monetary Fund paper suggests CBDCs could turn society cashless

From LifeSiteNews

A working paper by the International Monetary Fund suggests that cash may disappear from society entirely once central bank digital currencies become mainstream.

Digital currencies like CBDCs could make cash extinct, whether by design or through market preference, according to an IMF working paper.

With widespread digital currency adoption, cash may go the way of the dodo bird, and it would be “challenging and costly” to revive it if a society were to go fully cashless, according to the IMF working paper, Could Digital Currencies Lead to the Disappearance of Cash from the Market? by Marco Pani and Rodolfo Maino.

The disappearance of cash, according to the authors, could come about either through direct policy or as a natural part of innovation and digital currency adoption.

They say that “the introduction of a DC [Digital Currency] in a diverse payment ecosystem—comprising cash, traditional payment cards, and modern electronic money—where the use of physical cash has already declined significantly, could lead to the complete disappearance of cash, even if such an outcome were not an intentional policy objective.”

READ: Financial expert warns all-digital monetary system would enable ‘complete control’ of citizens

The authors looked at how merchants and customers use physical cash and cards, and simulated how the introduction of digital currencies could either complement cash and cards or wipe them out completely.

According to the report, the introduction of a new currency can alter the market equilibrium in several qualitatively different ways:

- It may displace one of the exiting currencies (either cash or cards);

- It may replace both currencies; or

- It may continue to be used indefinitely alongside the other two currencies.

"You could have a potentially […] darker world where the government decides that [CBDC] can be used to purchase some things, but not other things that it deems less desirable like say ammunition, or drugs, or pornography, or something of the sort": Eswar Prasad, WEF #AMNC23 pic.twitter.com/KkWgaEWAR5

— Tim Hinchliffe (@TimHinchliffe) June 28, 2023

Programmable digital currencies like Central Bank Digital Currencies (CBDCs) cannot operate without pegging every user to a digital identity.

What’s more, these programmable digital currencies can be controlled remotely, so that taxes and fines could automatically be taken out of accounts, or so that restrictions could be placed on what you could buy, where you could buy it and when.

Last year, the IMF published a policy brief acknowledging that CBDCs could be used for state surveillance while posing risks to privacy and cybersecurity that could undermine trust in central bank money.

According to the November 2024 IMF brief, Central Bank Digital Currency: Progress And Further Considerations:

CBDC, as a digital form of central bank money, may allow for a ‘digital trail’—data—to be accessed, collected, processed and stored.

In contrast to cash, CBDC could be designed to potentially include a wealth of personal data encapsulating transaction histories, user demographics, and behavioral patterns.

Personal data could establish a link between counterparty identities and transactions.

While the IMF acknowledges the risks to privacy, the potential for government surveillance, and how public and private entities could leverage user data for nefarious means, it is still plowing ahead with a CBDC Handbook for central banks and governments to follow during their rollouts.

READ: International Monetary Fund ‘working hard’ on a global Central Bank Digital Currency platform

The IMF consistently says that digital currencies should be complementary to physical cash and to not replace it, but all signs point towards the erosion of cash over time, whether through convenience or coercion — carrot or stick.

Speaking at the World Economic Forum’s (WEF) Special Meeting on Global Collaboration, Growth and Energy Development last year, Central Bank of Bahrain governor Khalid Humaidan told the panel “Open Forum: The Digital Currencies’ Opportunity in the Middle East” that one of the goals of CBDC was to replace cash, at least in Bahrain, and to go “one hundred percent digital.”

"We're probably going to stop calling it central bank digital currency [CBDC]. It's going to be a digital form of cash, and at some point in time hopefully we will be able to be 100% digital": Central Bank of Bahrain Governor Khalid Humaidan to the WEF https://t.co/Pspr0M1Uuq pic.twitter.com/N5aOkCpzh1

— Tim Hinchliffe (@TimHinchliffe) April 29, 2024

“If we think cash is the analogue and digital currency is the form of digital — CBDC is the digital form of cash — today, clearly we’re in a hybrid situation; we’re using both,” said Humaidan.

We know in the past when it comes to cash, central bankers were very much in control with all aspects of cash, and now we’re comfortable to the point where the private sector plays a big role in the printing of the cash, in the distribution of the cash, and with the private sector we use interest rates to manage the supply of cash.

The same thing is likely to happen with CBDC. Yes, the central bank will have a role, but at some point in time — the same way we don’t call it ‘central bank cash’ — we’re probably going to stop calling it central bank digital currency.

It’s going to be a digital form of the cash, and at some point in time hopefully we will be able to be one hundred percent digital.

"Is it [digital euro] going to be as private as cash? No. A digital currency will never be as anonymous and as protecting of privacy in many respects as cash, which is why cash will always be around": Christine Lagarde, BIS Innovation Summit, March 2023 #CBDC pic.twitter.com/BLMVOPax6a

— Tim Hinchliffe (@TimHinchliffe) April 11, 2023

While the IMF advises to not eliminate cash altogether, central banks and governments are already moving in that direction.

Furthermore, a WEF Agenda blog post from September, 2017 lists the “gradual obsolescence of paper currency” as being “characteristic of a well-designed CBDC.”

If cash were to go extinct, the latest IMF working paper warns, “reintroducing cash in a non-cash system would be challenging and costly.”

Therefore, the authors conclude:

To safeguard the continued utilization of cash and to uphold the equilibrium of the payment system, the study advocates for a proactive policy approach and for the implementation of measures aimed at ensuring the sustained relevance of physical currency, especially in scenarios where the introduction of new digital currencies might inadvertently lead to the extinction of traditional cash.

The IMF working paper Could Digital Currencies Lead to the Disappearance of Cash from the Market? was published on the IMF website in March 2025; however, the paper was first published in the International Advances in Economic Research journal on February 19, 2024 under its original title, Could CBDCs Lead to Cash Extinction? Insights from a ‘Merchant-Customer’ Model.

Reprinted with permission from The Sociable.

Note from LifeSiteNews co-founder Steve Jalsevac: This article is a must-read and view for all readers because of the profound personal impact a digital economy would have on every individual and every family.

The great Catherine Austin Fitts has strongly recommended that every citizen use cash as much as possible for purchases. She says that if millions did this, it would delay, if not stop, a forced digital economy. She should know. Fitts emphasizes, “In a highly leveraged financial system such as we have, a single individual counts for a lot.”

See her article, I Want to Stop CBDCs – What Can I Do

The increased use of credit and debit cards, including phone and other digital payment systems, is tempting because of their convenience. Still, it is also your cooperation in building your economic prison and total control of all that you say and do, where and when you travel, what you buy or subscribe to, and so on. We are facing a totalitarian control that has never before been experienced in human history. It is beyond frightening.

Carrying and using cash for purchases, and refusing to purchase anything from shops, restaurants or other services that do not accept cash or checks, is inconvenient and requires a little effort, commitment and some degree of courage.

Racket News

Racket News

By Eric Salzman

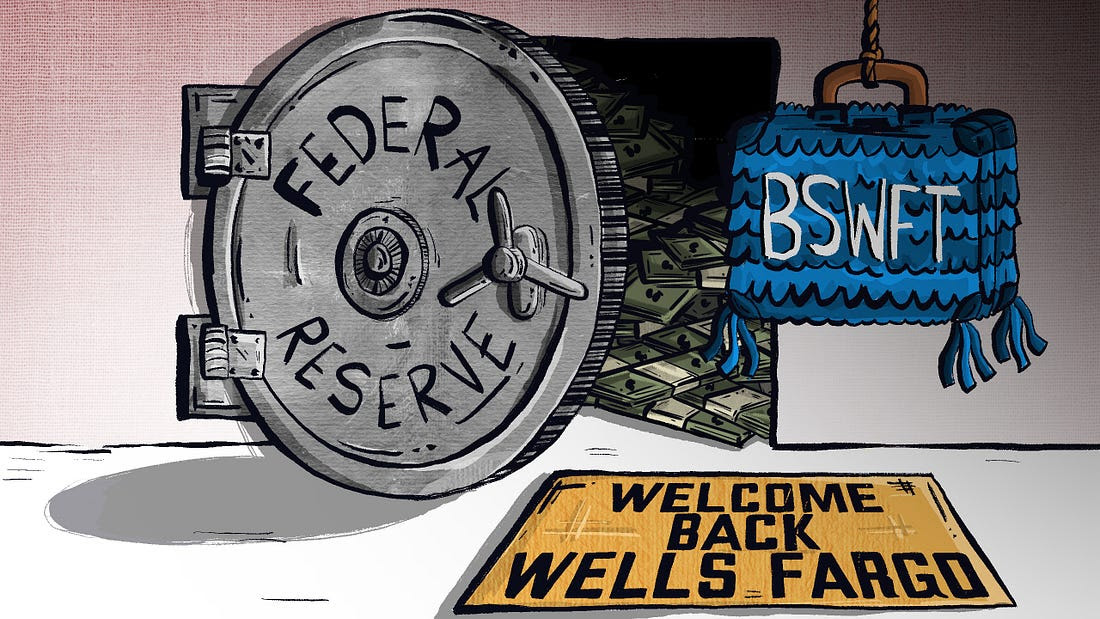

The heavyweight champion of financial crime gets seemingly its millionth chance to show it’s reformed

The past two decades have been tough ones for Wells Fargo and the many victims of its sprawling crime wave. While the banking industry is full of scammers, Wells took turning time honored street-hustles into multi-billion dollar white-collar hustles to a new level.

The Federal Reserve announced last month that Wells Fargo is no longer subject to the asset growth restriction the Fed finally enforced in 2018 after multiple scandals. This was a major enforcement action that prohibited Wells from growing existing loan portfolios, purchasing other bank branches or entering into any new activities that would result in their asset base growing.

Upon hearing the news that Wells was being released from the Fed’s penalty box, my mind turned to this pivotal moment in the classic movie “Slapshot.”

Here are some of Wells Fargo’s lowlights both before and after the Fed’s enforcement action:

- December 2022: Wells Fargo paid more than $2 billion to consumers and $1.7 billion in civil penalties after the Consumer Financial Protection Bureau (CFPB) found mismanagement — including illegal fees and interest charges — in several of its biggest product lines, such as auto loans, mortgages, and deposit accounts.

- September 2021: Wells Fargo paid $72.6 million to the Justice Department for overcharging foreign exchange customers from 2010-2017.

- February 2020: Wells Fargo paid $3 billion to settle criminal and civil investigations by the Justice Department and SEC into its aggressive sales practices between 2002 and 2016. About $500 million was eventually distributed to investors.

- January 2020: The Office of the Comptroller of the Currency (OCC) banned two senior executives, former CEO John Stumpf and ex-Head of Community Bank Carrie Tolstedt, from the banking industry. Stumpf and Tolstedt also incurred civil penalties of $17.5 million and $17 million.

- August 2018: The Justice Department levied a $2.09 billion fine on Wells Fargo for its actions during the subprime mortgage crisis, particularly its mortgage lending practices between 2005 and 2007.

- April 2018: Federal regulators at the CFPB and OCC examined Wells’ auto loan insurance and mortgage lending practices and ordered the bank to pay $1 billion in damages.

- February 2018: The aforementioned Fed enforcement action. In addition to the asset growth restriction, Wells was ordered to replace three directors.

- October 2017: Wells Fargo admitted wrongdoing after 110,000 clients were fined for missing a mortgage payment deadline — delays for which the bank was ultimately deemed at fault.

- July 2017: As many as 570,000 Wells Fargo customers were wrongly charged for auto insurance on car loans after the bank failed to verify whether those customers already had existing insurance. As a result, up to 20,000 customers may have defaulted on car loans.

- September 2016: Wells Fargo acknowledged its employees had created 1.5 million deposit accounts and 565,000 credit card accounts between 2002 and 2016 that “may not have been authorized by consumers,” according to CFPB. As a result, the lender was forced to pay $185 million in damages to the CFPB, OCC, and City and County of Los Angeles.

Additionally, somehow in 2023 Wells even managed to drop $1 billion in a civil settlement with shareholders for overstating their progress in complying with their 2018 agreement with the Fed to clean themselves up!

I imagine if Wells were in any other business, it wouldn’t be allowed to continue. But Wells is part of the “Too Big to Fail” club. Taking away its federal banking charter would be too disruptive for the financial markets, so instead they got what ended up being a seven-year growth ban. Not exactly rough justice.

While not the biggest settlement, my favorite Wells scam was the 2021 settlement of the seven-year pilfering operation, ripping off corporate customers’ foreign exchange transactions.

Like many banks, Wells Fargo offers its corporate clients with global operations foreign exchange (FX) services. For example, if a company is based in the U.S. but has extensive dealings in Canada, it may receive payments in Canadian dollars (CAD) that need to be exchanged for U.S. dollars (USD) and vice versa. Wells, like many banks, has foreign exchange specialists who do these conversions. Ideally, the banks optimize their clients’ revenue and decrease risk, in return for a markup fee, or “spread.”

There’s a lot of trust involved with this activity as the corporate customers generally have little idea where FX is trading minute by minute, nor do they know what time of day the actual orders for FX transactions — commonly called “BSwifts” — come in. For an unscrupulous bank, it’s a license to steal, which is exactly what Wells did.

According to the complaint, Wells regularly marked up transactions at higher spreads than what was agreed upon. This was just one of the variety of naughty schemes Wells used to clobber their customers. My two favorites were “The Big Figure Trick” and the “BSwift Pinata.”

The Big Figure Trick

Let’s say a client needs to sell USD for CAD, and that the $1 USD is worth $1.32 CAD. In banking parlance, the 32 cents is called the “Big Figure.” Wells would buy the CAD at $1.32 for $1 USD and then transpose the actual exchange rate on the customer statement from $1.32 to $1.23. If the customer didn’t notice, Wells would pocket the difference. On a transaction where the client is buying 5 million CAD with USD, the ill-gotten gain for Wells would be about $277,000 USD!

Conversely, if the customer did notice the difference, Wells would just blame it on the grunts in its operational back office, saying they accidentally transposed the number and “correct” the transaction. From the complaint, here is some give and take between two Wells FX specialists:

“You can play the transposition error game if you get called out.” Another FX sales specialist noted to a colleague about a previous transaction that a customer “didn’t flinch at the big fig the other day. Want to take a bit more?”

The BSwift Piñata

The way this hustle would work is, let’s say the Wells corporate customer was receiving payment from one of their Canadian clients. The Canadian client’s bank would send a BSwift message to Wells. The Wells client was in the dark about the U.S. dollar-Canadian dollar exchange rate because it had no idea what time of day the message arrived. Wells took advantage of that by purchasing U.S. dollars for Canadian dollars first. For simplicity, think of the U.S. dollar-Canadian dollar exchange rate as a widget that Wells bought for $1. If the widget increased in value, say to $1.10 during the day, Wells would sell the widget they purchased for $1 to the client for $1.10 and pocket 10 cents. If the price of the widget Wells bought for $1 fell to 95 cents, Wells would just give up their $1 purchase to the client, plus whatever markup they agreed to.

Heads, Wells wins. Tails, client loses.

The complaint notes that a Wells FX specialist wrote that he:

“Bumped spreads up a pinch,” that “these clients who are in the mode of just processing wires will most likely not notice this slight change in pricing” and that it “could have a very quick positive impact on revenue without a lot of risk.”

Talk about a boiler room operation. Personally, I think calling what you are doing to a client a “piñata” should have easily put Wells in the Fed’s penalty box another 5 years at least!

Wells has been released from the Fed’s 2018 enforcement order. I would like to think they have learned their lesson and are reformed, but I would lay good odds against it. A leopard can’t change its spots.

Racket News is a reader-supported publication.

Consider becoming a free or paid subscriber.

From the Fraser Institute

By Matthew Lau

And in January, all of Canada’s six largest banks quit the Net-Zero Banking Alliance, an alliance formerly led by Mark Carney (before he resigned to run for leadership of the Liberal Party) that aimed to align banking activities with net-zero emissions by 2050.

The Canada Pension Plan Investment Board (CPPIB) has cancelled its commitment, established just three years ago, to transition to net-zero emissions by 2050. According to the CPPIB, “Forcing alignment with rigid milestones could lead to investment decisions that are misaligned with our investment strategy.”

This latest development is good news. The CPPIB, which invest the funds Canadians contribute to the Canada Pension Plan (CPP), has a fiduciary duty to Canadians who are forced to pay into the CPP and who rely on it for retirement income. The CPPIB’s objective should not be climate activism or other environmental or social concerns, but risk-adjusted financial returns. And as noted in a broad literature review by Steven Globerman, senior fellow at the Fraser Institute, there’s a lack of consistent evidence that pursuing ESG (environmental, social and governance) objectives helps improve financial returns.

Indeed, as economist John Cochrane pointed out, it’s logically impossible for ESG investing to achieve social or environmental goals while also improving financial returns. That’s because investors push for these goals by supplying firms aligned with these goals with cheaper capital. But cheaper capital for the firm is equivalent to lower returns for the investor. Therefore, “if you don’t lose money on ESG investing, ESG investing doesn’t work,” Cochrane explained. “Take your pick.”

The CPPIB is not alone among financial institutions abandoning environmental objectives in recent months. In April, Canada’s largest company by market capitalization, RBC, announced it will cancel its sustainable finance targets and reduce its environmental disclosures due to new federal rules around how companies make claims about their environmental performance.

And in January, all of Canada’s six largest banks quit the Net-Zero Banking Alliance, an alliance formerly led by Mark Carney (before he resigned to run for leadership of the Liberal Party) that aimed to align banking activities with net-zero emissions by 2050. Shortly before Canada’s six largest banks quit the initiative, the six largest U.S. banks did the same.

There’s a second potential benefit to the CPPIB cancelling its net-zero commitment. Now, perhaps with the net-zero objective out of the way, the CPPIB can rein in some of the administrative and management expenses associated with pursuing net-zero.

As Andrew Coyne noted in a recent commentary, the CPPIB has become bloated in the past two decades. Before 2006, the CPP invested passively, which meant it invested Canadians’ money in a way that tracked market indexes. But since switching to active investing, which includes picking stocks and other strategies, the CPPIB ballooned from 150 employees and total costs of $118 million to more than 2,100 employees and total expenses (before taxes and financing) of more than $6 billion.

This administrative ballooning took place well before the rise of environmentally-themed investing or the CPPIB’s announcement of net-zero targets, but the net-zero targets didn’t help. And as Coyne noted, the CPPIB’s active investment strategy in general has not improved financial returns either.

On the contrary, since switching to active investing the CPPIB has underperformed the index to a cumulative tune of about $70 billion, or nearly one-tenth of its current fund size. “The fund’s managers,” Coyne concluded, “have spent nearly two decades and a total of $53-billion trying to beat the market, only to produce a fund that is nearly 10-per-cent smaller than it would be had they just heaved darts at the listings.”

Scrapping net-zero commitments won’t turn that awful track record around overnight. But it’s finally a step in the right direction.

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

Alberta Independence Seekers Take First Step: Citizen Initiative Application Approved, Notice of Initiative Petition Issued

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

National Health Care Fraud Takedown Results in 324 Defendants Charged in Connection with Over $14.6 Billion in Alleged Fraud

-

Business2 days ago

RFK Jr. says Hep B vaccine is linked to 1,135% higher autism rate

-

Business1 day ago

Why it’s time to repeal the oil tanker ban on B.C.’s north coast

-

Censorship Industrial Complex2 days ago

Censorship Industrial Complex2 days agoGlobal media alliance colluded with foreign nations to crush free speech in America: House report

-

Alberta21 hours ago

Alberta21 hours agoAlberta Provincial Police – New chief of Independent Agency Police Service

-

Opinion18 hours ago

Opinion18 hours agoBlind to the Left: Canada’s Counter-Extremism Failure Leaves Neo-Marxist and Islamist Threats Unchecked

-

Business2 days ago

Business2 days agoElon Musk slams Trump’s ‘Big Beautiful Bill,’ calls for new political party

-

Alberta1 day ago

Alberta1 day agoPierre Poilievre – Per Capita, Hardisty, Alberta Is the Most Important Little Town In Canada

-

COVID-1919 hours ago

COVID-1919 hours agoTop COVID doctor given one of Canada’s highest honors