Crime

“Fake Chinese income” mortgages fuel Toronto Real Estate Bubble: Canadian Bank Leaks

Canadian Banking Money Laundering Investigation Reposted in Light of Ottawa’s Fentanyl Czar Pledge

In response to Ottawa’s pledge to tackle fentanyl-linked money laundering—including the appointment of a “fentanyl czar” and new intelligence-sharing initiatives with the United States—The Bureau is reposting this February 2024 investigation estimating tens of billions, potentially several hundred billion, laundered through Vancouver and Toronto real estate via underground banking networks tied to China and global narcotics trafficking, including fentanyl.

FINTRAC’s 2023 analysis of 48,000 transactions involving members of the Chinese diaspora exposed vast wire transfers from Hong Kong and Mainland China, funneled through “money mule” accounts linked to students, homemakers, and shell businesses—including law firms. These findings raised serious concerns about Canada’s banking oversight but led to no prosecutions in Canada. The study also revealed laundering patterns central to the U.S. Justice Department’s $3 billion TD Bank case, with international students from China working with Beijing’s United Front networks playing key roles in the TD Bank money laundering, according to U.S. investigator David Asher, a former Trump Administration official. The revelations underscore how the so-called “Vancouver Model”—once centered on laundering drug proceeds through British Columbia government casinos—evolved during the COVID-19 pandemic, embedding itself deeper into Canada’s banking and legal systems. These findings align with research from SFU urban planner Andy Yan, who has documented how foreign capital distorts Canada’s housing market, with mortgage approvals and home purchases far exceeding reported local incomes.

At the heart of this investigation is HSBC Canada whistleblower “D.M.,” who believes they uncovered at least $500 million in dubious Toronto-area mortgages backed by fabricated remote-work salaries from China. After raising the alarm internally, D.M. says HSBC Canada introduced only superficial reforms and pressured him to delete critical records—deepening his conviction that Canada’s financial oversight remains dangerously weak.

Former RCMP investigators Garry Clement and Cal Chrustie, who reviewed D.M.’s evidence, warn that systemic vulnerabilities persist. Chrustie—who has extensively documented Canada’s weak regulations enabling underground banking linked to organized crime in China, Iran, and Mexico—pointed to the 2012 U.S. Justice Department case where HSBC was fined $1.9 billion over $881 million in cartel-linked transactions involving Mexico’s Sinaloa cartel and Colombia’s Norte del Valle cartel.

As Andy Yan has emphasized, governments at all levels bear responsibility for enabling foreign capital to flood Canada’s housing market without adequate transparency. “When you have programs designed to domesticate foreign capital into local real estate, you see these income-to-home-price incongruities,” he said.

Ottawa’s new fentanyl czar is tasked with coordinating intelligence-sharing and enforcement actions with U.S. agencies to disrupt fentanyl trafficking and related money laundering. Trudeau’s government has also pledged to designate cartels as terrorist organizations, a move that could have sweeping consequences for Canadian banks by exposing them to heightened U.S. financial scrutiny and enforcement actions.

It remains to be seen what position Liberal Party leadership favourite Mark Carney—former Governor of the Bank of Canada (2008–2013) and the Bank of England (2013–2020), and a globally influential banker—will take on Canada’s ongoing struggles with financial crime and illicit capital flows. While the Bank of Canada does not oversee financial crime enforcement, Carney’s extensive experience in international financial regulation—gained through his roles involving oversight at global institutions such as the Bank for International Settlements and his active participation in forums on financial stability—suggests he could offer valuable insights into Canada’s banking vulnerabilities. This is particularly noteworthy as he emerges as a political contender and potential Prime Minister.

|

OTTAWA, Canada — The whistleblower, a Canadian business school graduate, was staggered by the suspicious home loans he discovered in 2022 when he joined a mortgage approval team in a small HSBC branch on the outskirts of Toronto.

He knew of suspicions surrounding Chinese capital in British Columbia real estate, but had never witnessed shady lending while working at an HSBC branch in Campbell River, a bucolic town on the coast of Vancouver Island.

When he arrived at HSBC’s bank in Aurora, an affluent suburb north of Toronto, he discovered explosive growth in home loans to Chinese diaspora buyers during the Covid-19 pandemic.

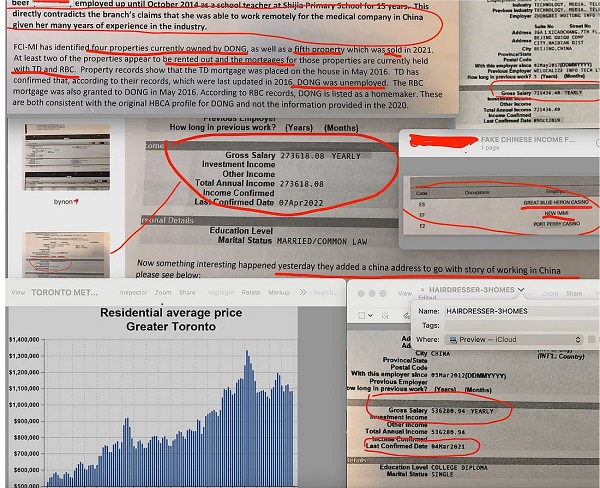

Chinese migrants living across Toronto were obtaining mortgages from HSBC while supposedly earning extravagant salaries from remote-work jobs in China. In one example, an Ontario casino worker that owned three homes also claimed to earn $345,000 in 2020 analyzing data remotely for a Beijing company.

Before joining HSBC Canada, the whistleblower had studied fake-income mortgage frauds for his Business Masters degree at Vancouver Island University. After arriving at Aurora in February 2022, while digging into the branch’s loan books and interrogating his colleagues, he made mind-blowing assessments.

Since 2015, the whistleblower concluded, more than 10 Toronto-area HSBC branches had issued at least $500-million in home loans to diaspora buyers claiming exaggerated incomes or non-existent jobs in China.

These foreign-income scams spiked during the pandemic, the whistleblower believed, because borrowers could somewhat plausibly claim to be working remotely in other countries while riding out Covid-19 in Canada.

While a small bank of Aurora’s size was expected to issue about $23-million in residential loans every year, this branch had shovelled out $88-million in mortgages in 2020, according to the whistleblower, and over $50-million in 2021.

The whistleblower, whomThe Bureau is calling D.M., immigrated to Canada as an international student from India, making him a minority among mostly Chinese-Canadian co-workers at the Aurora branch.

As D.M. probed his colleagues, his belief gained conviction, that HSBC Canada and other Canadian banks including CIBC had systemic problems with highly questionable mortgages issued to diaspora buyers with unverified sources of wealth in China.

Losing sleep, in April 2022, D.M. sent an audacious email to senior bank executives: “I am going to reveal potential mortgage fraud at HSBC Bank Canada and possibly some employees benefited from the fraud, financially pocketing thousands of dollars, which I call the proceeds of crime.”

D.M.’s explosive four-page complaint triggered an internal investigation that led to some reforms at HSBC Canada according to internal emails obtained by The Bureau.

But more than a year later, D.M. was so dissatisfied with the bank’s response that he risked sharing his story and numerous internal documents for an unprecedented journalistic investigation into Canada’s housing affordability crisis.

“I found out a huge mortgage fraud showing borrowers with exaggerated income from one specific country, China, pretending to be working remotely,” D.M. informed The Bureau in June 2023. “I believe the housing prices in Toronto are linked to this, because this is about income verification in banks, which is supposed to moderate demand.”

The Bureau asked HSBC Canada to review emailed information for this story and provide an appropriate manager for an interview regarding D.M. ‘s records and allegations.

“I won’t have anyone to speak with you directly,” Sharon Wilks, Head of Communications, responded. “But for context: As a global bank, HSBC is at the forefront of efforts to identify, prevent and deter financial crime … We will not do business with individuals or entities we believe are engaged in illicit conduct.”

Wilks added that HSBC Canada “can and do regularly exit relationships with clients whose activities we deem too risky.”

The Bureau’s seven-month investigation into D.M.’s allegations suggests HSBC Canada and other Canadian banks could have issued many billions of dollars in questionable mortgages to Chinese diaspora buyers, and a significant cause of Canada’s real estate bubble is hundreds of billions in illicit fund transfers from China into Canada, and bank lending that amplifies its impacts, especially in Toronto and Vancouver home prices.

“There are thousands of these cases, large scale,” D.M. said in an interview. “Hardworking Canadians are denied mortgages and these Chinese residents forge documents and get mortgages approved, heating up the already hot Ontario real estate markets.”

“These people don’t have steady jobs or income in Canada,” he alleged, “but what they are doing is scams to launder money, and get mortgages using fake documents.”

The Bureau’s investigation included asking seven prominent Canadian experts to assess some of D.M.’s documents, allegations and conclusions.

This investigation suggests D.M. ‘s calculation is plausible, that the Aurora branch and other Toronto-area HSBC branches have issued at least $500-million in questionable Chinese income loans since 2015.

But D.M’s findings could also change the public’s understanding of housing affordability in Toronto and Vancouver, a politically explosive issue expected to frame Canada’s upcoming federal election.

This is because, according to the academics and criminologists that reviewed D.M.’s documents with The Bureau, his evidence fits into FINTRAC’s much broader examinations of suspicious real estate and banking transactions.

In 2023, the anti-money laundering watchdog published a ground-breaking study into 48,000 Chinese diaspora banking transactions.

FINTRAC found that during the Covid-19 pandemic, because Canadian casinos were closed, Chinese underground banking schemes evolved, flooding electronic fund transfers from Hong Kong into Canadian bank accounts that served like corridors for murky real estate transactions.

The Bureau’s analysis also finds that what D.M. discovered in Toronto banks, finally sheds light on mysterious capital flows discovered by a prominent Canadian academic in 2015, in a study of Vancouver land titles and mortgages.

That examination of $525-million worth of real estate purchases in a six-month period found 66 percent of buyers in several affluent neighbourhoods were recent Chinese diaspora migrants, and most mortgages went to buyers with little or no income in Canada.

Similarly, what D.M. found in his probe of pandemic-era loans could be called the evolving “Toronto Method” of an underground banking system discovered first in Vancouver, and found to be laundering a stunning $1.2-billion in cash from Mainland China through British Columbia government casinos in 2014.

This system of shadowy transfers was dubbed the “Vancouver Model” by an Australian professor, and brings together transnational organized crime, affluent Chinese nationals seeking to export their wealth abroad, and Canadian casinos, banks and real estate, in transactions that evade policing because the pivotal cash exchanges are done off the books by professional money launderers serving the global Chinese diaspora.

According to FINTRAC’s 2023 study of 48,000 pandemic-era transactions, this evolving Vancouver Model network “simultaneously facilitates money laundering and the circumvention of Chinese currency controls”

“As a result of the temporary closures of Canadian casinos due to the COVID-19 pandemic, professional money launderers began to diversify their money laundering methods,” FINTRAC’s study says.

“During this time, FINTRAC observed a rise in money laundering typologies involving transferring large sums of funds to Canada from foreign money services businesses, often located in China, notably Hong Kong, and the laundering of the funds primarily through the real estate, securities, automotive and legal professions.”

These wire transfers from China were routed into bank accounts of “multiple, unrelated individuals in Canada,” that served as “money mules” in byzantine networks involving Canada-based real estate developers, real estate agents, mortgage brokers and banks.

These Chinese diaspora bank account owners often claimed they were students, homemakers, office managers, or unemployed, FINTRAC reported.

They sometimes used their accounts to send bank drafts to others in Canada for home purchases, or served as “straw buyers” for offshore investors.

“Mortgage payments are sourced from incoming funds from China,” FINTRAC’s alert said.

FINTRAC’s study doesn’t say that Canadian banks knowingly issued fake-income mortgages to Chinese diaspora buyers in Toronto.

But in an interview, D.M. said banking staff are trained to guard against fraud, and the loan application packages he reviewed in Aurora beggared belief.

“The bank found out that one lady works in a casino part-time but got a $1.4 million mortgage showing over $300,000 annual income,” he said. “Plus she takes money as benefits from the government, for her two kids.”

In other examples, an HSBC mortgage client claimed to earn $700,000 annually for remote work in China, while simultaneously living in Canada and paying off a $10,000 student loan.

Another woman who owned homes in Aurora, Markham and Scarborough, worked part-time as a hairdresser while also claiming to earn $536,280 at a “Business Manager” job in Guangzhou.

“Canadian workers have been put out of the real estate market by people working as a hairdresser that own a couple homes,” D.M. said in an interview.

“How is that fair?”

|

The most shocking case reviewed by The Bureau, shows that one woman that owns at least four Toronto properties opened her HSBC Aurora bank account in 2013, claiming to be a “Homemaker with no annual income.”

But her Toronto account soon received incredible amounts of wire transfers from HSBC China accounts, and paid out “high value cheques” to third parties for real estate purchases.

This case suggests “Toronto Method” shadow banking described in FINTRAC’s 2023 study has been seeping into Toronto real estate for about a decade.

And yet in 2020, this same woman applied for another HSBC Canada mortgage, claiming to earn $763,000 remotely from her job in China.

This evidence from the HSBC whistleblower complements the seminal investigations of Simon Fraser University academic Andy Yan, who examined sales from August 2014 to February 2015 in several communities on Vancouver’s westside. The average home price in Yan’s study was $3-million.

Looking back at his Vancouver findings in comparison to D.M.’s Toronto banking documents, Yan told The Bureau “I think this helps affirm some of my early work that I did, almost nine years ago.”

“This goes to the core of our banking system,” he said, “and how are we verifying identities and how are we verifying incomes.”

In Yan’s controversial study the vast majority of mortgages went to buyers listing their occupation as home-maker, followed by students, and managers. HSBC and CIBC were the dominant lenders.

Unlike the HSBC whistleblower, Yan had no access to internal banking data regarding the purported origin of funds behind these mortgages taken by Chinese diaspora buyers.

But in an interview, Yan said what he found most interesting back in 2015, was suspicions that Chinese migrants were often buying homes with bulk cash, weren’t accurate. The truth was more complex and seems to be clarified by D.M.’s mortgage findings in Toronto.

“It’s about that global flow of capital, and how it’s multiplied by Canada’s mortgage and lending system,” Yan said. “Because you have to remember, one of the biggest conclusions about my study was that it wasn’t bags of cash that were being used to purchase Vancouver homes outright. They were loans being used. So now, I’m thinking, this is where my study connects up to what you have discovered in Toronto.”

“The interesting story here,” Yan added, “is what happens in Toronto real estate may not repeat Vancouver, but it perhaps rhymes.”

Probably the most famous Chinese property owner from Yan’s 2015 study areas is Huawei executive Meng Wanzhou. In 2009 her family bought a home in Vancouver’s Dunbar neighborhood for $2.73 million, land titles show. In 1998, ten years before Vancouver Model transactions started to surge in Vancouver real estate, the home was sold for $370,000. The home is now valued at almost $6-million.

Ashleigh Rhea Gonzales, a former RCMP data scientist who recently published a criminology thesis finding Chinese diaspora underground banking causes significantly more money laundering into Canada’s real estate than previously estimated, said that D.M.’s findings resemble her own Vancouver Model research.

“This whistleblower’s allegations of widespread mortgage fraud at HSBC Canada align with some of the first-hand accounts from staff of some Canadian financial institutions that I have come across in my research on money laundering in British Columbia,” Gonzales said.

Gonzales, who worked for RCMP’s anti-gang unit in British Columbia until 2023, says she found reports of mortgage fraud accelerated “during the uptick in the Canadian housing bubble after the Vancouver 2010 Olympics,” and continued to surge from 2015 to 2018.

With all this considered, and comparing data sources in this story with previous evidence confirmed in British Columbia’s Cullen Commission, The Bureau estimates that from 2014 to 2023, well over $200-Billion in Vancouver Model and Toronto Method funds could have poured through underground diaspora networks and Canadian financial institutions into Toronto and Vancouver’s real estate.

A federal official not authorized to comment publicly also examined D.M.’s banking leaks for The Bureau, and called this information “explosive.”

The official said money laundering is increasing in Canada, and D.M.’s belief that Chinese-income mortgage fraud has boosted home prices in Toronto is likely true, but also should apply for Vancouver and Montreal real estate prices. The official noted that other nations require tax agencies to verify incomes for mortgages, which isn’t the case in Canada.

“It matters for our next generation because of the impact on the housing market,” the official said.

Queen’s University professor Christian Leuprecht – editor of Dirty Money, a new academic text that probes how Ottawa’s weak regulation has “turned the Canadian federation into a destination of choice for global financial crime” – also reviewed some of D.M. ‘s leaks.

“It’s not a new problem, but you’re taking it to the next level,” Leuprecht said.

“Why does this matter? Because organized crime isn’t just laundering their ill-gotten gains, like any good business person, when they buy real estate, they generate a down payment, then get a mortgage for the rest. Why buy one property when you can buy four?”

“Do you know how many mortgage frauds we have in our books?”

The Bureau’s review of HSBC Canada emails and D.M.’s text messages, shows he came to believe numerous employees at the Aurora branch had direct knowledge of faked Chinese income mortgages, and a veteran manager with oversight of more than 10 Greater Toronto branches knew about broad and questionable mortgage lending for Chinese diaspora clients.

Months after D.M. blew the whistle internally he exchanged texts with another employee, identifying colleagues that they believed had knowledge of diaspora mortgage scams.

The texts suggest D.M. believed HSBC Canada and other Canadian banks continued to hold vast amounts of suspicious foreign income mortgages, which could cause systemic loan quality risks if Toronto’s real estate prices decline.

“Do you know how many mortgage frauds we have in our books,” D.M. texted to his colleague. “It’s insane.”

“She told me,” the colleague replied, referring to an HSBC branch manager.

“She was like, if you do come, you gotta be prepared for the mortgage payout.”

“These people showed fake income and got mortgage,” D.M. continued. “Now interest rate is high, they can’t cope.”

“Other branches did the same thing too,” his co-worker replied. “I heard there’s a lot.”

“Absolutely,” D.M. texted. “All branches engaged in it.”

“This is like the unspoken secret,” his co-worker concluded. “I’m pretty sure other banks have it too. My Aunt have no income and got a mortgage for 700k. They just need a Covenanter from China.”

Generally, in mortgage contracts a covenanter takes responsibility for the loan if the primary borrower defaults.

Internal records reviewed by The Bureau confirm that on April 18, 2022, D.M. sent a lengthy complaint email to senior HSBC Canada executives, informing them of allegations he’d learned from his colleagues.

In it, he alleges that an Aurora manager had informed him of a complaint letter posted to the branch, that accused mortgage brokers and branch employees of colluding in scam mortgages emanating from Mainland China fraud networks.

Pointing to specific examples, D.M. claimed that another branch colleague had admitted processing numerous loan applications without meeting his clients, because a branch manager delivered her subordinates foreign income client applications so “they did not have to get sales themselves.”

“Surprisingly all these clients he would get will have foreign income most of the time very inflated like 400k or 670k a year,” D.M. wrote. “To me that’s suspicious, but he never questioned the branch manager because in Asian culture it’s disrespectful to question elders.”

D.M. also informs his bosses that one Aurora bank manager opened up to him, saying she believed allegations of mortgage fraud collusion involving some branch staff.

“She said yes, she knows specially in Mainland China there is a team who would even answer emails and phone calls verifying [Chinese income] but it’s a sophisticated and well organised scam,” D.M. ‘s email to HSBC Canada managers says.

His complaint explains that he continued to press an Aurora bank manager on her knowledge of fraud allegations.

“When I asked for such a serious issue if she raised a HSBC confidential [complaint] or not she evaded my question,” D.M. wrote. “Now we all love numbers, but I don’t think the bank will like these kinds of numbers achieved through this way.”

Describing why he contacted HSBC Canada executives directly, the whistleblower’s complaint says he felt confused and isolated, but D.M. decided “local leadership if not participated, at least turned a blind eye,” to Chinese fake-income scams, forcing D.M. to “bring up a serious issue against people of superior positions.”

“I could not have stayed silent, in fact I could not sleep well thinking about it,” his April 2022 complaint says. “It reminds me to some extent what happened with the Home Capital Group.”

“The whole thing is wrong on so many grounds,” D.M. continued.

“Now I know one more reason why Canadians and permanent residents are not getting into the housing market. It’s not only HSBC such things are happening across other Canadian banks as well.”

In the Home Capital case, the Ontario Securities Commission fined the prominent Ontario-based subprime mortgage lender in 2017, alleging Home Capital failed to disclose several of its mortgage brokerages had major problems with faked-income mortgages.

D.M. concluded his four-page complaint to senior executives, writing: “I recommend all mortgage deals of this branch in the last 3 years at least if not longer with Foreign income be probed.”

“Bank statements can be verified directly with the foreign banks or use a reputable third party to verify,” he suggested. “When we find someone with Fake ID or trying to impersonate someone we call the cops. But these people, both staff nor clients who did fraud were reported.”

Hours later on April 18, 2022, an HSBC Canada executive emailed back: “I am going to refer this to our Fraud and Risk teams and they will investigate your concerns.”

“The Implications are Broader”

The next day D.M. continued to hound HSBC Canada managers with emails to support his allegations, spotlighting the absurdity of massive Chinese remote incomes claimed by diaspora buyers.

He pointed to one woman with a $1.6-million HSBC Canada mortgage.

“The client claims to be in Canada but [is] a office supervisor in China. [In the] age of remote working in which country [does] a office supervisor makes 400k please tell me,” D.M. wrote.

“[W]hen I asked the co-worker she said her job is not to use the brain or be a police, when I asked do you think she makes that kind of money and how is she doing her job being in Canada to be an office supervisor in China[?]”

Pointing to another document, D.M. warned his managers about Ms. Chen, who claimed to make $721,000 annually as “project manager” for a Beijing telecommunications company, to secure a $1.89 million mortgage.

|

Again on May 4, 2022, D.M. emailed executives, suggesting internal records for an Aurora client named Ms. Lin had been altered soon after D.M. blew the whistle on fake Chinese income loans.

His email, which included Ms. Lin’s client profile, warned: “Something interesting happened yesterday, they added a China address to go with [the] story of working in China, please see below.”

The Aurora branch banking records disclosed to The Bureau show that Ms. Lin owns three homes in the blocks surrounding Pacific Mall in Markham.

“The client was onboarded on 24th March with Canada address only and Canadian tax residency,” D.M.’ s email continued.

“She claims to be working in China and have foreign income, so the story she is stuck in Canada due to Covid is very interesting. Suddenly yesterday she decided her address in China. Someone saw the discrepancies and the branch team decided to change it.”

“To me that’s a red flag done to align with the story portrayed.”

Next, D.M. exposed Ms. Lin’s foreign income claim.

“She works for Food processing company, a logistics officer making 273k a year,” he wrote. “I don’t know which logistics officer can work when physically in a different company and also who makes 273k working as a logistics officer.”

Citing another internal banking record, D.M.’s email pointed to Ms. Lin’s $273,000 income and said “it’s interesting how they did the verification.”

The email continues to explain that branch records showed Ms. Lin and her husband had a joint mortgage with a balance of $497,000 at CIBC.

But suddenly during Covid-19, Ms. Lin applied for a new mortgage for $1.2 million with HSBC Canada.

“When I see such things I can’t stay quiet,” D.M.’s May 2022 email says. “[I] was assuming with the new rules things will stop, [but] declining the mortgage or retraining the staff is like treating the symptoms.”

He added that many suspicious Chinese income loans had been “flagged by our Fraud Team already.”

The whistleblower’s scathing assessment ends with the observation that D.M. didn’t believe “someone woke up and decided to scam the bank, but [worked with] a sophisticated network of agents who are training people what to say and answer.”

“The implications are broader and as a responsible bank and citizen we have to,” request investigations from the Canadian Revenue Agency or Ontario Provincial Police, D.M. asserted.

|

The Bureau asked Gonzales, the former RCMP data scientist, to review some of D.M.’s documents and conclusions.

“From what I have reviewed, D.M.’s findings align with what appear to have been commonplace practices by some groups of staff complicit from the front line, middle office, and back office and sanctioned by management,” Gonzales wrote, adding “whether knowingly or not depends on the individual work cultures.”

The Bureau also asked Stephen Punwasi to review D.M. ‘s leaked banking documentation.

Punwasi is a financial expert who founded Better Dwelling, a real estate analysis website with a large following of young professionals trying to understand why they’re excluded from home ownership in Canadian cities.

He also provided analysis for British Columbia’s 2018 report into Vancouver Model money laundering in casinos, real estate and luxury vehicles.

What Punwasi explained to the report’s author, former RCMP executive Peter German, is that even though Vancouver Model money launderers don’t comprise a majority of buyers in Vancouver, their willingness to overbid on home sales causes ripples that sends prices skyrocketing, especially during times when political turmoil inside China triggers increased capital flight.

“In 2015 and 2016 Ontario saw this flood of money from China, just like British Columbia, and it was not just to do with immigration, it was due to President Xi’s political crack down on corruption,” Punwasi said. “I think we’ve seen that capital flight in Ontario and B.C. in two big cycles, also including 2020 and 2021.”

The Bureau asked Punwasi if the banking records disclosed by D.M. help to explain Toronto’s real estate price surges.

“Absolutely,” he said, pointing to the case of Ms. Lin (who claimed a $273,000 remote-work income in China) and her three homes surrounding Markham’s Pacific Mall.

Property buyers that aren’t shopping for shelter, but for capital flight or money laundering vehicles, are what Punwasi terms the “marginal buyer.”

“The marginal buyer is like an exuberant buyer on crack, so if they are motivated to move as much money as possible,” he said, “the larger the mortgage they can get, it helps them to overpay for homes, and that can cause the price to launch.”

“So if you see a townhome in Toronto going for $2-million, you don’t know if it is mortgage money laundering or someone buying a place to live. You just have to compete with the going price.”

Punwasi says housing prices are a powerful political issue that will shape the next federal election.

But at the same time, young generations are confused by competing explanations on the causes of Canada’s housing affordability crisis, Punwasi believes, whether its lack of housing supply due to restrictive zoning bylaws, or increased demand due to recent immigration surges, or other factors that make Canada’s housing bubble an outlier in the Western world.

“There are so many conflicting narratives right now that people find it hard to believe the scale of impact that money laundering can have on Toronto real estate prices,” Punwasi said. “But no one has thought it through, that having criminals run our renting stock is a liability.”

Punwasi also believes that Prime Minister Justin Trudeau’s government has decreased scrutiny of money laundering in recent years.

He points to new data uncovered in a ministerial inquiry from Conservative MP Adam Chambers, who is a proponent of tougher money laundering laws, which found sharp declines in Canadian Revenue Agency audits of FINTRAC leads.

“The systemic corruption in housing has been snowballing,” Punwasi said, “to where it’s turned into, maybe the banks don’t need to check where the incomes are coming from, and now whole generations can’t find stable shelter.”

|

“Delete, delete, delete”

HSBC Canada emails reviewed by The Bureau show that while the bank appears to have responded to some of D.M. ‘s recommendations in 2022, troubling mortgage applications and problems with existing Chinese income loans continued.

A January 2023 email to an Aurora branch manager from HSBC Canada’s office in Montreal pointed to a client named Ms. B., who worked at an Ontario government casino, and owned homes across Toronto, in Richmond Hill, Newmarket and East York.

Documents show she obtained an HSBC Canada mortgage for $1.26 million in 2016, and that HSBC Canada staff “confirmed” in July 2021 that she was earning $345,000 with a remote work job in Beijing.

Despite her incredible claimed income, documents show, Ms. B. was having trouble paying at least one of her three mortgages.

An email from a “Senior Loss Mitigation” employee in Montreal to an Aurora branch employee says: “client is going through a tough time … her income is limited … I know she collect rent and she use it to pay her second mortgage. Please review the situation with the client to see if there is any special agreement available to her.”

But Aurora’s branch wrote back to the Montreal branch: “What we have told her is … if she really can’t pay, then she just have to put her house for sale … but she doesn’t want to do that.”

In an interview D.M. told The Bureau this case was typical.

“What they are doing is AirBnBing these properties,” he said. “But they can’t manage with higher interest rates.”

He said during mortgage application interviews at the Aurora branch he would often look across his desk and ask questions without letting clients know he was looking at their income claims from purported Chinese companies on his computer screen.

“Most of these people don’t even know what type of company is in their job profile,” he said.

And documents reviewed by The Bureau show that mortgage applications consistent with Fintrac’s 2023 Chinese money laundering report continued in Aurora.

In May 2023, D.M. emailed a senior HSBC Financial Crime Compliance investigator, writing “Just came across two profiles of clients and I have strong evidence these mortgages were also obtained with fake docs and fraudulently.”

When the investigator responded “I will take a look,” D.M. replied: “One had a CDA student loan of 10k and making 700k in China. Makes no sense, there are many other anomalies.”

In interviews, D.M. told The Bureau he waited “patiently for a year” after reporting his Chinese-income mortgage concerns to HSBC Canada managers, before concluding the bank’s response was insufficient.

“This has been going on for seven years and no one spoke up,” he said. “In my first meeting last year, they asked me a lot of questions, like why didn’t you use the normal channels? But I had no faith in the normal channels.”

“Many bank staff were obviously involved,” D.M. alleged. “It was not one or two employees turning the blind eye but the entire system, someone verifying those fake offer letters and pay stubs, or their bank statements from China.”

D.M. said his concerns also included HSBC Canada’s proposed sale to RBC, which was announced in 2022, about six months after D.M. ‘s April 2022 internal complaint. The sale was approved in December 2023 by Canada’s deputy Prime Minister Chrystia Freeland.

Christian Leuprecht, among other experts interviewed for this story, agreed that D.M.’s allegations of widespread Chinese-income frauds at HSBC Canada could raise questions about whether Freeland, Canada’s finance minister, had knowledge of mortgage lending investigations inside HSBC when she approved the sale.

Freeland directed RBC to “establish a new Global Banking Hub in Vancouver,” and “maintain Mandarin and Cantonese banking services at HSBC branch locations,” a Department of Finance statement says.

Ultimately, D.M. says he chose to share his story with Canadian citizens partly because he felt pressured to erase evidence from his whistleblower complaint emails.

A June 2023 email from the bank’s personnel department says “we hereby demand that you immediately and permanently delete any and all HSBC information on any personal email accounts.”

Crime

Ontario Police’s Record Fentanyl Bust Suggests Cartel–Iranian–PRC-Supplied Nexus from Ottawa to Hamilton Along Six Nations Corridor

Investigators found that packages were being shipped across Canada using both courier services and Canada Post. The digital reach of the network spanned nearly the entire country: Alberta, British Columbia, Manitoba, New Brunswick, Nunavut, Nova Scotia, Ontario, Prince Edward Island, and Quebec.

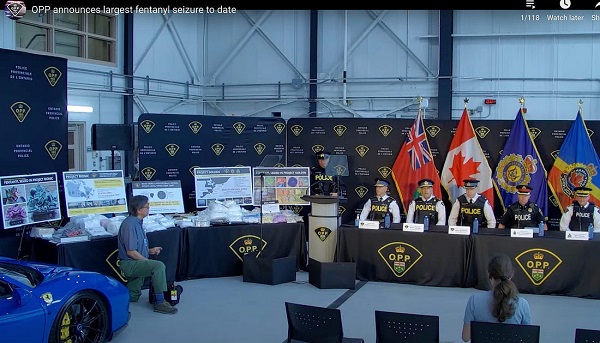

In a pair of sweeping investigations unveiled yesterday, the Ontario Provincial Police announced the largest fentanyl seizure in the force’s history—more than 43.5 kilograms of deadly synthetic opioids, including fentanyl, carfentanil, and precursor substances—enough to generate over 435,000 potentially lethal street doses. Nearly 20 suspects were arrested and more than 200 criminal charges laid in connection with the operations, codenamed Project Bionic and Project Golden.

The twin probes targeted sophisticated fentanyl trafficking networks that stretched across southern Ontario, extending northeast into the nation’s capital, Ottawa, and penetrating the national mail and courier systems. The seizures—made in locations ranging from Hamilton-area homes to Ottawa postal depots—come amid mounting warnings from U.S. security officials that Canadian territory is increasingly being exploited by Mexican and Chinese cartel networks, often intertwined with Iranian state-aligned trafficking and laundering operations.

The Bureau, a leading authority on North American fentanyl trafficking and Canada’s structural vulnerabilities, has reported extensively on Chinese-run illegal marijuana operations and cartel-affiliated smuggling corridors spanning British Columbia, Quebec, and Indigenous territories in southern Ontario. These networks operate near Hamilton and Six Nations and extend eastward through the Ottawa-Cornwall corridor to the New York State border, where key enforcement actions linked to Project Golden were concentrated.

OPP Commissioner Thomas Carrique called the busts historic in scope.

“Although these two investigations are independent, they both resulted in alarming seizures of fentanyl and reveal a complex level of drug trafficking,” he said at a press conference in Orillia. “These operations occurred at opposite ends of our province, which underscores that this is a province-wide public safety issue.”

“Between these investigations, there was a staggering 43 kilos of fentanyl seized,” Carrique added, “which equates to about 435,000 potentially lethal street doses.”

Launched in November 2024 by the OPP Covert Internet Intelligence Unit, Project Bionic was the force’s first major dark web narcotics probe. The investigation—led by the Organized Crime Enforcement Bureau—targeted a trafficking operation that processed high volumes of drug orders via encrypted marketplaces. Investigators found that packages were being shipped across Canada using both courier services and Canada Post. The digital reach of the network spanned nearly the entire country: Alberta, British Columbia, Manitoba, New Brunswick, Nunavut, Nova Scotia, Ontario, Prince Edward Island, and Quebec.

On Monday, March 10, 2025, OPP officers arrested two individuals at a Canada Post location in Ottawa and seized 86 packages containing various drugs ready to be shipped across the country. The raids yielded more than 27 kilograms and 64,000 tablets, representing 37 different illegal drugs and diverted prescription medications, including fentanyl, hydromorphone, methamphetamine, ketamine, MDMA, and others. Officers also seized $95,000 in cash, a firearm, and two stolen luxury vehicles. Among them was a stolen 2018 Ferrari 488 Spider convertible, valued at over $400,000. Investigators also recovered fraudulent licence plates and reprogrammable key fobs, highlighting the operation’s links to broader auto theft and financial crime networks.

Later that month, police recovered an additional 11 stolen vehicles. Four Ottawa-area individuals were arrested and now face a total of 85 charges.

Among those charged was 26-year-old Amr Hammami, who faces 56 counts under the Criminal Code and the Controlled Drugs and Substances Act. Charges include possession of prohibited firearms and ammunition, laundering proceeds of crime, and trafficking or possession for the purpose of trafficking in fentanyl, cocaine, methamphetamine, heroin, MDMA, ketamine, oxycodone, hydromorphone, alprazolam, and methylphenidate. Police allege Hammami coordinated drug shipments, managed laundering operations, and operated from within Ottawa’s urban core.

“Project Bionic exposed the alarming volume of dangerous drugs being sold through dark web marketplaces, with packages shipped across the country,” Carrique said. “These arrests show that law enforcement can track and stop even the most complex online trafficking operations. This investigation also plainly demonstrates the connections between drug trafficking and other crimes, such as auto theft and illegal firearms. This seizure is a major step in dismantling drug networks—whether online or on the street—and reflects the OPP’s ongoing commitment to public safety.”

The dark web refers to a portion of the internet not indexed by standard search engines. It requires specialized software to access and employs encrypted communication protocols to conceal users and platforms. Within it, marketplaces operate as anonymous forums for criminal transactions—trading in everything from drugs and stolen data to counterfeit pharmaceuticals and hacking tools.

Project Golden, launched in July 2024, tracked a sprawling fentanyl distribution ring with supply hubs in Hamilton, Oxford, Norfolk, Burlington, Mississauga, York, and Toronto. On May 28, police executed 16 coordinated search warrants targeting residences, businesses, and vehicles. They seized $5.4 million in narcotics, including 38 kilograms of fentanyl—the largest single fentanyl seizure in OPP history—alongside 19.5 kg of methamphetamine, 5.5 kg of cocaine, MDMA, psilocybin, three guns, three vehicles, and $121,600 in cash.

Fifteen individuals were arrested under Project Golden, facing 140 charges including conspiracy, trafficking, and weapons offenses. One of the central figures was 44-year-old Matthew Savory, who faces 70 charges, including two counts of trafficking carfentanil, and conspiracy to traffic in fentanyl, cocaine, and methamphetamine.

Despite the operation’s scope, Commissioner Carrique urged reporters not to fixate on whether the fentanyl was U.S.-bound. “There’s no indication the fentanyl was destined for the United States or any other country,” he said.

But The Bureau’s prior investigations suggest a more complex picture. In 2022, Montreal trafficker Arden McCann—known online as “The Mailman”—was indicted in the Northern District of Georgia for mailing synthetic opioids from Canada and China into all 49 U.S. states. McCann’s dark web network—located 192 kilometres from Ottawa, the Project Bionic dark web nexus—generated more than $10 million in revenue, using Canada Post and encrypted platforms—an operational model nearly identical to Project Bionic.

As part of that investigation, DEA agents and Canadian authorities seized two million counterfeit Xanax pills, five industrial pill presses, $200,000 in cash, 15 firearms, ballistic vests, and detailed ledgers showing transactions with Chinese precursor suppliers.

Investigators say the geography of southwestern Ontario—stretching from Hamilton to Six Nations and down to the Buffalo border—makes it a key strategic zone for cartel activity. The Bureau previously revealed a related cartel-linked bust on Six Nations reserve land, where counterfeit tobacco production and drug trafficking thrived in a jurisdictional grey zone.

The timing and location of Project Golden, coming shortly after the Six Nations-based Project Panda raids, suggest links. Both operations targeted the same narcotics distribution corridors between Brantford and Hamilton, uncovering fentanyl, firearms, and vehicles connected to high-level criminal networks.

The findings align with concerns raised by FBI Director Kash Patel, who recently warned that cartels were increasingly exploiting Canada as a fentanyl staging ground.

While the OPP emphasized the domestic impact of removing 43.5 kilograms of fentanyl from circulation, law enforcement experts warn that without structural reforms—including a Canadian anti-racketeering law, enhanced port and border surveillance, stricter chemical import tracking, and expanded financial intelligence enforcement—Canada will remain a vulnerable node in the transnational opioid web.

The Bureau is a reader-supported publication.

To receive new posts and support my work, consider becoming a free or paid subscriber.

Invite your friends and earn rewards

![]()

From the Daily Caller News Foundation

By Mariane Angela

During a Monday night press briefing, Democratic Los Angeles Mayor Karen Bass told the Trump administration to stop the Immigration and Customs Enforcement (ICE) raids in Los Angeles.

President Donald Trump deployed the National Guard to Los Angeles on Saturday after riots erupted following an ICE raid at a Home Depot. During Monday’s press briefing, Bass called for an end to the raids conducted by the Trump administration, claiming that the power to deploy troops or request assistance should lie with state and local officials, not the federal government.

“I would say stop the raids. Stop the raids, period. I would say give the power back to our governor, and if we need the National Guard, we can do it in the normal circumstances, which is the request is made local, and the governor decides, or not to, grant that to our city,” Bass said when asked what she would say to the Trump administration.

Bass reiterated her earlier stance and questioned the need for an additional military presence, given the National Guard’s current role in securing federal buildings.

WATCH:

“We didn’t need the National Guard. Why on earth? What are they going to do? Do you know what the National Guard is doing now? They are guarding two buildings,” Bass said when asked to react to the deployment of Marines.

Bass then called the deployment an unjustified and overreaching action.

“They are guarding the federal building here in downtown, and they’re guarding the federal building in Westwood. That’s what they’re doing. So they need Marines on top of it? I don’t understand that. That’s why I feel like we are part of an experiment that we did not ask to be a part of,” Bass added.

Despite Bass claiming that the National Guard’s deployment was unnecessary, Fox News reporter Bill Melugin shared videos showing ICE agents in one of the vehicles being struck by rocks. Melugin also posted additional footage and photos of the aftermath, including an image of an ICE agent’s injury and a windshield damaged by a rioter’s rock.

Around 1,000 individuals wreaked havoc in Los Angeles Friday night, surrounding a federal building, attacking ICE agents, deflating tires and vandalizing government property, according to the Department of Homeland Security. The unrest caused significant damage and severe traffic disruptions, bringing several key city roads to a complete standstill.

On Saturday night, Trump authorized the deployment of the National Guard to assist local law enforcement and warned Democratic California Gov. Gavin Newsom that the federal government would intervene if local authorities failed to restore order.

In response, California filed a lawsuit against the Trump administration Monday, challenging the deployment of National Guard troops to Los Angeles to address the immigration riots. Attorney General Rob Bonta and Newsom said that federalizing 2,000 California National Guard members without Newsom’s consent exceeded the president’s authority.

Alberta senator wants to revive lapsed Trudeau internet censorship bill

Anti-Trump protests planned across the country on Saturday as LA violence continues

Leftists devastate Los Angeles with fiery riots against Trump immigration policy

FBI Director: CCP Behind Wave of Pathogen Smuggling as Third Chinese Student Charged in Michigan Lab Probe

-

National2 days ago

National2 days agoCarney promotes MP instrumental in freezing Freedom Convoy donors’ bank accounts

-

conflict1 day ago

conflict1 day agoIran nuclear talks were ‘coordinated deception’ between US and Israel: report

-

illegal immigration2 days ago

illegal immigration2 days agoLA protests continue as judge pulls back CA National Guard ahead of ‘No Kings Day’

-

conflict2 days ago

conflict2 days agoIsrael strikes Iran, targeting nuclear sites; U.S. not involved in attack

-

International1 day ago

International1 day agoIsrael’s Decapitation Strike on Iran Reverberates Across Global Flashpoints

-

Energy1 day ago

Energy1 day agoCanada is no energy superpower

-

Alberta1 day ago

Alberta1 day agoPunishing Alberta Oil Production: The Divisive Effect of Policies For Carney’s “Decarbonized Oil”

-

International2 days ago

International2 days agoPentagon agency to simulate lockdowns, mass vaccinations, public compliance messaging