Business

EXCLUSIVE: Investment Giants Leveraged Red State Universities’ Endowment Funds To Back Anti-Oil Agenda, Report Finds

From the Daily Caller News Foundation

![]()

By Jason Cohen

Several asset managers leveraged two major Texas university systems’ endowment funds to advance anti-fossil fuel shareholder proposals in 2022 and 2023, according to a report from the conservative watchdog group American Accountability Foundation (AAF).

BlackRock-owned Aperio Group, Cantillon, former Vice President Al Gore-chaired Generation Investment Management, GQG Partners and JP Morgan Asset Management collectively manage approximately $4 billion for The University of Texas/Texas A&M Investment Management Company (UTIMCO) as of July, which handles the university systems’ endowments. Despite the company’s policy against it and Texas’ status as the leading crude oil and natural gas-producing state, UTIMCO’s asset managers backed over 150 shareholder resolutions under the environmental, social and governance(ESG) umbrella, including proposals that could undermine the oil and gas industry, according to documents AAF obtained through a public records request and shared exclusively with the Daily Caller News Foundation.

“Once again, woke ESG ideology has infected a public institution and hijacked its money for their own purposes. This is an outrageous betrayal of the public’s trust,” AAF president Thomas Jones told the DCNF. “[Republican Texas] Gov. Greg Abbott must take immediate action to end this nonsense. He must shake up the leadership at UT/A&M that let this happen and use his influence with UTIMCO to ensure that it never happens again.”

UTIMCO told the DCNF that the ESG and diversity, equity and inclusion (DEI)-related votes violate “a long-standing policy that prohibits using the endowments’ economic power to advance social or political agendas” and that a review found they consist of 0.3% out of around 45,000 proxy votes in recent years. The endowment manager added that it has since modified its guidelines after finding the violative votes and will impose them on all of its third-party investment managers before future proxy votes, and revoking voting authority for those that cannot follow them.

🚨EXCLUSIVE🚨Swing State’s Pension Funds Used By Wall Street Titans To Push ‘Racial Equity’, Climate Agenda, Report Finds from @jasonJournoDC https://t.co/LXx3y4WZPV

— Daily Caller (@DailyCaller) January 25, 2024

The company’s asset managers voted in favor of a total of 159 shareholder proposals between them that include “racial and gender pay gap reports, efforts to defund conservative candidates and pro-business trade associations, radical climate policy, targeting of gun purchasers, and proabortion initiatives,” according to the watchdog.

UTIMCO oversees the largest public endowment fund in the U.S., managing over $76 billion as of Aug. 31.

“UTIMCO’s mission is to ‘generate superior long-term investment returns to support The University of Texas and Texas A&M University Systems,’ yet these votes endorse political agendas that run contrary to the Systems’ best interests,” American Energy Institute CEO and former Republican Texas state Rep. Jason Isaac told the DCNF. “By supporting proposals that harm American energy producers, UTIMCO’s fund managers are violating their fiduciary responsibility.”

Texas leads the nation in crude oil and natural gas production and in 2023 was responsible for 43% of crude oil output, according to the U.S. Energy Information Administration. However, AAF found many examples of UTIMCO’s asset managers voting in favor of proposals aimed at reducing greenhouse gas emissions (GHG) emissions and other actions to mitigate so-called climate change, which the watchdog alleges comes at the expense of producing value for investors.

For instance, at ExxonMobil’s May 2023 yearly shareholder meeting, Aperio Group voted in support of a proposal to recalculate its GHG emissions to account for the assets it has sold. The resolution asserted that “the economic risks associated with climate change exist in the real world rather than on company balance sheets” and argues that the investments ExxonMobil sells may lower emissions on paper but that they fail to actually help achieve the goal of keeping global temperatures from rising by 1.5 degrees Celsius — which is an objective of the 2015 Paris Climate Agreement — potentially exposing the company and its stakeholders to what it calls “climate risk.”

Some of Aperio Group’s clients have access to customize their individual proxy voting policy, according to BlackRock. BlackRock itself voted against this ExxonMobil proposal on behalf of most of its clients.

AAF’s “report on UTIMCO’s investment practices should alarm every Texan who values our state’s proud oil and gas industry,” Texas Railroad Commissioner Wayne Christian told the DCNF. “It’s outrageous to see Texas university investments being used to support radical ESG agendas, decarbonization, and dangerous policies like Net Zero and the Paris Accord, which threaten our energy independence and economy. We must put an end to the woke political agendas that undermine the very foundation of Texas’ success and ensure our investments align with the values of hard-working Texans.”

Moreover, at defense contractor Raytheon Technologies’ yearly shareholder meeting in May 2023, J.P. Morgan Asset Management backed a proposal urging the company to publish a report on efforts to reduce GHG emissions in alignment with the Paris Climate Agreement.

“Raytheon Technologies creates significant carbon emissions from its value chain and is exposed to numerous climate-related risks,” it states. “Failing to respond to this changing environment may make Raytheon less competitive and have a negative effect on its cost of capital and shareholders’ financial returns.”

Isaac told the DCNF that UTIMCO’s “managers are discriminating against fossil fuel” companies through ESG investing based on the definition of “boycott” in Texas’ Senate Bill 13, which Abbot signed in 2021 and the former representative said he helped create.

The bill defines boycotting energy companies as refusing to engage or ending business with a company involved in fossil fuels “without an ordinary business purpose.” It also specifies actions aimed “to penalize, inflict economic harm on, or limit commercial relations with a company because the company” does business related to fossil fuels and fails to “pledge to meet environmental standards beyond applicable federal and state law.”

Isaac added that the asset managers “should be held accountable and placed on Texas’ list of “financial companies that boycott energy companies,” which mandates Texas public investment entities subject to SB 13 “avoid contracting with, and divest from, these companies unless they can demonstrate this would conflict with their fiduciary duties.”

The S&P Global Clean Energy Index, which includes companies that engage in energy production from renewable sources, has fallen about 7% so far in 2024, while the S&P 500 Energy Index, which features many oil and gas companies, has risen close to 3% in that same time.

Louisianans’ pension funds were similarly leveraged to push climate-related proposals within publicly traded companies, the DCNF reported in April, based on another public records request by AAF.

“UTIMCO’s asset managers’ apparent promotion of leftist objectives, including ESG, is extremely troubling and contrary to Texas law banning boycotts and discrimination against fossil fuels. The legislature must exercise oversight and hold UTIMCO accountable,” Republican Texas state Rep. Brian Harrison told the DCNF. “Governmental bodies, including their proxies, should not pursue objectives that harm the Texas economy and go against our values.”

Cantillon, GQG Partners, Texas A&M and Abbot’s office did not respond to the DCNF’s requests for comment. Aperio Group, Generation Investment Management, JP Morgan Asset Management and the University of Texas declined to comment.

Business

The world is no longer buying a transition to “something else” without defining what that is

From Resource Works

Even Bill Gates has shifted his stance, acknowledging that renewables alone can’t sustain a modern energy system — a reality still driving decisions in Canada.

You know the world has shifted when the New York Times, long a pulpit for hydrocarbon shame, starts publishing passages like this:

“Changes in policy matter, but the shift is also guided by the practical lessons that companies, governments and societies have learned about the difficulties in shifting from a world that runs on fossil fuels to something else.”

For years, the Times and much of the English-language press clung to a comfortable catechism: 100 per cent renewables were just around the corner, the end of hydrocarbons was preordained, and anyone who pointed to physics or economics was treated as some combination of backward, compromised or dangerous. But now the evidence has grown too big to ignore.

Across Europe, the retreat to energy realism is unmistakable. TotalEnergies is spending €5.1 billion on gas-fired plants in Britain, Italy, France, Ireland and the Netherlands because wind and solar can’t meet demand on their own. Shell is walking away from marquee offshore wind projects because the economics do not work. Italy and Greece are fast-tracking new gas development after years of prohibitions. Europe is rediscovering what modern economies require: firm, dispatchable power and secure domestic supply.

Meanwhile, Canada continues to tell itself a different story — and British Columbia most of all.

A new Fraser Institute study from Jock Finlayson and Karen Graham uses Statistics Canada’s own environmental goods and services and clean-tech accounts to quantify what Canada’s “clean economy” actually is, not what political speeches claim it could be.

The numbers are clear:

- The clean economy is 3.0–3.6 per cent of GDP.

- It accounts for about 2 per cent of employment.

- It has grown, but not faster than the economy overall.

- And its two largest components are hydroelectricity and waste management — mature legacy sectors, not shiny new clean-tech champions.

Despite $158 billion in federal “green” spending since 2014, Canada’s clean economy has not become the unstoppable engine of prosperity that policymakers have promised. Finlayson and Graham’s analysis casts serious doubt on the explosive-growth scenarios embraced by many politicians and commentators.

What’s striking is how mainstream this realism has become. Even Bill Gates, whose philanthropic footprint helped popularize much of the early clean-tech optimism, now says bluntly that the world had “no chance” of hitting its climate targets on the backs of renewables alone. His message is simple: the system is too big, the physics too hard, and the intermittency problem too unforgiving. Wind and solar will grow, but without firm power — nuclear, natural gas with carbon management, next-generation grid technologies — the transition collapses under its own weight. When the world’s most influential climate philanthropist says the story we’ve been sold isn’t technically possible, it should give policymakers pause.

And this is where the British Columbia story becomes astonishing.

It would be one thing if the result was dramatic reductions in emissions. The provincial government remains locked into the CleanBC architecture despite a record of consistently missed targets.

Since the staunchest defenders of CleanBC are not much bothered by the lack of meaningful GHG reductions, a reasonable person is left wondering whether there is some other motivation. Meanwhile, Victoria’s own numbers a couple of years ago projected an annual GDP hit of courtesy CleanBC of roughly $11 billion.

But here is the part that would make any objective analyst blink: when I recently flagged my interest in presenting my research to the CleanBC review panel, I discovered that the “reviewers” were, in fact, two of the key architects of the very program being reviewed. They were effectively asked to judge their own work.

You can imagine what they told us.

What I saw in that room was not an evidence-driven assessment of performance. It was a high-handed, fact-light defence of an ideological commitment. When we presented data showing that doctrinaire renewables-only thinking was failing both the economy and the environment, the reception was dismissive and incurious. It was the opposite of what a serious policy review looks like.

Meanwhile our hydro-based electricity system is facing historic challenges: long term droughts, soaring demand, unanswered questions about how growth will be powered especially in the crucial Northwest BC region, and continuing insistence that providers of reliable and relatively clean natural gas are to be frustrated at every turn.

Elsewhere, the price of change increasingly includes being able to explain how you were going to accomplish the things that you promise.

And yes — in some places it will take time for the tide of energy unreality to recede. But that doesn’t mean we shouldn’t be improving our systems, reducing emissions, and investing in technologies that genuinely work. It simply means we must stop pretending politics can overrule physics.

Europe has learned this lesson the hard way. Global energy companies are reorganizing around a 50-50 world of firm natural gas and renewables — the model many experts have been signalling for years. Even the New York Times now describes this shift with a note of astonishment.

British Columbia, meanwhile, remains committed to its own storyline even as the ground shifts beneath it. This isn’t about who wins the argument — it’s about government staying locked on its most basic duty: safeguarding the incomes and stability of the families who depend on a functioning energy system.

Resource Works News

“It’s a good a bet that high-speed rail between Toronto and Quebec City isn’t even among the top 1,000 priorities for most Canadians.”

The Canadian Taxpayers Federation is criticizing Prime Minister Mark Carney for borrowing billions more for high-speed rail between Toronto and Quebec City.

“Canadians need help paying for basics, they don’t need another massive bill from the government for a project that only benefits one corner of the country,” said Franco Terrazzano, CTF Federal Director. “It’s a good a bet that high-speed rail between Toronto and Quebec City isn’t even among the top 1,000 priorities for most Canadians.

“High-speed rail will be another costly taxpayer boondoggle.”

The federal government announced today that the first portion of the high-speed rail line will be built between Ottawa and Montreal with constructing starting in 2029. The entire high-speed rail line is expected to go between Toronto and Quebec City.

The federal Crown corporation tasked with overseeing the project “estimated that the full line will cost between $60 billion and $90 billion, which would be funded by a mix of government money and private investment,” the Globe and Mail reported.

The government already owns a railway company, VIA Rail. The government gave VIA Rail $1.9 billion over the last five years to cover its operating losses, according to the Crown corporation’s annual report.

The federal government is borrowing about $78 billion this year. The federal debt will reach $1.35 trillion by the end of this year. Debt interest charges will cost taxpayers $55.6 billion this year, which is more than the federal government will send to the provinces in health transfers ($54.7 billion) or collect through the GST ($54.4 billion).

“The government is up to its eyeballs in debt and is already spending hundreds of millions of dollars bailing out its current train company, the last thing taxpayers need is to pay higher debt interest charges for a new government train boondoggle,” Terrazzano said. “Instead of borrowing billions more for pet projects, Carney needs to focus on making life more affordable and paying down the debt.”

Wisdom of Our Elders: The Contempt for Memory in Canadian Indigenous Policy

Liberal bill “targets Christians” by removing religious exemption in hate-speech law

Egypt, Iran ‘completely reject’ World Cup ‘Pride Match’ plan

Canada’s free speech record is cracking under pressure

-

National2 days ago

Canada’s free speech record is cracking under pressure

-

Energy1 day ago

Energy1 day agoTanker ban politics leading to a reckoning for B.C.

-

Energy1 day ago

Energy1 day agoMeet REEF — the massive new export engine Canadians have never heard of

-

Business2 days ago

Business2 days agoTaxpayers Federation calls on politicians to reject funding for new Ottawa Senators arena

-

Fraser Institute1 day ago

Fraser Institute1 day agoClaims about ‘unmarked graves’ don’t withstand scrutiny

-

Business2 days ago

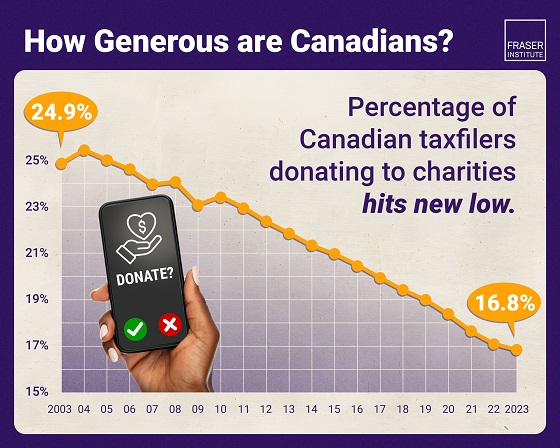

Business2 days agoAlbertans give most on average but Canadian generosity hits lowest point in 20 years

-

Energy10 hours ago

Energy10 hours agoCanada’s future prosperity runs through the northwest coast

-

Business1 day ago

Business1 day agoToo nice to fight, Canada’s vulnerability in the age of authoritarian coercion